LONDON/NEW YORK, Feb 22 (Reuters) – Markets, bracing for a “no landing” scenario where global economic growth is resilient and inflation stays higher for longer, are dialling back appetite for both risk assets and government debt.

For months, investors have bet on global growth softening just enough to cool inflation and persuade hawkish central banks to pause their rate hikes.

The notion of the U.S. Federal Reserve and other central banks using monetary tightening to engineer a mild, soft landing before pivoting to avoid a deep recession has supported a cross-asset rally since October, depressed the dollar and sent capital flowing into emerging markets.

But recent data reflecting still tight jobs markets has traders entertaining a new scenario where economic growth holds up and inflation remains sticky.

That means rates could be pushed higher too – a negative for risk assets. World stocks hit one-month lows on Wednesday, while Wall Street had its worst day of the year so far on Tuesday.

“We’ve gone from softer landing to no landing – no landing being that (financing) conditions will remain tight,” said David Katimbo-Mugwanya, head of fixed income at EdenTree Asset Management.

Latest Updates

View 2 more stories

U.S. jobs growth accelerated sharply in January, U.S. and German inflation remained high, while U.S. and European business activity rebounded in February.

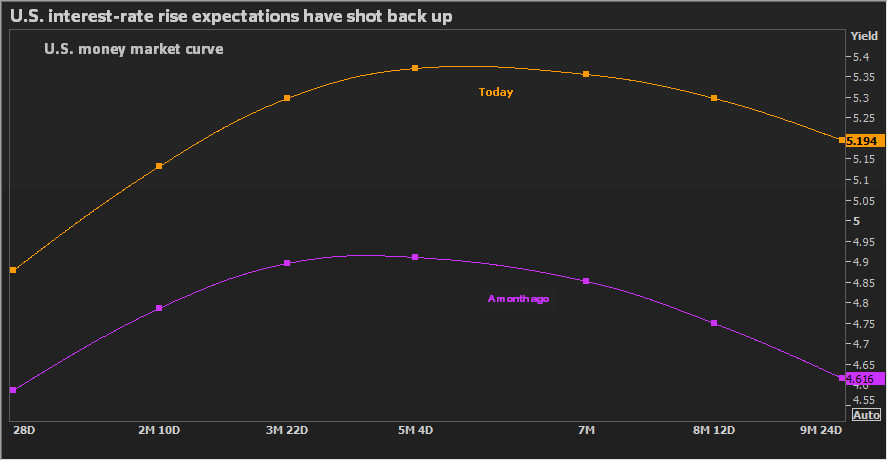

Investors have now ditched expectations for rate cuts later this year and renewed their bets on higher rates, which in the U.S. are now seen peaking in July at about 5.3%, up from about 4.8% in early February.

Deutsche Bank said this week it expects European Central Bank rates to peak at 3.75% from 3.25% previously.

China’s reopening, an easing in Europe’s gas crisis and strong U.S. consumer spending “are probably more bearish than positive for markets,” said Richard Dias, founder of macro-economic research house Acorn Macro Consulting.

“We’re getting into a situation where good news is bad news,” he said.

For Paul Flood, head of mixed assets at Newton Investment Management, “if wage growth stays high and demand stays high, then the Fed will push up interest rates further and that’s not a good environment for equity or bond markets.”

Bond prices fall, and yields rise, when expectations of higher rates on cash make their fixed interest payments less appealing. Stocks typically move lower when bond yields rise to account for the extra risk of owning shares.

U.S. 10-year Treasury yields are near their highest since November at almost 4%, up from a January low of 3.3% . An index measuring the dollar against other major currencies is set for its first monthly gain in five as rate-hike bets lift the greenback .

GOODBYE RECESSION RISK?

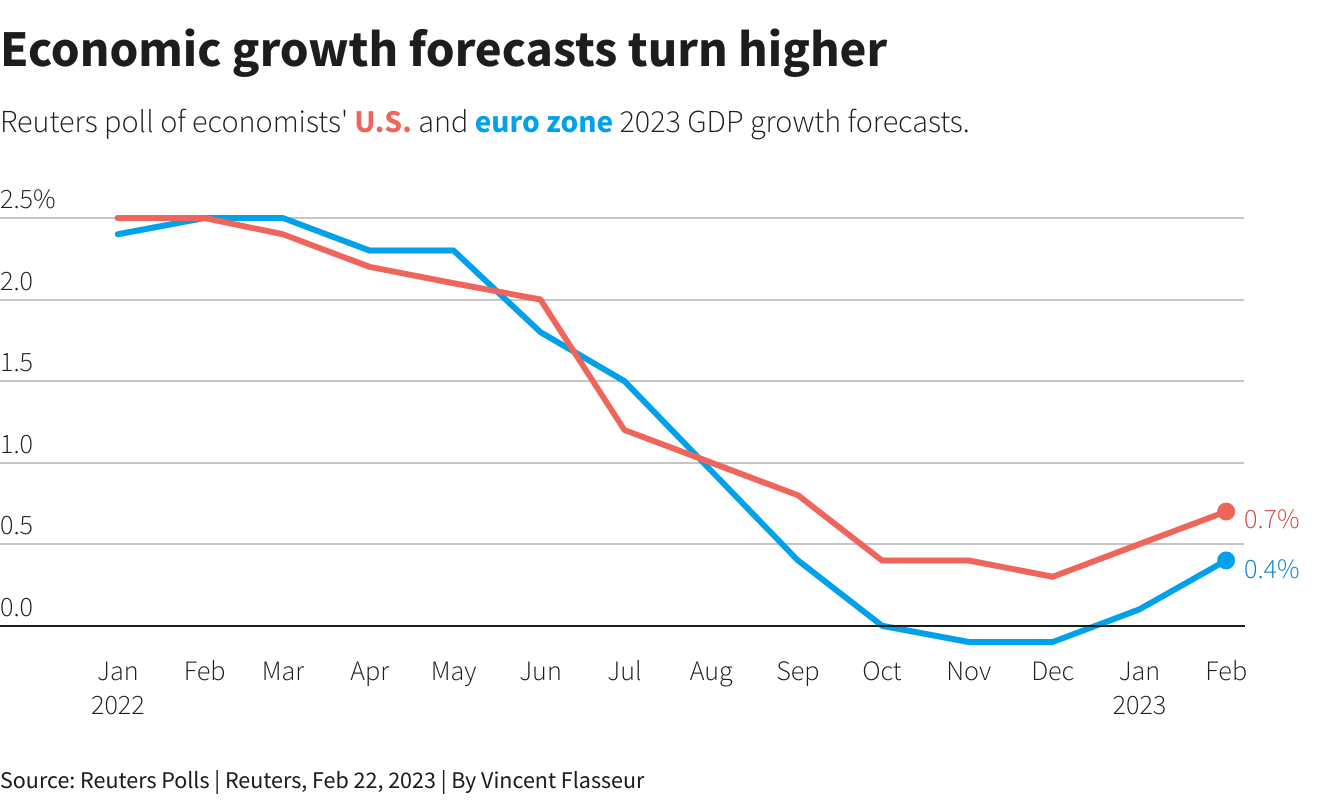

In December, most economists expected the U.S. economy to contract slightly this year but the consensus now is for 0.7% growth. Fed officials have signalled that they will likely keep raising rates for longer than previously forecast.

Euro zone recession expectations mostly faded in mid January as energy prices tumbled. Economists polled by Reuters see inflation in the bloc remaining above its 2% target into 2025 as growth holds up.

“The road map was one of a shallow recession and declining inflation,” said Florian Ielpo, head of macro at Lombard Odier Investment Managers. “That consensus is being challenged by the data.”

Many investors still believe inflation will subside, and see recent strong data as probably supported by one-time factors such as an unseasonably mild winter and the remainder of consumer savings accumulated during the COVID-19 pandemic.

“There should be more signs of a slowdown as the year unfolds and weather normalises, and there’s just not another pent up savings to spend as we go into the second half of the year,” said Rhys Williams, chief strategist at Spouting Rock Asset Management.

Thomas Hayes, chairman and managing member of New York-based Great Hill Capital, said a soft landing is still likely as declining U.S. rental costs start weighing on inflation metrics and labour market participation increases as consumers run out of savings, helping contain wage growth.

“If oil doesn’t spike above $100 it is going be very hard for inflation to re-accelerate after the Fed pauses,” he said.

Lombard Odier’s Ielpo said he had not changed the positioning of his funds significantly since January but was “happy to not have more” equity risk.

Katimbo-Mugwanya at EdenTree Asset Management, said long-dated bonds still offered value as he saw central banks still closing in on the end of rate-rise cycles.

But, he added, because “data is a bit more robust on the economic front than maybe we were led to believe at the turn of the year…there’s no pressure on them to start signalling a looser stance just yet.”

Reporting by Naomi Rovnick in London and Davide Barbuscia in New York; additional reporting by Yoruk Bahceli in Amsterdam, Editing by Dhara Ranasinghe and Kirsten Donovan

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}