Bogota, Mexico City y Sao Paulo — Brazil, Mexico and Colombia, three of the largest economies in Latin America, have experienced double-digit currency appreciation against the dollar so far this year, not only due to a more favorable global context for emerging markets, but also to the uniqueness of local conditions in each country.

Macroeconomic diversity in Latin America has impacted exchange rates from Brazil to Mexico, with currencies in the largest markets among the most appreciated in emerging markets so far in 2023. But how can such different economies muster these levels of appreciation against the greenback?

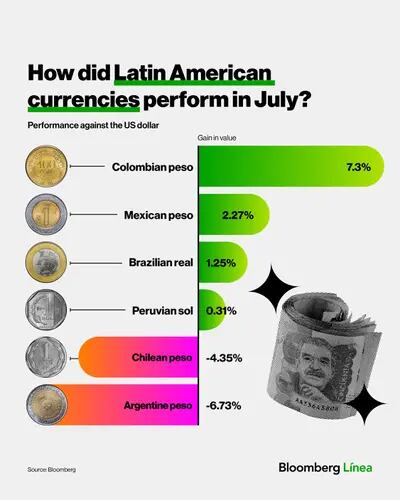

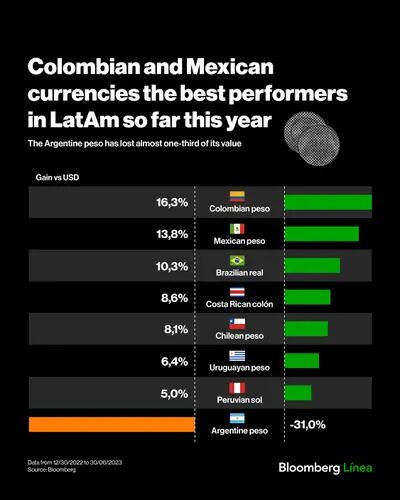

The currencies in question are in fact the three most appreciated against the dollar among emerging markets in 2023. While the Colombian peso has strengthened by 19.61%, the Mexican peso has risen by 14.53% and the Brazilian real by 9.77%.

Although the dollar’s weakness globally has been one of the main ingredients in this dynamic, local factors such as the political climate and investments driven by the different administrations are also playing a key role.

On the international scene, the prospect of the Federal Reserve halting interest rate hikes has helped to favor investments in emerging markets such as Brazil, which still offers higher interest rates.

The view that the U.S. central bank is managing to bring down inflation without triggering a recession has also brought relief to financial markets.

Credicorp Capital’s Managing Director and Chief Research Economist, Daniel Velandia, explained to Bloomberg Línea in Bogota that currency trends in the region have closely followed global developments.

In fact, in recent days, the region’s currencies have been impacted by the uncertainty of triggered by Fitch’s downgrade of the US’ long-term credit rating from AAA to AA+, highlighting the degree of external vulnerability that still weighs on these markets.

“We have seen a depreciation of the dollar globally so far this year and this has been reflected in the countries of the region, particularly in those with higher interest rates such as Colombia, Brazil and Mexico”, stated Velandia.

Credicorp Capital argues that in a context in which the US Federal Reserve is expected to end its rate hike cycle soon and begin to cut rates, this could generate a positive climate for risk taking and the search for higher yields.

Brazilian real: spending figures are positive for the real

In Brazil, the dollar has lost strength against the real in recent months and, in July, quotes reached the lowest levels so far this year.

The US currency started 2023 trading at R$5.28 and reached a high of R$5.47 on January 3. The current price is still historically high. However, the depreciation of the dollar has helped keep inflation under control, preventing price increases in products influenced by international prices, such as fuel and food.

The 12-month cumulative national consumer price index (CPI) reached 3.16% in June, a significant drop from the 12.1% peak in April 2022.

On the domestic front, the approval of the new fiscal rules and tax reform in the Lower House have reduced uncertainties about the public accounts. Greater control over spending tends to avoid a disorderly growth of gross debt in relation to GDP, as well as leading to a reduction of the primary deficit.

“The economy continues to benefit from a more favorable scenario, marked by an inflation target set at 3% for the years 2024 to 2026 and the approval of the tax reform of indirect taxes in the Chamber of Deputies,” said economists Leonardo Paiva and Arthur Mota, from BTG Pactua (BPAC11), in a foreign exchange report in July. “These decisions improved predictability for market players.”

On that note, the Credicorp Capital analyst highlighted in conversation with Bloomberg Línea “the substantial improvement in Brazil’s fiscal accounts”, which is one of the issues that worries investors the most: “President Lula da Silva has been successful in Congress with the approval of a new fiscal framework and at the same time of a tax reform”.

“What we have been seeing is a reduction in fiscal risks. Likewise, there were doubts about President Lula da Silva’s governability, especially with the protests and violence at the beginning of his term, but all that has been correcting itself and then the market is assuming that there is a good environment to carry out reforms that for now do not look radical, which was also an important fear,” he pointed out.

In addition to lower fiscal risk, the prospect of a cycle of lower interest rates and higher-than-expected Gross Domestic Product (GDP) growth has contributed to the appreciation of the country’s main assets.

The Ibovespa (IBOV), the main stock market index, rose 24.5% between its March low and the end of July.

The recent upgrade of Brazil’s credit rating from BB- to BB by Fitch and the revision of the country’s rating to positive by S&P helped attract investors’ attention to the country, favoring capital inflows.

“Brazil is also showing that the Lula government continues to be pragmatic,” David Cubides, director of economic research at the brokerage firm Alianza Valores, told Bloomberg Línea.

In the face of the falling dollar, Brazilian exports continue to be high, favored by the increase in foreign sales in the agricultural sector and the still high prices of raw materials.

In July, the trade balance reached a monthly record, totaling US$9 billion. In the year to July, Brazil recorded a positive trade balance of US$54.1 billion, 36% more than in the same period of the previous year, according to data from the Ministry of Development, Industry, Trade and Services.

Mexican peso strengthens on nearshoring and remittances

In Mexico, the peso has rallied on investments related to nearshoring, as well as healthy fiscal accounts that are attracting fixed income flows from abroad once again, according to sources consulted by Bloomberg Linea.

Investment expectations are growing through nearshoring due to Mexico’s proximity to the US, according to Finamex’s chief economist, Jessica Roldán.

The inflow of dollars into the country through record remittances and foreign investment also stands out.

Velandia, from Credicorp Capital, highlighted the fact that US economic activity has slowed to a lesser extent, and that this is key in the dynamics of remittances to Mexico, which continue “to be a very important factor for the movement of the currency and has surprised on the upside”.

Even so, the main catalyst is the rate spread between the Bank of Mexico and the US Federal Reserve, which currently stands at 575 basis points, sparking investors’ interest in Mexican peso-denominated assets.

Another element is the liquidity of the Mexican currency against its peers, according to Gabriela Siller, Chief Economist at Banco Base.

According to the latest triennial survey by the Bank for International Settlements (BIS), the Mexican peso is the third most liquid currency in the basket of emerging countries and the most liquid in Latin America, along with Brazil’s.

The elements that will determine the direction of the Mexican currency are the monetary policy of the Fed and the Bank of Mexico.

BlackRock analysts estimate that Banxico, as the local monetary authority is known, will start cutting rates and, with this, the Mexican peso will begin a gradual depreciation.

So far, the Citibanamex analyst survey estimates that the Mexican peso will close the year at MXN17.95 per greenback, equivalent to a 5.5% depreciation from the August 2 intraday price of $17 per unit.

Moderate reforms could support the Colombian peso

The Colombian peso appreciated by 7.21% against the US dollar in July, and was the strongest currency among emerging markets. However, the Andean currency has lost ground once again in August and has returned to the 4,000 peso level in the face of global pressures due to the US rating downgrade.

In the case of Colombia, Cubides explains that the rebound of the peso so far this year has to do, in part, a base effect. “Last year Colombia had one of the worst currencies in this same basket. So, here what we are basically doing is giving back all those losses we experienced last year,” the analyst told this media outlet.

The lower price of the dollar in recent months in the country has been accompanied by a moderation in the cost of living, as inflation lost pace for the third consecutive month in June and stood at 12.13% annually in Colombia.

Likewise, Cubides associates this dynamic of the Colombian peso to the fact that the “political scenario has also calmed down a little” in view of the reforms proposed by Gustavo Petro’s administration, which in this legislature will insist on moving forward with its projects to modify the labor and retirement systems, after the setbacks suffered in Congress in the last legislature.

For Cubides, “the markets are beginning to incorporate the idea that eventually they will not end up passing all the proposals coming from the Executive, nor as originally presented”.

“In general, we know that the President does not have a coalition in Congress, he dropped the labor reform, the political reform. And despite the fact that the Government’s objective was to approve the most important reforms before the end of the first semester of the year, only the pension and health reforms have passed in a debate. Therefore, this is going much slower”, complemented Daniel Velandia, from Credicorp Capital.

In addition, the regional and local elections of mayors and governors in October could change the political panorama of the country, with which “the governability of President Petro, in part, will be at stake”, in the midst of the sharp drop in the approval of his Administration.

{kind=link}