NEW YORK (ICIS)–The failure of two sizeable

banks (Silicon Valley Bank and Signature Bank)

in the US and the crisis of confidence

contagion spreading to other regional banks and

now European financial institutions threatens

to significantly tighten lending conditions at

the very least, further slowing economic growth

and potentially tipping US and European

economies into recession.

The implications for the economically sensitive

chemical industry are huge, as a major step

down in GDP growth or a contraction would

crater demand in an already weak environment.

The US regional banking crisis reduces the odds

of a soft landing, and our base case is still a

mild recession lasting two to three quarters.

Stabilising the financial system will be

critical to keeping the downturn mild.

The emergency takeover of Credit Suisse by UBS

at the behest of the Swiss government

highlights the inherent risks to the global

economy from banking contagion.

The US Federal Reserve raised interest rates at a record pace through 2022 to tamp down runaway

inflation. The result has been a collapse

in the value of long-term Treasuries and other

long-duration debt such as mortgage-backed

securities (MBS) that banks accumulated on

their books. In a bank run, banks must sell

these securities at big

losses to cover outflows.

The Fed, Treasury, and Federal Deposit

Insurance Corporation (FDI)C stepped in on 12

March with a strong move to halt a run on

regional banks, guaranteeing all deposits at

the two banks above the protected $250,000

threshold.

The Fed also created a new lending facility to

boost liquidity where banks can pledge debt

securities as collateral at par (face value),

even if the value of those securities may be

far lower.

Yet without an explicit guarantee that all

uninsured bank deposits (those over $250,000)

will be safe, it’s hard not to believe large

depositors, including businesses, will continue

to take funds out of smaller regional banks and

put them into the ones deemed

“too big to fail”.

DOWNBEAT DATA

Meanwhile,

the latest economic data from the US shows

weakening consumer spending and inflation at

the producer level.

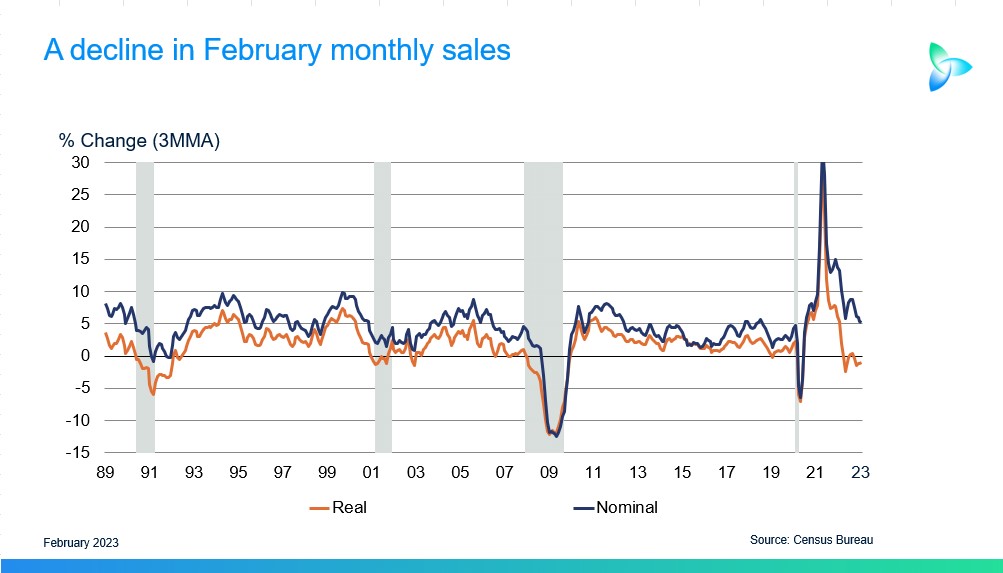

Retail sales fell by 0.4% month on month in

February, while the Producer Price Index (PPI)

fell by 0.1%. Yet the key Consumer Price

Index (CPI) was up by 0.4% in February from

January and up by 6.0% year on year.

The core CPI (excluding food and energy) being up 5.5% from last year is still well above the Fed’s 2% inflation target.

The Fed on 22 March raised rates by another

0.25 percentage points and

softened its stance towards further hikes

in the light of uncertainty amid the regional

banking crisis. The Fed remains undeterred in

its goal of bringing inflation down to its 2%

target.

Fed chair Jerome Powell acknowledged that the

banking turmoil will likely tighten credit

conditions, but added that it is too early to

tell the extent of the impact.

GROWTH SLOWLY RISING

ICIS

expectations for US GDP growth are at around

0.6% in 2023 and 0.7% in 2024. Global GDP

is forecast to grow at 1.8% in 2023, rebounding

to 2.8% in 2024.

The US industrial sector is already taking a

hit, with the latest ISM US Manufacturing

Purchasing Managers’ Index (PMI) in contraction

(below 50) in February for the fourth

consecutive month at 47.7. However, the

Services PMI remains strong, with the February

reading at 55.1.

The labour market continues to show resilience,

with unemployment ticking up slightly to 3.6%

in February. Wage gains have moderated,

providing some relief on the inflation front.

Meanwhile, the ICIS US Leading Business

Barometer (LBB) rebounded in February after 11

months of decline but is still signalling

recessionary conditions. Even as interest rates

are poised to decline heading into a recession,

tighter credit conditions will continue to

weigh on the key housing and automotive end

markets.

ICIS projects that US housing starts will

plunge by 19% to 1.26m in 2023. While light

vehicle sales are expected to rebound by 7% to

14.7m units this year on easing supply-chain

constraints, they will remain far below the

pre-pandemic 2019 level of 17.0m.

Additional contribution from ICIS senior

economist Kevin Swift

{kind=link}