WASHINGTON, Oct 2 (Reuters) – U.S. manufacturing took a step further towards recovery in September as production picked up and employment rebounded, according to a survey on Monday that also showed prices paid for inputs by factories falling considerably.

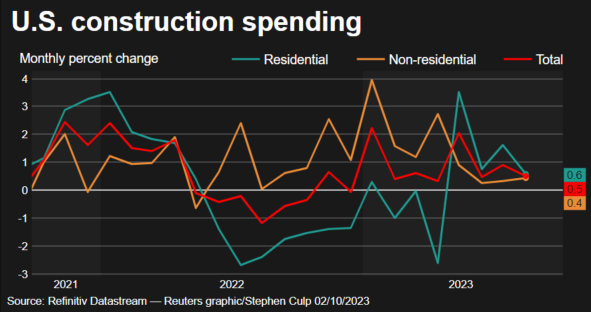

The third straight month of improvement reported by the Institute for Supply Management (ISM) strengthened economists’ expectations that economic growth accelerated in the third quarter, despite higher interest rates. That was reinforced by a Commerce Department report showing construction spending was solid in August, driven by the building of houses and factories.

The economy’s continued resilience raises hope that a recession could be averted in the near term.

“The soft landing narrative still holds as we enter the final quarter of 2023,” said Jennifer Lee, a senior economist at BMO Capital Markets in Toronto.

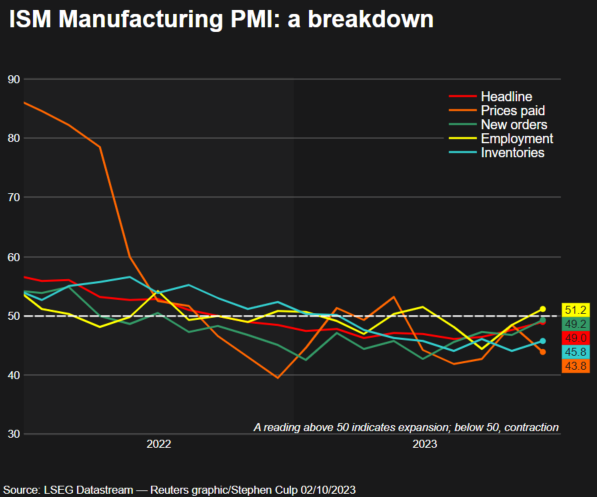

The ISM said that its manufacturing PMI increased to 49.0 last month, the highest reading since November 2022, from 47.6 in August. Still, September marked the 11th straight month that the PMI remained below 50, which indicates contraction in manufacturing. That is the longest such stretch since the 2007-2009 Great Recession.

Economists polled by Reuters had forecast the index edging up to 47.7. Last month’s rise pulled the PMI above the 48.7 level that the ISM says over time indicates an expansion of the overall economy. Growth estimates for the third quarter are as high as a 4.9% annualized rate. The economy grew at a 2.1% pace in the April-June quarter.

A survey from S&P Global also struck a fairly optimistic note on manufacturing.

Five manufacturing industries in the ISM survey reported growth last month, including textile mills and primary metals.

Among the 11 industries reporting contraction were computer and electronic products, machinery, as well as electrical equipment, appliances and components.

Comments from respondents in the survey remained mixed. Makers of transportation equipment said “orders and production remain steady, and we are maintaining a healthy backlog.”

Manufacturers of miscellaneous goods said they were keeping an eye on the Panama Canal drought, U.S.-China relations, and the impact the United Auto Workers strike on the supply chains. They, however, viewed overall conditions as “stable.”

Apparel, leather and allied products makers described markets as “soft,” while primary metals producers said “business conditions and market demand remain strong,” and they “projected to be at capacity in the next 12 months.” Petroleum and coal products manufacturers said “a recession feels imminent.”

Stocks on Wall Street were higher. The dollar rose against a basket of currencies. U.S. Treasury prices fell.

NEW ORDERS IMPROVE

While the PMIs and other business surveys have painted a grim picture of manufacturing, which accounts for 11.1% of the economy, so-called hard data have suggested that the sector continues to chug along.

Orders for long-lasting manufactured goods increased 4.2% year-on-year in August and business spending on equipment appears to have remained strong in the third quarter after rebounding in the April-June period.

The ISM survey’s forward-looking new orders sub-index increased to 49.2 last month from 46.8 in August. With new orders improving, production at factories accelerated. The production index increased to 52.5 from 50.0 in the prior month.

But the average commitment lead time for capital expenditures increased by two days.

“This compares to an average of 139 days in over the period 2015-2019, indicating that it still takes a long time to order, obtain, and install business equipment,” said Conrad DeQuadros, senior economic adviser at Brean Capital in New York.

Though backlog orders shrank, inventories at factories and their customers remained very low, which should support future production. Delivery performance of suppliers to manufacturers improved for the 12th straight month. This, together with still- sluggish demand, helped to depress prices for factory inputs.

The survey’s measure of prices paid by manufacturers fell to 43.8 from 48.4 in August. This bodes well for goods disinflation, but the striking auto workers could boost prices of motor vehicles. Rising energy prices could drive inflation higher, but also support manufacturing.

“High oil prices may present headwinds for some parts of the economy and not every manufacturer celebrates higher prices for crude, but on balance high oil prices are associated with brisk activity in manufacturing,” said Tim Quinlan, a senior economist at Wells Fargo in Charlotte, North Carolina.

Factory employment improved further after slumping to three-year lows in July. The survey’s gauge of factory employment rose to 51.2 last month from 48.5 in August.

“Attrition remained the primary source of head-count reductions, but hiring freezes were more prevalent,” said Timothy Fiore, Chair of the ISM Manufacturing Business Survey Committee.

A separate report from the Commerce Department showed construction spending increased 0.5% in August after rising 0.9% in July, lifted by outlays on single- and multi-family housing. But with mortgage rates near 23-year highs, momentum could slow.

Construction spending jumped 7.4% on a year-on-year basis in August. Spending on private construction projects rose 0.5%, with investment in residential construction advancing 0.6% after increasing 1.6% in the prior month. Private construction spending gained 1.2% in July.

Spending on private non-residential structures like factories climbed 0.3% in August. Spending on manufacturing construction projects shot up 1.2% amid efforts by the Biden administration to bring semiconductor manufacturing back to the United States.

Reporting By Lucia Mutikani; Editing by Andrea Ricci and Aurora Ellis

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}