WASHINGTON, Dec 15 (Reuters) – U.S. retail sales fell more than expected in November, but consumer spending remains supported by a tight labor market, with the number of Americans filing for unemployment benefits decreasing by the most in five months last week.

The biggest decrease in retail sales in 11 months reported by the Commerce Department on Thursday was likely payback after sales surged in October as Americans started their holiday shopping early to take advantage of discounts by businesses desperate to clear excess inventory.

Economists also noted that goods prices tumbled in November, which could have weighed on retail sales last month. The discounts by retailers were also probably a drag on the dollar value of sales. Retail sales are mostly goods and are not adjusted for inflation.

“It is hard to know at this point if the November weakness represented a fundamental change in the trend or reflected some inevitable cooling following a strong run for real spending into October, or some combination, but for now we are not particularly alarmed by the November drop in retail spending,” said Daniel Silver, an economist at JPMorgan in New York.

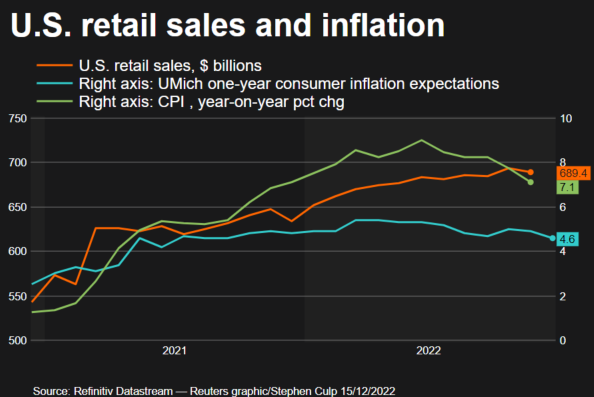

Retail sales fell 0.6% last month, the biggest drop since December 2021, after an unrevised 1.3% jump in October. Economists polled by Reuters had forecast sales dipping 0.1%. Retail sales increased 6.5% year-on-year in November.

Last month’s decrease in sales also reflected the fading boost from one-time tax refunds in California, which saw some households receiving as much as $1,050 in stimulus checks in October, and Amazon’s second Prime Day. Spending is also rotating back to services.

“Accounting for goods disinflation and strong October spending, it’s premature to call this a sign of collapsing consumer demand,” said Will Compernolle, a senior economist at FHN Financial in New York. “Most likely, holiday spending is earlier this year, reflecting discounting, availability, and frustration over long shipping delays a year ago.”

Sales at auto dealers fell 2.3% as motor vehicles remain in short supply. Receipts at service stations dipped 0.1%, reflecting lower gasoline prices. Online retail sales decreased 0.9%, which was at odds with reports of strong Black Friday sales. Furniture stores sales dropped 2.6%.

Sales at food services and drinking places, the only services category in the retail sales report, increased 0.9%. Electronics and appliance store sales fell 1.5%. There were also decreases in receipts at general merchandise stores as well as sporting goods, hobby, musical instrument and book stores. Clothing stores sales fell 0.2%.

Nevertheless, the almost broad weakness in sales suggests higher borrowing costs and the threat of an imminent recession are hurting household spending. Savings, which have helped to cushion consumers against inflation, are dwindling. The saving rate was at 2.3% in October, the lowest since July 2005. But economists also expect slowing inflation to support spending.

The Federal Reserve on Wednesday raised its policy rate by half a percentage point and projected at least an additional 75 basis points of increases in borrowing costs by the end of 2023. This rate has been hiked by 425 basis points this year from near zero to a 4.25%-4.50% range, the highest since late 2007.

Stocks on Wall Street were trading lower. The dollar rose against a basket of currencies. U.S. Treasury yields fell.

STRUCTURAL LABOR SHORTAGE

[1/5] A man walks under the rain with his shopping bags as people visit a department store during the holiday season in New York City, U.S., December 15, 2022. REUTERS/Eduardo Munoz

Excluding automobiles, gasoline, building materials and food services, retail sales slipped 0.2%. Data for October was revised lower to show these so-called core retail sales increasing 0.5% instead of 0.7% as previously reported.

Core retail sales correspond most closely with the consumer spending component of gross domestic product. The weakness in core retail sales is likely to be offset by gains in services, keeping consumer spending and the overall economy on a moderate growth path this quarter.

The economy grew at a 2.9% annualized rate in the third quarter after contracting in the first half of the year.

Higher interest rates are pressuring manufacturing. A separate report from the Fed on Thursday showed manufacturing production falling 0.6% in November. Conditions in manufacturing, which accounts for about 11.3% of the economy, are likely to remain weak heading into the new year.

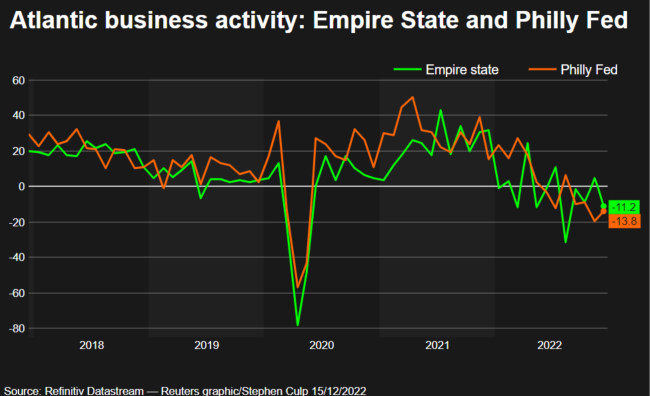

Reports from the New York Fed and Philadelphia Fed showed business conditions in New York state and the mid-Atlantic region remaining depressed in December. But businesses were fairly upbeat about conditions over the next six months.

Despite the growing recession risks spawned by the Fed’s rate hikes, the labor market remains strong.

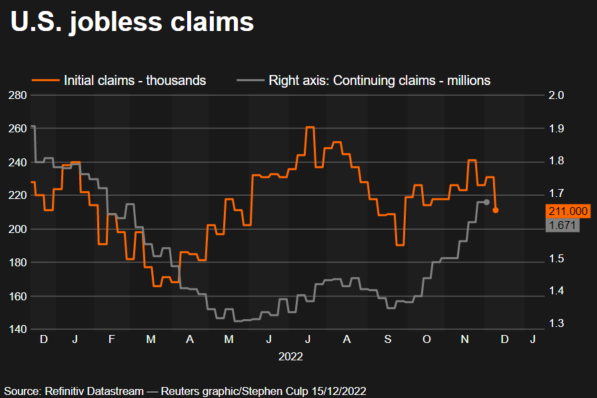

A fifth report from the Labor Department showed initial claims for state unemployment benefits declined 20,000 to a seasonally adjusted 211,000 during the week ended Dec. 10.

Last week’s decrease in claims was the largest since July and pushed them to a three-month low. Economists had forecast 230,000 claims for the latest week. There were large decreases in unadjusted claims in California, New York, Georgia and Texas.

Though claims have swung up and down in recent weeks, they have stayed below the 270,000 threshold, which economists said would raise a red flag for the labor market, despite a wave of layoffs in the technology sector.

Businesses are generally reluctant to lay off workers, having struggled to find labor in the aftermath of the COVID-19 pandemic, a fact that was acknowledged by Fed Chair Jerome Powell on Wednesday.

Powell described the labor market as “extremely tight,” adding “it feels like we have a structural labor shortage out there.” There were 1.7 job openings for every unemployed person in October.

The claims report also showed the number of people receiving benefits after an initial week of aid, a proxy for hiring, rose 1,000 to 1.671 million in the week ending Dec. 3. While that was the highest reading since February, the pace of increase in the so-called continuing claims has slowed from prior weeks.

“While employers may be reluctant to fire workers, they are becoming more cautious about hiring as the economy slows,” said Nancy Vanden Houten, lead U.S. economist at Oxford Economics in New York.

Reporting by Lucia Mutikani; Editing by Chizu Nomiyama and Andrea Ricci

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}