With the benefit of hindsight, the UK housing market possibly didn’t need a stamp duty holiday in July 2020, four months into the pandemic. Trading activity was strong during successive lockdowns as people reassessed how and where they lived.

But some form of UK-wide support would certainly be welcome now given the negative events supressing demand. We will find out if the government has a plan in the Autumn Statement later this month.

In the meantime, the number of UK mortgage approvals was more than a third below the five-year average in September and transaction volumes were down by just under a quarter.

NO SINGLE CAUSE

Unlike the early months of Covid or the period following the mini-Budget, there is no single cause of the slowdown.

Sentiment has been affected by a series of factors including the financial pain of higher mortgage rates, the Bank of England’s struggle to contain inflation, the impending general election, and uncertainty arising from overseas military conflicts.

The weak sentiment extends to London’s prime postcodes. Activity in prime central and outer London this October was similar to the same month in 2022, a moment of high uncertainty after the mini-Budget caused a spike in rates and the widespread withdrawal of mortgage products.

The number of new prospective buyers registering in London was only 1.2% higher, exchanges were 2.2% higher and the number of viewings was 1.4% lower.

CASH BUYERS

A greater proportion of cash buyers and higher levels of housing equity help protect prime London markets to some degree but they have less effect on overall sentiment.

A rise in the supply of higher-value lettings properties demonstrates how some prospective sellers are hesitating and opting to let out their property instead.

The number of rental properties coming to the housing market in prime central London above £1,000 per was 22% higher in October compared to the same month last year. Meanwhile, prices also reflect the current mood of uncertainty.

The quarterly fall of -0.9% was the biggest since July 2020.”

Average prices in prime central London fell 1.6% in the year to October, with 1.2% of the decline taking place in the last six months. The quarterly fall of -0.9% was the biggest since July 2020, the month that the stamp duty holiday was introduced.

Meanwhile, activity in prime outer London (POL) was supported more by needs-driven buyers. That said, average prices in POL fell 1.4% for the second consecutive month, the biggest drop since February 2021.

High demand and low supply have pushed up rental values at unprecedented rates over the last two years, but the financial pain for tenants is reducing as the market re-balances.

Source: Knight Frank / Rightmove

Average rents in prime central (9.6%) and outer London (8.3%) both grew by less than 10% in the year to October, the first time the annual rate has been in single digits since September 2021. Furthermore, there was no monthly change to average rents in either market, the first time they have been flat since April 2021.

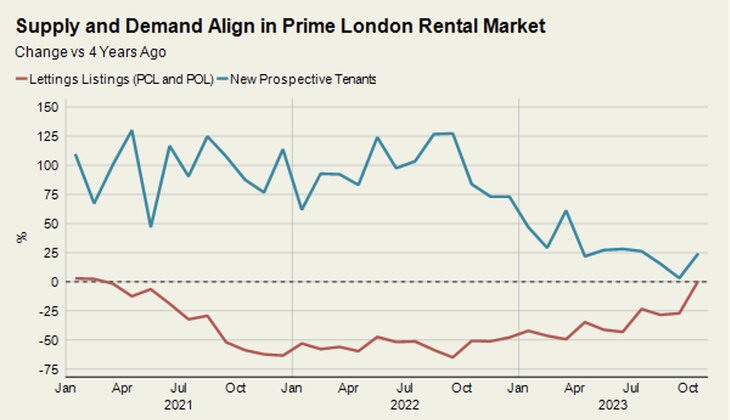

Overall, the supply of lettings property in PCL and POL was 0.6% higher than in 2019. Meanwhile, the number of new prospective tenants has calmed down in recent months.

Landlords have faced a proliferation of red tape and higher taxes.”

Supply has been driven lower in recent years as landlords have faced a proliferation of red tape and higher taxes. Meanwhile, demand has been underpinned by a sharp rise in mortgage rates that has forced more prospective buyers to become tenants.

housing market

As the situation re-balances, supply has increased to a greater extent in higher-value markets where owners, who typically have more financial flexibility, have opted to let out their property given the weakness in the sales market.

Despite the slowdown, average rents in PCL are 32% higher than they were before the pandemic while the equivalent increase is 28% in POL.

Higher rents and a weak sales market also mean yields are rising. The average gross yield in PCL in October was 4.15%, which compares to 3.42% before the pandemic.

While this will attract some landlords into the sector, rising mortgage costs, tax and red tape are likely to keep downwards pressure on supply.

Tom Bill (main picture) is head of UK residential research at Knight Frank

{kind=link}