Currency is traditionally the largest liability of a central bank and today accounts for 36% of the Federal Reserve’s liabilities, or $1.59 trillion.1 The Fed supplies currency to meet demand, so changes in the demand for currency will be an important determinant of how the Fed’s balance sheet evolves in the future. In this Chicago Fed Letter, we examine currency demand around the world and over time to learn about the range of possibilities for how U.S. currency demand might change. We then project currency demand over the next decade in several illustrative scenarios.

An international perspective

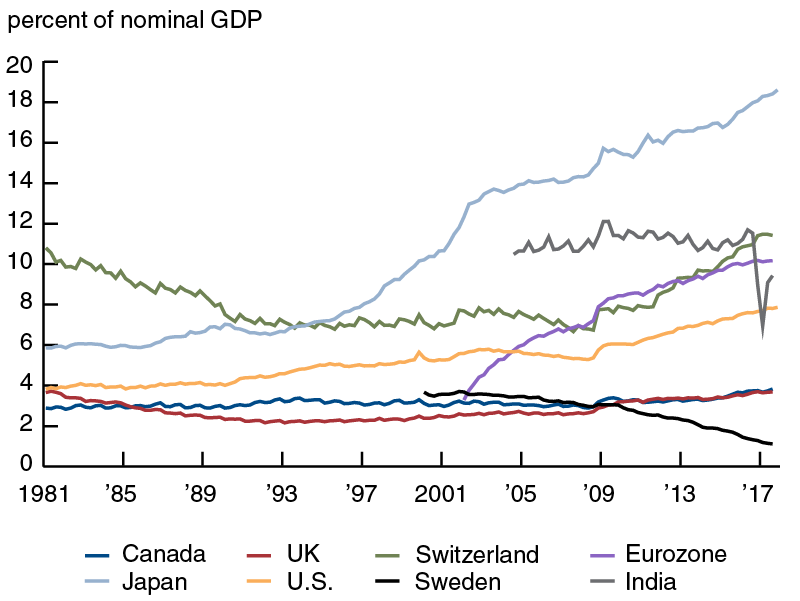

Figure 1 shows the ratio of currency to gross domestic product (GDP) over time for seven countries (Canada, India, Japan, Sweden, Switzerland, the United Kingdom, and the United States) and the eurozone. The relationship between currency demand and the size of an economy is not entirely clear-cut. We might expect currency use to rise with GDP, because a larger economy will have more transactions and thus more need for currency. But in fact, the ratio varies both between countries and over time for a given country. These variations help reveal some of the main determinants of currency demand.

1. Banknotes in circulation

One important factor affecting currency demand is the adoption of alternative technologies for making payments. In Japan, a largely cash-based economy where the use of credit cards and other electronic payments is relatively uncommon, currency demand now stands at nearly 19% of GDP—the highest of any country for which the Bank for International Settlements collects statistics.2 But in Sweden, demand for currency has plummeted in recent years as electronic payment technologies have replaced cash. The large differences across countries suggest that the adoption of new payment technologies is likely to be at least as important as whether the technology exists: People know how to use credit and debit cards around the world, but they have been much more eager to switch to cards in some places than others. Increased use of by-now traditional electronic payment tools, such as credit cards, has been sufficient to dramatically reduce currency demand in countries such as Sweden.3 If cryptocurrencies such as Bitcoin were ever to become widely used, the demand for cash could fall further.

Another important determinant of currency demand is the extent to which a country’s currency is used abroad. The U.S. and Canada have relatively similar economies, yet currency is now 8% of GDP in the U.S. and only 4% of GDP in Canada. The gap has risen over the three decades shown in figure 1, which some analysts argue is related to the increasing use of U.S. dollars in other countries.

Government policies can also cause sharp changes in currency relative to GDP, as can be seen in the case of India. India’s share of currency to GDP fell sharply after November 8, 2016, when the government announced that existing 500 and 1,000 rupee notes would no longer be valid and that the old notes needed to be exchanged for new 500 and 2,000 rupee notes.4 The eurozone provides another example of the impact of policy changes—in this case, the introduction of an entirely new currency. Euro coins and bills were first distributed in late 2001 and became legal tender on January 1, 2002, replacing the separate currencies of the countries that make up the eurozone. But the quantity of euro currency in circulation that first day was less than people ultimately demanded; as more euros were printed and as the new currency gained public acceptance, the amount in circulation grew.

Finally, the trends in figure 1 provide suggestive evidence that interest rates may affect the demand for currency. Currency does not earn interest, while funds held in bank accounts typically do. Thus, when interest rates are low, the opportunity cost of holding currency instead of putting money in the bank is lower, and people may tend to hold more currency. Consistent with this idea, we see in figure 1 that the ratio of currency to GDP has risen since the financial crisis in Switzerland, the U.S., Canada, and the UK as all of those countries’ central banks have set interest rates at their effective lower bounds. And currency use began rising sharply in the mid-1990s in Japan, when that country’s interest rates fell to near zero.5

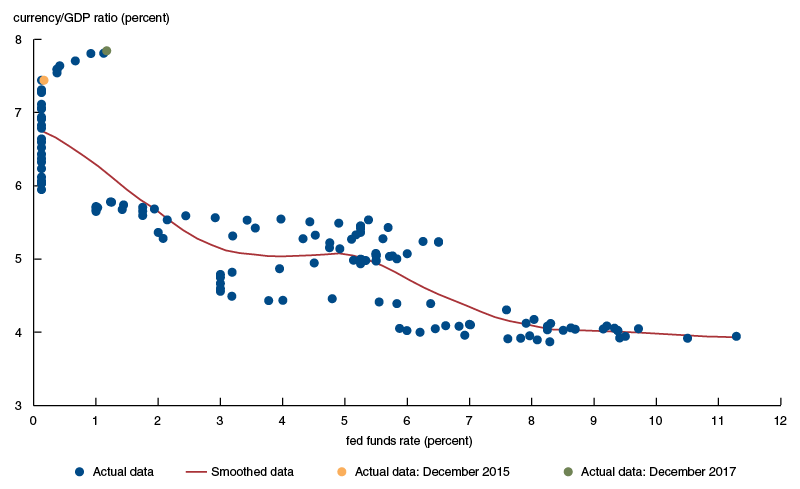

2. Fed funds rate and U.S. currency-to-GDP ratio

Sources: Board of Governors of the Federal Reserve System and U.S. Bureau of Economic Analysis via Haver Analytics.

Low rates, lots of cash

Figure 2 examines the relationship between interest rates and currency use for the U.S. The figure plots quarterly data on the ratio of currency to GDP on the vertical axis against the target federal funds rate set by the Federal Open Market Committee (FOMC) on the horizontal axis. Each dot shows data from a different quarter, and the solid line smooths out the dots to show the average relationship between interest rates and currency. The overall negative relationship is clear—a rise in the fed funds rate from 0% to 2% has been associated, on average, with a 1 percentage point drop in the ratio of currency to GDP.

However, changes in factors other than interest rates may also have contributed to the relationship shown in the figure. For example, interest rates have generally been falling over the period shown in the data, while foreign demand for U.S. currency appears to have risen during that period for reasons other than interest rates. Thus, some of the apparent association between low interest rates and high currency demand may not actually be a function of interest rates. For this reason, we cannot be sure that future changes in interest rates would cause currency demand to change by exactly the amount suggested by the figure.

Indeed, the FOMC’s most recent series of rate increases is an exception to the typical relationship. From December 2015 to December 2017, the FOMC raised its target for the fed funds rate by 1 percentage point. Yet the figure shows that the ratio of currency to GDP rose by 0.4 percentage points over that time, indicating that influences other than interest rates have significantly affected the demand for currency.

Exporting dollars

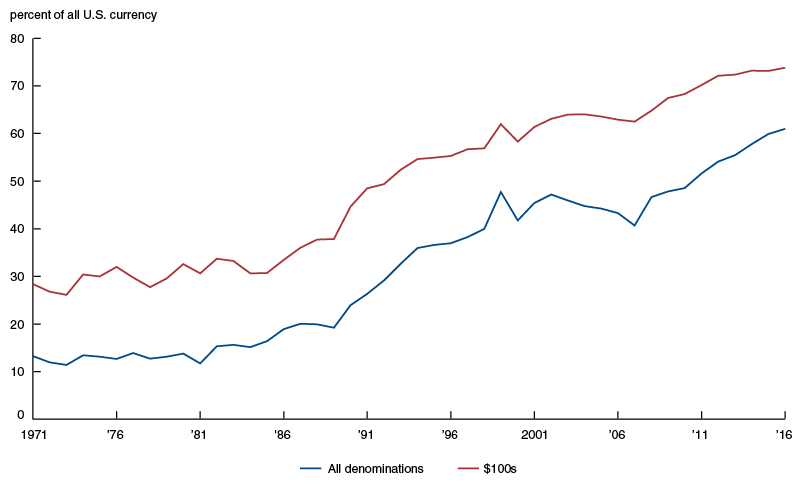

People in other countries, especially countries with unstable financial systems, often use U.S. financial assets as a safe haven. U.S. currency is a particularly attractive asset for people who want a stable currency for their day-to-day transactions, as well as people who are engaged in illicit activities and do not want to put their money in a place where it would be visible to authorities, such as a financial security or bank account. As a result, demand for U.S. currency overseas is substantial. Much of this demand is for $100 bills, whose high value makes them more convenient for transporting large sums of cash.

Figure 3 shows estimates of the fraction of all U.S. currency and of $100 bills held overseas from Federal Reserve Board economist Ruth Judson.6 Paper currency is not easily tracked once the central bank distributes it, so the amount of U.S. currency abroad must be estimated. Judson’s estimates assume that, in the absence of foreign demand, the relationship between currency use and GDP in the U.S. would be the same as in Canada. In other words, she assumes that the higher ratio of currency to GDP in the U.S. is due to foreign demand. The estimates suggest that more than 60% of all U.S. bills and nearly 80% of $100 bills are now overseas—up from 15% to 30% around 1980. In her research, Judson has found that economic and political instability contribute to this demand.7

Future scenarios

The factors we’ve assessed suggest that to estimate future U.S. currency demand, we need to consider at least four key variables: the size of the economy, the adoption of new payment technologies that replace currency, changes in interest rates, and changes in foreign demand. As of March 14, 2018, U.S. currency outstanding was $1.59 trillion. Figure 4 shows estimates for what currency outstanding might be ten years from now, in 2028, under three scenarios that take these variables into account.

3. Shares of U.S. currency abroad

In scenario 1, our baseline or middle scenario, we assume that the use of payment technologies doesn’t change and that demand for U.S. currency, both at home and abroad, is driven by changes in the U.S.’s nominal GDP and interest rates. The FOMC’s median projection in March 2018 was that the federal funds rate target in the long run will be 2.9%, up from a range of 1.50% to 1.75% today.8 Figure 2 shows that such a rise in the fed funds rate has historically been associated with reducing the ratio of domestic currency to GDP by about 1.03 percentage points. That would reduce the currency/GDP ratio to 6.92%, compared with 7.95% today. Combined with the 3.9% average annual growth rate of nominal GDP projected by the Congressional Budget Office (CBO) in June of last year,9 this implies U.S. currency demand of $2 trillion ten years from now. The rising interest rates in this scenario mean that total currency demand grows more slowly than GDP and is $298 billion lower than it would be if interest rates were to stay at their March 2018 levels. As a result, in this scenario currency demand is somewhat lower than staff projections from the Fed’s Board of Governors that assume currency will grow proportionately to GDP.10

But other outcomes are possible. As figure 1 shows, the ratio of currency to U.S. GDP has grown steadily over time. From the end of 2014 through the end of 2017, the ratio grew by an average of 0.06 percentage points per quarter. This might seem like a small change each quarter, but if that rate of change were to continue for ten years, the ratio of currency to GDP would reach 10.2% a decade from now. Combined with the CBO’s projection for GDP growth and assuming that interest rates do not rise, currency demand would then reach $2.95 trillion. This number forms scenario 2, our high scenario for currency demand.

In scenario 3, our low scenario, we assume that interest rates normalize and that rapid adoption of new payment technologies both in the U.S. and abroad causes the ratio of total currency to GDP to fall by a factor of four, just as it did in Sweden. This leaves the ratio of currency to GDP at about 1.73%, and with the CBO’s path for GDP growth, total currency demand would be just $501 billion. In this scenario, just over $1 trillion in currency would actually be returned to the Fed.

4. Scenarios for future U.S. currency demand

|

Scenario |

|

in 2028 (%) |

in 2028 ($ billions) |

|

1 – Baseline |

Rising interest rates reduce currency/ |

|

|

|

2 – High |

Foreign demand continues to increase |

|

|

|

3 – Low |

Rising interest rates and new payments |

|

|

|

Memo: Current data |

|

|

|

Conclusion

While our low and high scenarios are perhaps unlikely, they illustrate the wide range of possible outcomes for currency demand and, as a result, for the future size of the currency component of the Fed’s balance sheet. Projecting the demand for U.S. currency is challenging and requires a number of assumptions. Currency demand depends on how quickly the economy grows, on interest rates, on the invention and adoption of new payments technologies, and on whether people in other countries continue to see U.S. dollar bills as a useful asset—all factors that are, to say the least, uncertain.

1 We thank Michael Locke for excellent research assistance. Our recent Chicago Fed Letter describing Federal Reserve liabilities is available online. Crossref

2 Bank for International Settlements, Committee on Payments and Market Infrastructures, 2016, Statistics on Payment, Clearing and Settlement Systems in the CPMI Countries: Figures for 2015, Basel, Switzerland, December.

3 Liz Alderman, 2015, “Where even banks don’t accept cash anymore,” New York Times, December 27, p. A1.

4 More information is available online.

5 Some of the increase in the ratio of currency to GDP when interest rates are low reflects low GDP growth during those periods.

6 Ruth Judson, 2017, “The death of cash? Not so fast: Demand for U.S. currency at home and abroad, 1990-2016,” paper presentation at the Deutsche Bundesbank International Cash Conference 2017, War on Cash: Is There a Future for Cash?, Island of Mainau, Germany, April 26, available online.

7 Ruth Judson, 2012, “Crisis and calm: Demand for U.S. currency at home and abroad from the fall of the Berlin Wall to 2011,” International Finance Discussion Papers, Board of Governors of the Federal Reserve System, No. 2012-1058, November.

10 Erin E. Syron Ferris, Soo Jeong Kim, and Bernd Schlusche, 2017, “Confidence interval projections of the Federal Reserve balance sheet and income,” FEDS Notes, Board of Governors of the Federal Reserve System, January 13.

{kind=link}