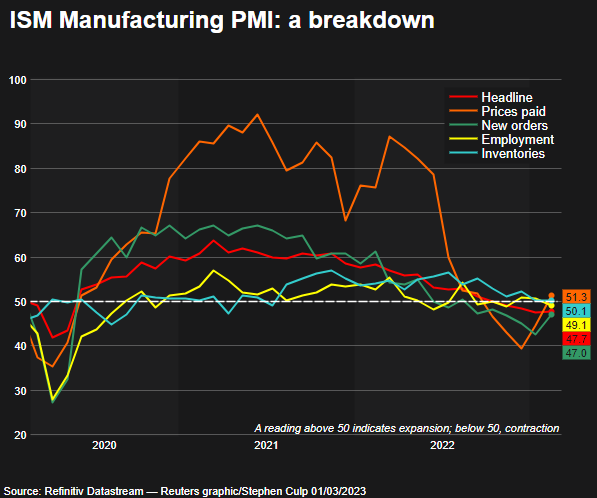

WASHINGTON, March 1 (Reuters) – U.S. manufacturing contracted for a fourth straight month in February, but there were signs that factory activity was starting to stabilize, with a measure of new orders pulling back from a more than 2-1/2-year low.

The Institute for Supply Management survey on Wednesday also showed prices for raw materials increasing last month, which the ISM partly attributed to “a return to more balanced supplier-buyer relationships, as sellers are more interested in filling order books and buyers now see the need to reorder.”

The survey also hinted at buyer resistance to higher prices. Nevertheless, the rebound in prices at the factory gate suggests inflation could remain elevated for a while after monthly consumer and producer prices surged in January.

“Manufacturing continues to contract but not at a sufficiently rapid pace to suggest a recession in the overall economy at this point, while prices of raw materials appear to have risen,” said Conrad DeQuadros, senior economic advisor at Brean Capital in New York.

Latest Updates

View 2 more stories

The ISM’s manufacturing PMI edged up to 47.7 last month from 47.4 in January. The small rise was the first in six months. Economists polled by Reuters had forecast the index would increase to 48.0. A PMI reading below 50 indicates contraction in manufacturing, which accounts for 11.3% of the U.S. economy.

Only four industries, including transportation equipment and electrical equipment, appliances and components, reported growth last month. Paper products, textile mills, furniture and related products as well as nonmetallic mineral products, computer and electronic products were among the 14 reporting contraction.

Stocks on Wall Street were trading lower as traders raised bets that the Federal Reserve would continue to hike interest and keep them at a higher level for a while. The dollar fell against a basket of currencies. U.S. Treasury yields rose.

WORST BEHIND

But the worst could be over for manufacturing. So-called hard data on factory production was solid in January, while business spending on equipment appeared to have rebounded at the start of the first quarter. Comments from some manufacturers in the ISM survey were supportive of this thesis.

Makers of computer and electronic products reported a “good start to the year for bookings.” Transportation equipment manufacturers said “sales remain solid, and most assembly plants are running at capacity.” Primary metals producers described business conditions as “still strong” but noted that “inventory has exceeded our planned levels.”

Food manufacturers, however, said they expected “the first half of 2023 in the U.S. to be slower than the second half.”

With odds increasing that the Fed could keep raising rates into summer, a turnaround in manufacturing is unlikely.

The U.S. central bank has raised its policy rate by 450 basis points since last March from the near-zero level to a 4.50%-4.75% range. Two additional 25-basis-point rate hikes in March and May are expected, though financial markets are betting on another increase in June.

Manufacturing is also being undermined by the dollar’s past appreciation against the currencies of the United States’ main trade partners and softening global demand.

The ISM survey’s forward-looking new orders sub-index improved to 47.0 last month from 42.5 in January, which was the lowest reading since May 2020. Timothy Fiore, chair of the ISM Manufacturing Business Survey Committee, said “new order rates remain sluggish due to buyer and supplier disagreements regarding price levels and delivery lead times.”

This suggests buyers were pushing back at some of the price increases from their suppliers. Walmart Inc (WMT.N) last month warned major packaged goods makers that it could not longer stomach their price hikes.

There was also an improvement in order books, though the backlog of unfinished work remained low. The survey’s measure of supplier deliveries was little changed at 45.2, the fastest supplier delivery performance since March 2009. A reading below 50 indicates faster deliveries to factories.

Stretched supply chains early in the COVID-19 pandemic were one of the major drivers of inflation last year. Despite improving supply and softening demand, inflation flared up.

The ISM survey’s measure of prices paid by manufacturers rebounded to 51.3 in February from 44.5 in January, breaking above the 50 mark for the first time in five months.

“This is a potential concern to the extent that it signals that recent economic resilience is putting renewed upward pressure on inflation,” said Andrew Hunter, deputy chief U.S. economist at Capital Economics. “But that index is still consistent with a sharp fall in the headline CPI rate.”

Its gauge of factory employment fell to 49.1 from 50.6 in January. But that measure, which has swung up and down, has not been a good predictor of manufacturing payrolls in the government’s closely watched employment report. Factory payrolls have mostly grown at a solid clip.

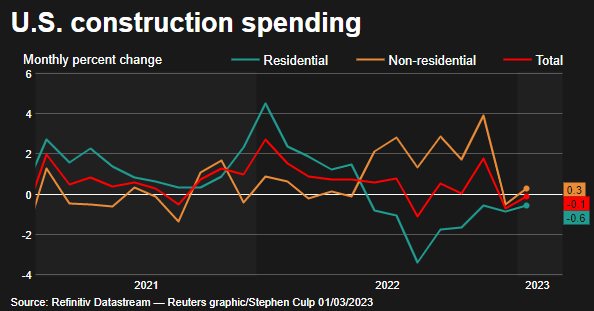

Other data from the Commerce Department showed construction spending dipping 0.1% in January as investment in single-family homebuilding continued to decline. The housing market has been hammered by the Fed’s aggressive monetary policy tightening.

Reporting by Lucia Mutikani; Editing by Chizu Nomiyama, Paul Simao and Andrea Ricci

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}