US jobs report weaker than expected; UK economy ‘flirting with recession’, economists say –as it happened | Business

US jobs report weaker than expected

The US economy added 150,000 jobs in October, fewer than expected, and previous months were revised lower, suggesting the economy is not quite as strong as thought.

Economists had expected 180,000 new jobs. In September, employers hired 297,00 more people, less than the 336,000 previously reported, and in August, there were 165,000 new private sector jobs, revised down from 227,000.

The unemployment rate ticked up to 3.9% from 3.8% in September.

The dollar index, which measures the greenback against a basket of other major currencies, fell to a 10-day low.

Key events

Closing summary

The US added another 150,000 jobs in October, fewer than expected, amid signs that the white-hot US jobs market is cooling. The unemployment rate rose to 3.9% from 3.8% in September.

Economists had been expecting the US to add 180,000 jobs over the month. The pace of job growth slowed sharply from September when the economy added a revised 297,000 – a still impressive figure and far higher than had been expected.

Our other main stories today:

Thank you for following us this week. Have a lovely weekend. We’ll be back next week. Take care – JK

UK shopper numbers down 5.7% in October, says BRC

The number of people who were out shopping in October fell sharply last month, as heavy rain (Storm Babet) kept consumers at home.

According to the latest data from the British Retail Consortium, retail footfall dropped 5.7% year-on-year in October, worsening from September’s 2.9% decline.

Within that, high street footfall fell 4.6%, while retail parks and shopping centres posted declines of 4.3% and 7.3% respectively.

Helen Dickinson, the BRC’s chief executive said:

Umbrellas were up as heavy rainfall descended across the UK in October, leading many shoppers to stay at home.

As inflationary pressures on households begin to ease, some people are shopping around slightly less, braving the rain only to make their final purchases.”

While consumer confidence may be higher than 2022, it is still very weak. The economic landscape remains tough, with input prices and cost pressures above normal levels.

Bank of England’s Pill: Inflation won’t necessarily fall fast as demand slows

Britain’s stubbornly high inflation will not necessarily fall quickly as demand slows, according to the Bank of England’s chief economist Huw Pill.

He spoke a day after the central bank held its benchmark interest rate at 5.25% (the highest since the 2008 financial crisis) for a second meeting in a row.

Pill said:

The overall judgments of the MPC has a little bit switched from being associated with demand factors to be more associated with supply factors.

We can be less sanguine about the idea that the slowing of demand, the slowing of activity that we are seeing will lead to inflation returning to target.

Falling profitability of UK firms casts doubt on ‘greedflation’

Phillip Inman

Official figures show the profitability of UK companies declined in the second quarter of the year, indicating that fears of price gouging to boost profits margins are misplaced.

The net rate of return for private non-financial corporations (PNFCs), which excludes oil and gas firms operating in the North sea, was 9.6% in the three months from April to the end of June this year, down from a revised estimate of 10.7% in the first quarter.

The net rate of return is a measure of company profitability used by the ONS. A breakdown of the figures that shows the fortunes of services and manufacturing firms follows the same pattern.

Company profitability was almost identical in 2019, before the pandemic, revealing that with a few minor ups and downs in the last three years, companies have maintained their profit margins.

And these ups and downs were mostly related to government energy subsidies, which have reduced this year and lowered profit margins previously boosted by subsidies.

This situation contrasts with the average household, which have also been helped by energy subsidies, but suffered low wage rises from these same companies (their employers) and seen disposable incomes sink during the same period.

US services growth slows in October

More data from the US: The Institute for Supply Management’s services index fell to a five-month low of 51.8 in October, from 53.6 in September, indicating slower growth.

Any reading above 50 indicates growth.

This is more evidence that economic growth is slowing after a blockbuster third quarter, said Paul Ashworth, chief North America economist at Capital Economics.

Unlike the renewed slump in the manufacturing index, however, the dip in the aggregate services index was driven not by a slump in new orders, but rather new-found weakness in current business activity, employment and inventories.

The supplier deliveries index also dropped back further, indicating that supply shortages are largely a thing of the past. In contrast, the new orders index strengthened to 55.5, from 51.8.

Cameron Misson, economist at the UK think tank Centre for Economics and Business Research, has also looked at the US jobs report.

Today’s data may be an early signal that the US labour market is cooling, reinforcing the Federal Reserve’s decision to hold interest rates at its November meeting. Subdued non-farm payroll growth, a slight uptick in unemployment, and slowing wage growth are all evidence the central bank’s interest rate hikes are having the desired effect of slowing economic activity.

However, wage and price inflation remain too high, so expect interest rates to remain elevated for an extended period of time.

The Fed kept interest rates unchanged on Wednesday and along with other major central banks such as the Bank of England, is widely expected to keep borrowing costs at the current level for some time.

Fed chair Jerome Powell said then that robust jobs growth showed more people were coming back into the workforce, and an uptick in immigration. “That’s a big supply-side gain that is really helping the economy.”

Treasury secretary Janet Yellen has echoed this sentiment, telling the Financial Times in an interview last month that growth was a “positive, not a negative” that reflected “more people wanting to work and finding jobs”.

Wall Street has opened higher: the Dow Jones rose nearly 150 points or 0.4% to 33,988. The S&P 500 added 16 points, or 0.4%, to 4,334 while the Nasdaq gained nearly 70 points, or 0.5%, to 13,362 at the opening bell.

Wall Street shares are expected to rise at the open, after the weaker than expected non-farm payrolls data, which showed slowing job growth and a surprise uptick in the unemployment rate to 3.9%. This boosted investor expectations that the Federal Reserve won’t hike interest rates again.

You can find the US Labor Department figures here.

Jay Hatfield, chief executive at Infrastructure Capital Management, said:

It is consistent with the views of the market that the job market and the economy is decelerating and that’s going to keep the Fed on hold and will cause central banks next year to cut rates.

Here’s more instant reaction. Daniel Casali, chief investment strategist at the wealth management group Evelyn Partners, said:

While there is increasing evidence that US job creation is slowing, it is unlikely to change the Fed’s plan to keep interest rates ‘higher for longer’ to address inflation in the near term.

Nevertheless, overall employment is still expanding by around 2% per annum and that should provide support for consumption growth. Other measures of labour activity are also indicative of a relatively healthy labour market. For instance, weekly initial job claims are a timely signal for the unemployment trend. Given this was recently reported at an historically low level, this implies there are fewer workers seeking unemployment benefits.

Similarly, the September reading for job openings (from the JOLTS survey) came in at 9.6 million, versus the pre-pandemic level of around 7m at the end of 2019. This shows that firms are still looking to hire. Indeed, the Manpower survey rebounded in the fourth quarter to show that a net 36% of firms were planning to hire in the 3 months, compared to 20% at the end of 2019.

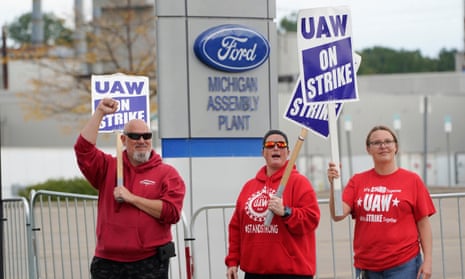

Importantly, average hourly earnings from the payroll report are slowing and that should give the Fed some comfort that wage-driven inflation is coming under control. Though recent bumper wage deals agreed between the United Auto Workers’ labour union and major auto manufacturers is a risk to the overall inflation outlook.

US factory jobs declined by 35,000 last month while government jobs increased by 51,000. There were also job gains in health care and social assistance.

Andrew Hunter, deputy chief US economist at Capital Economics, said:

The muted 150,000 gain in non-farm payrolls in October is another sign that the economy’s strength in the third quarter is likely to unwind in the fourth. With wage growth also continuing to slow, it is increasingly hard to imagine the Fed hiking interest rates any further.

Admittedly, recent strike action hit payrolls again last month, with 33,200 UAW (United Auto Workers) workers walking out during the October survey period. That helps explain the 35,000 fall in manufacturing payrolls, which will be reversed in November with the autoworkers’ strike now over.

That said, strikes can’t explain the declines in employment in transportation & warehousing, information and finance. Furthermore, payrolls are still being supported by growth in the non-cyclical government and health care & social assistance sectors – excluding those, payrolls rose by just 22,000 last month.

Finally, after a blip in September, the persistent pattern of downward revisions to past months has returned – with August and September payroll gains revised down by a cumulative 101,000.

The UAW union struck deals with the car manufacturers Ford, General Motors and Stellantis in the past week, ending the car worker strikes.

US government bonds rallied after the data, which showed employers hired fewer people than expected in October.

This pushed bond yields lower (yields move inversely to prices). The yield, or interest rate, on benchmark 10-year Treasuries fell 11 basis points to 4.55%, the lowest in three weeks. Two-year yields dropped 10 bps to 4.87%, the lowest since early September.

European bonds also rallied, as did sterling and the euro, rising 0.8% against the dollar to $1.2305 and $1.0714 respectively.