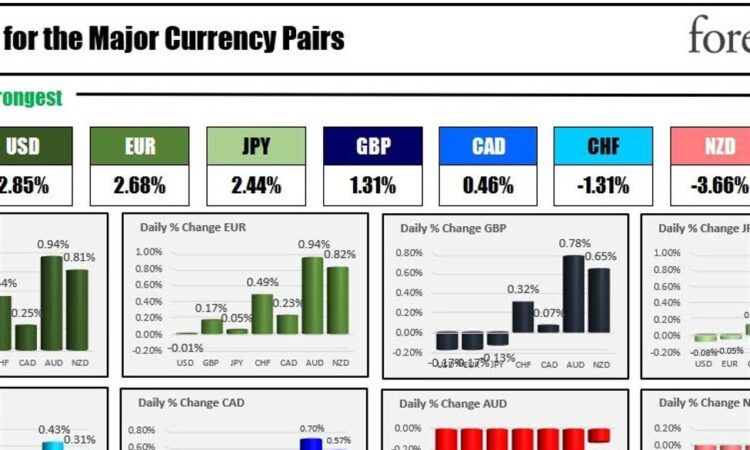

The strongest to the weakest of the major currencies

The USD is the strongest while the AUD is the weakest as the NA session begins. US yields are higher once again, which is pressuring stocks in early trading as well.

In Australia overnight, the RBA kept rates as expected at 4.10%. The AUDUSD has been In the statement, the central bank said in their statement:

- Interest rates have risen by 4 percentage points since the previous May, aiming to balance supply and demand in the economy.

- Despite passing its peak, inflation in Australia remains high and is expected to return to the 2-3% target range by late 2025.

- The Australian economy’s growth was stronger than expected in the first half of the year, but is currently experiencing below-trend growth due to high inflation impacting real incomes and household consumption.

- The unemployment rate is expected to rise gradually to around 4.5% late next year, with wages growth still aligned with the inflation target.

- The Board prioritizes returning inflation to the target, as high inflation impacts savings, household budgets, business planning, and income equality.

- Recent data indicates inflation is decreasing, the labour market is strong, and the economy is operating at a high capacity, though growth has slowed.

- Uncertainties exist around the outlook, including persistent services price inflation overseas, the effects of monetary policy, and household consumption affected by financial squeezes and rising housing prices.

- The Chinese economy’s outlook remains uncertain due to stresses in the property market.

- Further tightening of monetary policy might be needed to bring inflation back to target, depending on data and risk assessments.

Looking at the daily chart, the price is testing the lower trendline near 0.6297. The low just reached 0.62946. For dip buyers, this is the place to put a toe in the water.

The AUDUSD is testing a lower trend line target

The USDCHF continues its run to the upside after weaker CPI data earlier today (-0.1% vs. 0.0% estimate). The USDCHF is trading at the highest level since March 22 – moving above the high price from last week at 0.92242 a high price of 0.9237 and moving away from the broken 38.2% retracement of the move down from the November 2022 high at 0.91615. Buyers are in control above the 38.2% retracement in the medium term.

USDCHF moves away from the 38.2% retracement level

In the US, 10-year Treasury yields have climbed above 4.743%, and in the process reaching a new 16-year high, due to investor confidence in the robust economy leading to prolonged higher borrowing costs. The economy’s resilience has diminished hopes of the Federal Reserve reducing interest rates, leading to an expectation of sustained high borrowing costs for longer, which has in turn reduced the appeal of riskier assets like stocks. The Utility sector of the S&P is under extreme pressure as higher borrowing costs for longer, will raise costs for the capital-intensive industry, and with other yields rising, the choices for yield-hunting investors is greater. The utility sector of the S&P has tumbled 13.82% in the last 11 trading days, and is down -20.5% from the beginning of the year.

Economic data today will include the latest Job Openings and Labor Turnover Survey (JOLTS report). It is anticipated to reveal a decline in job openings to 8.8 million in August, continuing the trend from the previous month and indicating a slowdown in the labor market. This slowdown supported the Federal Reserve’s decision to maintain the current interest rates in September. The pace of workers quitting their jobs has also slowed, suggesting reduced confidence in finding better employment opportunities, which could potentially ease inflationary pressures. Despite this, the labor market remains tight, with job vacancies still outnumbering unemployed individuals, although the ratio has decreased slightly. The US jobs data from the BLS will be released on Friday with expectations of a gain of 169K (vs 187K last month). The unemployment rate is expected to dip to 3.7% from 3.5% and the average hourly earnings are expected to rise by 0.3% versus 0.2% last month.

A snapshot of the markets as the NA session gets underway shows:

- Crude oil is trading down $0.45 -0.51% at $88.36

- Spot gold is trading down $-2 or -0.11% at $1825.96. The price is trading at the lowest level since March 2023

- Spot silver is trading up 1% or 0.08% at $21.02

- Bitcoin is trading higher at $27,565. At this time yesterday the price was trading at $28212.

In the US premarket for US stocks, futures are implying a lower opening

- Dow Industrial Average futures are implying a decline of -146 points points after Monday’s decline of -74.15 points

- S&P index futures are implying a decline of -19.5 points after yesterday’s small 0.36 point gain

- NASDAQ futures are implying a small gain of -82 points after Monday’s 88.45 point rise

In the European equity markets, the major indices are trading mostly lower:

- German DAX, -0.78%

- France’s CAC, -0.75%

- UK’s FTSE 100, -0.13%

- Spain’s Ibex, -0.84%

- Italy’s FTSE MIB, -0.97% (10 minute delay)

In the US debt market, yields are higher with the yield curve steepening further. The 2 – 10 year spread is at -38 basis points which is steeper than the -47 base points at this time yesterday:

- 2-year yield, 5.123%, +1.1 basis points

- 5-year yield, 4.758%, +4.1 basis points

- 10-year yield, 4.743%, +6.0 basis points

- 30-year yield, 4.861% +6.4 basis points

- 2 – 10 year spread is trading at -38 basis points after trading at -47 basis points at this time yesterday

In the European debt market, benchmark 10-year yields are trading higher:

European benchmark 10 year yields

{kind=link}