WASHINGTON, April 5 (Reuters) – The U.S. services sector slowed more than expected in March as demand cooled, while a measure of prices paid by services businesses fell to the lowest in nearly three years, giving the Federal Reserve a boost in the fight against inflation.

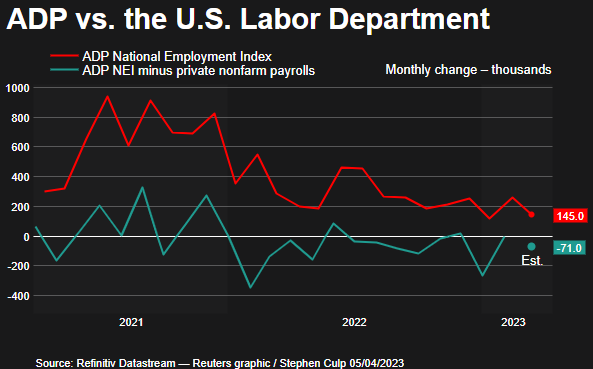

There are also growing signs that the labor market is loosening, with other data on Wednesday showing private payrolls growth slowed considerably last month. This followed on the heels of news on Tuesday that job openings fell below 10 million at the end of February for first time in nearly two years.

The Fed is contemplating pausing the U.S. central bank’s fastest interest rate hiking cycle since the 1980s.

“The Fed wants this and needs this,” said Jennifer Lee, a senior economist at BMO Capital markets in Toronto. “Slower growth, slower demand for services, slower demand for workers, and slower inflation. We’re getting there.”

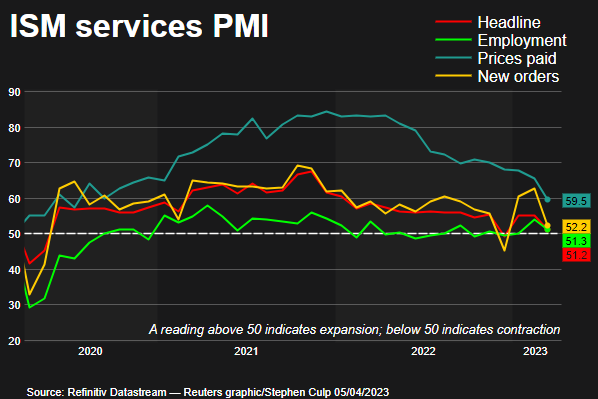

The Institute for Supply Management (ISM) said its non-manufacturing PMI fell to 51.2 last month from 55.1 in February. A reading above 50 indicates growth in the services industry, which accounts for more than two-thirds of the economy.

There was no mention of the financial markets turmoil, which has led to a tightening in credit conditions.

Economists polled by Reuters had forecast the non-manufacturing PMI decreasing to 54.5. Despite the pullback in growth in the services sector, Anthony Nieves, chair of the ISM Services Business Survey Committee noted that “the majority of respondents report a positive outlook on business conditions.”

The PMI remains above the 49.9 level which the ISM says over time indicates growth in the overall economy. Nevertheless, the softer-than-expected reading, coming on the heels of continued weakness in manufacturing activity last month, increases the risk of a recession this year.

The ISM reported on Monday that its manufacturing PMI fell in March to the lowest level since May 2020. It was the first time since 2009 that all subcomponents of the manufacturing PMI fell below the 50 threshold.

Thirteen services industries reported growth, including arts, entertainment and recreation, accommodation and food services, public administration and mining as well as utilities, construction and information.

Finance and insurance, wholesale trade and retail trade were among the five industries reporting a decline. The services sector is being supported by consumers switching spending from goods, which are typically bought on credit.

The Fed last month raised its benchmark overnight interest rate by a quarter of a percentage point, but indicated it was on the verge of pausing further rate hikes due to financial market turmoil. The U.S. central bank has hiked its policy rate by 475 basis points since last March from the near-zero level to the current 4.75%-5.00% range.

U.S. stocks were trading lower. The dollar rose against a basket of currencies. U.S. Treasury yields fell.

TRADE DEFICIT WIDENS

While accommodation and food services businesses reported that “traffic is recovering and nearly flat,” they added “we are optimistic about the coming months.” Construction businesses described sales as continuing to rise “even as interest rates moderately increase.”

Businesses in the information sector said the “slowdown in the economy is leading to reduced expenditure amounts,” while healthcare and social assistance firms said “the near-term forecast is optimistic,” despite labor shortages and inflation leading to higher operating costs.

The survey’s gauge of new orders received by services businesses dropped to 52.2 last month from 62.6 in February. Twelve industries reported growth in orders and comments from businesses included “increased guest traffic over last month,” and “placing orders for the second half of year.”

With demand cooling, services sector inflation continued to subside, though it remains elevated. A measure of prices paid by services industries for inputs fell to 59.5, the lowest reading since July 2020, from 65.6 in February.

The services sector is now at the heart of the fight against inflation as services prices tend to be stickier and less responsive to interest rate increases.

Some economists view the ISM services prices paid gauge as a good predictor of personal consumption expenditures (PCE) inflation. The Fed, which has a 2% inflation target, tracks the PCE price indexes for monetary policy.

Last month’s slowdown in prices paid by services businesses also reflected a continued improvement in supply.

The survey’s measure of services industry supplier deliveries fell to 45.8 from to 47.6 in February. A reading below 50 indicates faster deliveries.

Services sector employment growth also moderated. The survey’s measure of services industry employment fell to 51.3 from 54.0 in February.

That somewhat aligned with the ADP National Employment report on Wednesday showing private payrolls increased by 145,000 jobs in March after rising 261,000 in February.

The reports were further evidence that the labor market was cooling. The government reported on Tuesday that there were 9.9 million job openings at the end of February, the lowest level since May 2021. Still, there were 1.7 job openings for every unemployed person in February.

According to a Reuters survey of economists, the government’s closely watched employment report will likely show on Friday that nonfarm payrolls increased by 240,000 jobs in March after rising 311,000 in February. The unemployment rate is forecast unchanged at 3.6%.

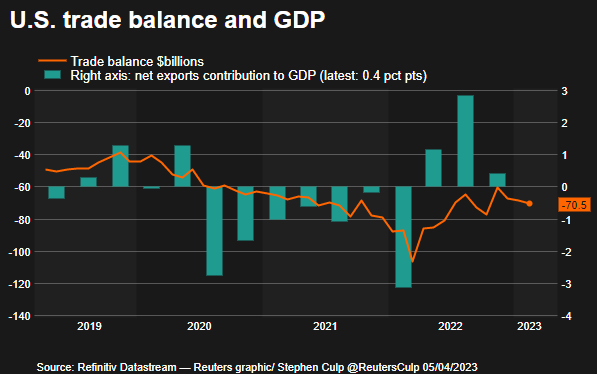

Slowing economic activity was also confirmed by a third report from the Commerce Department showing that the trade deficit widened 2.7% to $70.5 billion in February as exports plunged, outpacing a decline in imports.

That prompted Goldman Sachs to lower its GDP growth estimate for first quarter to a 2.3% annualized rate from a 2.6% pace. A smaller trade gap contributed to the economy’s 2.6% growth pace in the fourth quarter.

“We expect net trade to pose a drag on GDP growth this year,” said Matthew Martin, a U.S. economist at Oxford Economics in New York. “Weak demand overseas and the strong dollar will drag on exports, while soft domestic demand will pull down imports.”

Reporting by Lucia Mutikani; Editing by Chizu Nomiyama and Andrea Ricci

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}