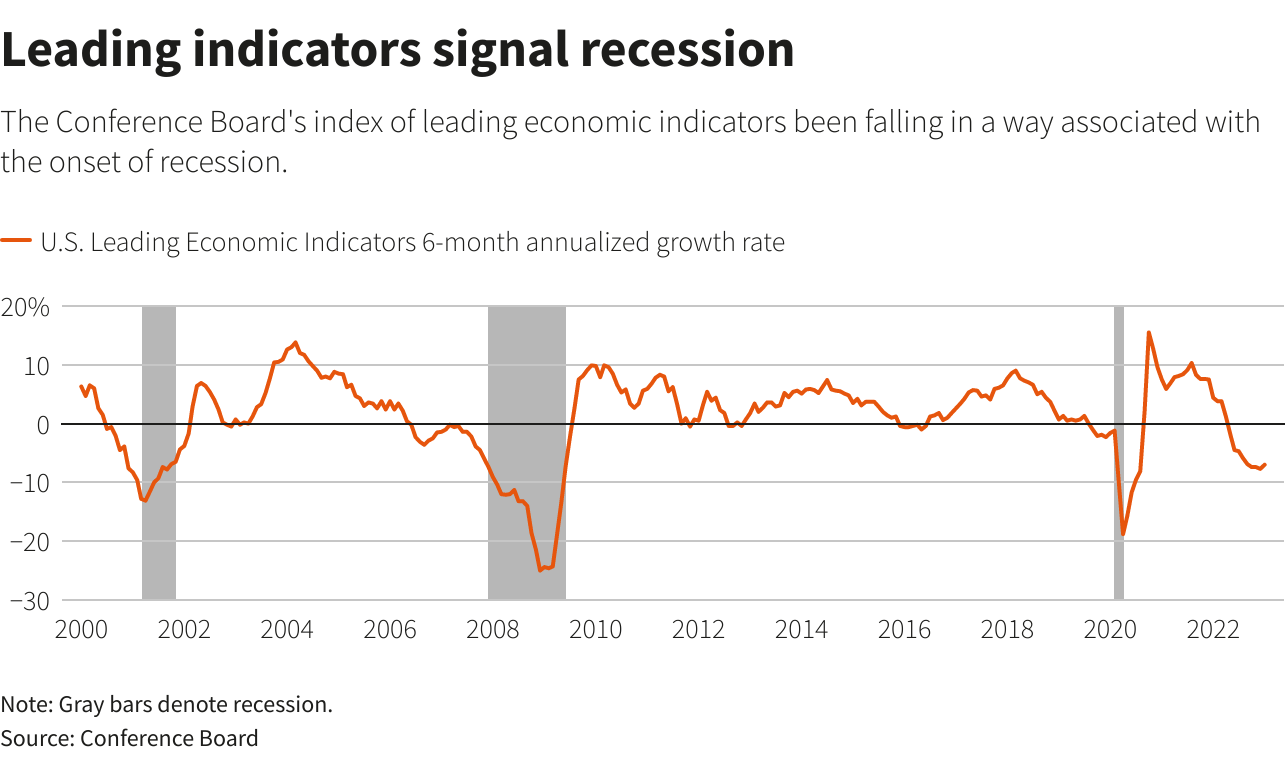

WASHINGTON, Feb 27 (Reuters) – Dana Peterson, the chief economist at the Conference Board, sees a clear conclusion in the sharp decline of the U.S. business group’s Leading Economic Index: If recession isn’t already taking hold in the United States, then it will soon.

Tell that to Matt Malone, the chief executive officer of Groundworks, and the response is anything but recessionary – with his residential foundation and water management company still booking strong sales, pressing to fill several hundred open jobs, and seeing consumers ready to spend.

“We’ve been talking about impending recession for several quarters now,” said Malone, whose Virginia Beach-based company has a national footprint. “There’s a lot of confusion and mixed signals as to what’s going on with the consumer … At the end of the day, we have not seen it affect our business yet.”

Such is the mystery of the U.S. economy, and increasingly the global one as well, three years after the onset of a devastating pandemic, a year and a half into a still-developing inflation surge, and many months into predictions of recessions that continue to miss the mark.

Latest Updates

View 2 more stories

Major central banks have jacked up interest rates at a pace many policymakers and economists thought would prove crushing, perhaps taming inflation but at a high cost. Inflation has slowed a bit, but not so fast or so far that any central banker feels the war is won, and recent data have shown the progress to be slowing.

Demand for goods and services has fallen in sectors like housing and technology that are both highly sensitive to interest rates and were big pandemic winners perhaps due for a trim; but economy-wide, many of the recent surprises have been to the upside as consumers keep finding the means to spend.

The job market?

Businesses like Malone’s don’t seem to have gotten the memo. The U.S. unemployment rate, at 3.4%, is the lowest it has been since 1969. At this point, Fed officials are less concerned about recession than of trends like labor hoarding that may keep available workers scarce and prevent the modest rise in unemployment many of them feel is needed for inflation to fall.

Cleveland Fed President Loretta Mester said in a CNBC interview on Friday that she felt the economy would grow “well below trend” this year, but grow nonetheless.

While some sectors are slowing, “coming into this year there was a little bit more underlying strength than forecasters thought,” Mester said, while businesses “have spent so much effort to hire people they are going to do everything they can to keep people on staff, so after we get beyond this slowdown they will have the staff they need.”

CONSUMER IS ‘KEY’

Globally, similar dynamics have developed as seemingly inevitable recessions in the euro zone and the United Kingdom have given way to modest ongoing growth.

Unusually warm weather and lower energy prices have helped. So has unexpectedly strong consumer spending and, for the world outlook, the reopening of China’s economy from strict COVID lockdowns.

It is, Peterson acknowledged, shaping up as a weird situation. Even if a U.S. recession takes place, she said it could well be short and shallow, with companies retaining hard-to-find workers and only modest cutbacks in household and business spending.

“Businesses are telling us that they are continuing to hire, or not looking to shrink their labor force,” Peterson said. She added, however, that ultimately “the key is the consumer.”

“How much are consumers willing to spend? Out of their own income, their wealth … their credit cards? Maybe we are approaching the point where consumers are tapped out.”

There are warnings on that front beyond the Conference Board’s key U.S. index, which has been flashing a recession warning for about a year now.

In the bond market, yields on shorter-term government debt are above those for longer-term securities, a classic recession signal but one Fed officials discount as distorted by inflation.

On a recent earnings call, Walmart Inc (WMT.N) executives noted strong sales growth but signs of economically weakened households: Higher-income consumers bargain shopping to beat inflation, for example, or lagging purchases for discretionary goods.

‘MORE RESILIENT’

If, however, consumers continue consuming, hiring bosses keep hiring, and the economy keeps expanding, the dilemma for the Fed and other major central banks is whether inflation can still slow in such an environment.

It’s an iffy proposition. Indeed, an Atlanta Fed model currently sees first-quarter U.S. GDP growth, for one, at a robust 2.5%.

The situation has snapped financial markets into their closest alignment with the Fed’s outlook since the U.S. central bank began shifting its monetary policy stance in late 2021 and started raising interest rates last March.

Markets have long been skeptical of the Fed’s resolve, but what finally seems to have synched them with the U.S. central bank has been data showing the economy was not cracking easily, nor was inflation slowing easily. That poured cold water on the idea that the Fed would “pivot” on a dime to lower rates.

Benson Durham, head of global asset allocation at Piper Sandler, said his analysis suggests the recent rise in bond yields that more closely aligned markets with the Fed may not be such good news because it seems to have been driven by expectations for higher inflation.

“Government bond yields are up” since the last Fed policy meeting, Durham wrote. “But to conclude that financial conditions are thereby tighter, and that the Fed has less work to do now, would be hasty … The Fed may now punch harder.”

The release in the coming weeks of employment and inflation data for February will be important in determining whether that is about to happen as Fed policymakers prepare for a March 21-22 meeting, which will include a decision on rates and updated projections for the policy rate and economic outlook.

U.S. consumption and inflation data released on Friday would appear to argue for Fed policymakers to raise their estimated stopping point for the policy rate above December’s forecast of 5.1%. Consumer spending rose by the most in nearly two years in January; inflation-tracking indexes that form the basis for Fed policy accelerated that month; and revisions to late-2022 figures showed less progress had been made in beating back inflation than previously thought.

Some argue, however, that the developing market outlook for stickier inflation and higher interest rates may just be the flip side of an economy that keeps surprising in its strength, and which Fed policymakers still feel they can guide to lower inflation levels without a collapse.

“Markets overpriced a recession in the second half of 2022 and overpriced a recession in the first half of 2023,” St. Louis Fed President James Bullard told CNBC last week. “It kind of seems the U.S. economy might be more resilient than markets thought six or eight weeks ago.”

Reporting by Howard Schneider;

Additional reporting by William Schomberg in London;

Editing by Dan Burns and Paul Simao

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}