The dollar usually weakens in young bull markets.

It is a good thing currencies don’t have feelings, because if they did, the dollar would be a perpetually sad sack. Up or down, strong or weak, it always seems to inspire gloom. Last year, when it strengthened, pundits warned it would hamper global trade and force other nations—especially in Emerging Markets—to intervene to shore up their currencies and risk over-tightening monetary policy in the process. So now that it is weaker, you might think everyone is breathing a sigh of relief. But you would be wrong. Now, we are told, the dollar signals a declining US economy and impending debt ceiling doom. We think the truth is a lot more simple and benign, rendering the dollar a brick in stocks’ wall of worry.

It is a common—and in our view wrong—belief that long-term currency moves derive from economic conditions. Sometimes the dollar is weak relative to a trade-weighted currency basket during economic expansions, and sometimes it is strong. The same goes for the yen, euro, pound and other major currencies, which makes sense when you remember that currencies trade in pairs. If the dollar has no preset relationship with the economic cycle, then by definition other major currencies can’t, either.

But the dollar does have an interesting relationship with the stock market cycle. As with economic expansions, it is true that the dollar can swing both ways during a bull market. But during bear markets, it usually strengthens. Not because the stronger dollar is causing stocks to drop, but because when financial markets globally look dicey, there tends to be what analysts call a flight to quality. That is, when stocks and other securities are dropping, investors will shift into assets with the most perceived stability and liquidity—which tends to be the good old greenback. Other nations (e.g., Switzerland, the UK) might have similarly stable money, but their capital markets don’t have the depth to absorb the surge in demand. Uncle Sam does, so the dollar usually benefits from the flood of risk-averse investors. Then, as the bear market ends and stocks recover, the dollar often weakens—a byproduct of thawing sentiment.

We think this explains much of last year’s movement. Yes, money moves to the highest-yielding asset, all else equal, and yes, the Fed out-hiked its peers last year. That probably contributed. But global stocks also endured a bear market, which started in early January. The dollar hit a high in late September and retested it several times through early November. Stocks’ low (to date) occurred smack in the middle of that stretch, on October 12. Their ascent since then—and the dollar’s parallel decline—occurred despite continued rate hikes. To us, that suggests sentiment has had an outsized influence over the dollar, and its decline is more about the flight to quality reversing than signaling economic risk.

A picture is worth a thousand words, so here are three showing how the dollar behaved during and just after the most recent three bear markets.

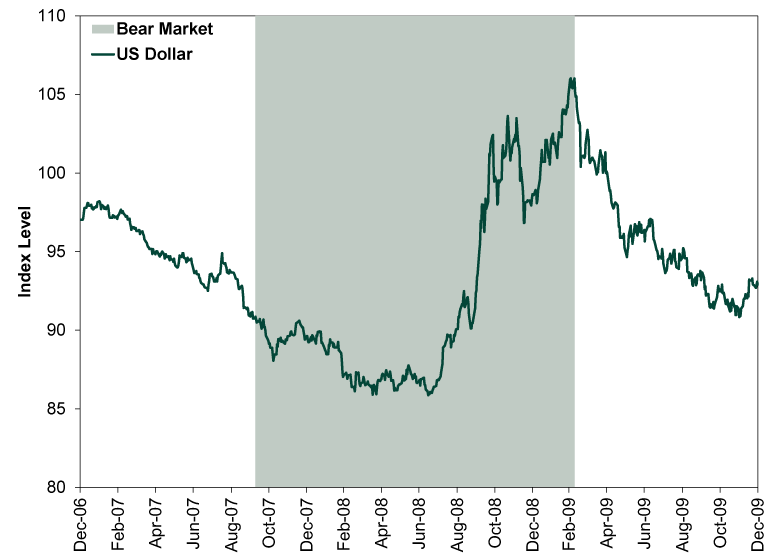

Exhibit 1: The Dollar Strengthened in 2008 …

Source: FactSet, as of 5/1/2023. Nominal trade-weighted US dollar index (broad), 12/31/2006 – 12/31/2009.

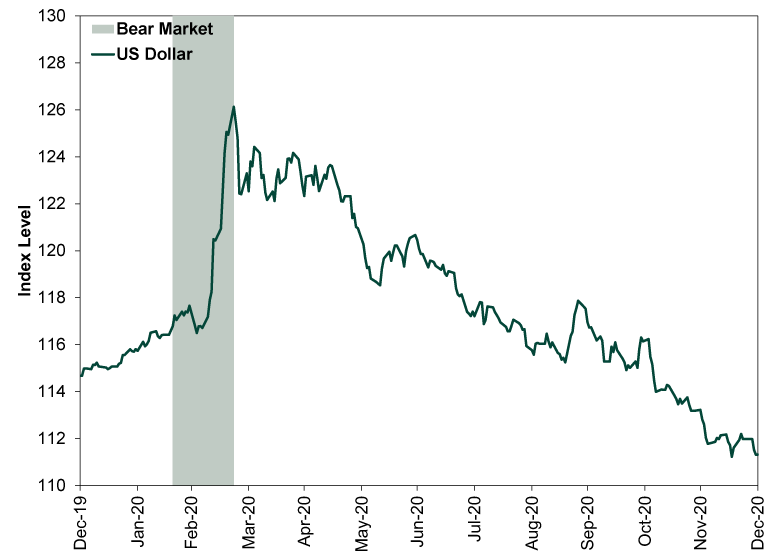

Exhibit 2: … and During the COVID Lockdown Bear Market …

Source: FactSet, as of 5/1/2023. Nominal trade-weighted US dollar index (broad), 12/31/2019 – 12/31/2020.

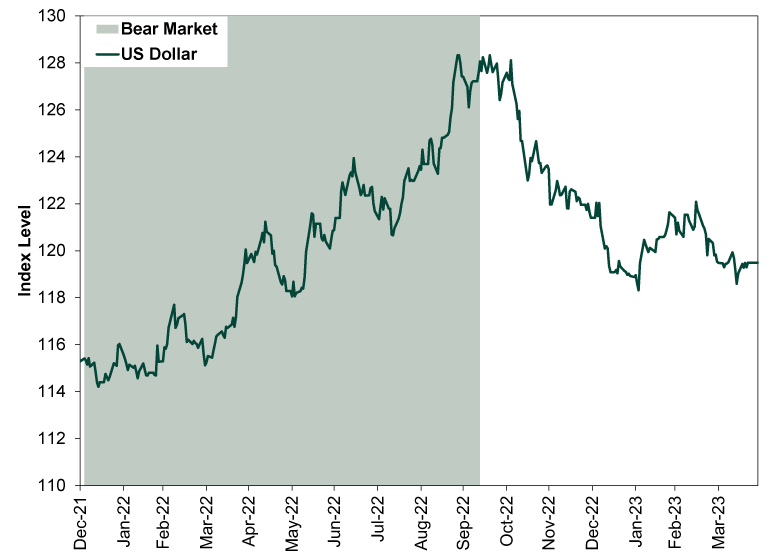

Exhibit 3 … and During 2022’s Bear Market

Source: FactSet, as of 5/1/2023. Nominal trade-weighted US dollar index (broad), 12/31/2021 – 4/30/2023.

See? Normal behavior. But people always fear it, which we think speaks to early bull market pessimism. Usually, as stocks recover, people hunt the proverbial next shoe to drop. The dollar, with all of its entangled emotions, is an easy target. It provides a handy way to argue stocks are overlooking some big risk, be it a worsening economy, the banks, debt ceiling theatrics and more—it is a standard the dollar sees what stocks miss argument, whether it is implied or explicit. But, in our view, similarly liquid markets discount the same widely known information simultaneously. They just register that information in different ways, and early in a bull market, a lower dollar usually signals things are starting to look up.

You won’t hear that from most other outlets, for the simple reason that people tend to fear the dollar no matter what it does. When it is strong, we hear it will hamper US exports and endanger emerging economies. When it is weak, we don’t get the reverse of that—people don’t cheer it will cause an export boom and give emerging nations more flexibility. Instead it signals something or other going wrong on our shores. We take a more nuanced and probably boring view. The dollar, up or down, creates winners and losers. A strong dollar makes US companies’ imported labor, components and natural resources cheaper but can reduce export revenues. A weaker dollar can raise export revenues while increasing import costs. And many businesses hedge for all of it, usually blunting the impact.

In the end, the dollar is just there, triggering people’s emotions without doing much of anything at a fundamental level. For us, it is a handy sentiment snapshot, and if ever there came a time when the dollar inspired universal cheer, it would probably make us look long and hard for a euphoric stock market peak. But for now, we think it is the sort of false fear that new bull markets thrive on.

{kind=link}