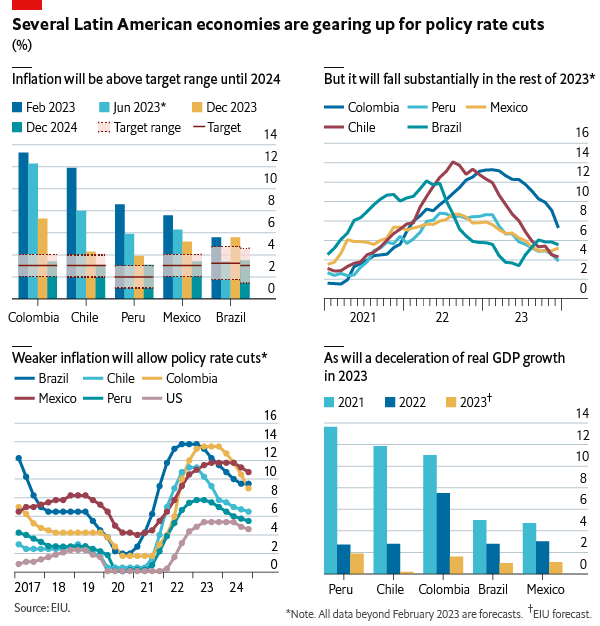

Notwithstanding continuing concern over the direction of the global economy, monetary policy easing is on the cards in Latin America this year. As economic activity weakens, inflation eases and inflation expectations move back towards target, central banks in the region are eyeing up rate cuts, and questions over the trajectory of US and European rates seem unlikely to stop them. For instance, in mid-March, in the same week that banking sector stress in the US and Europe caused currency jitters worldwide, Costa Rica made headlines by going ahead with a cut to its policy rate, becoming the first Latin American economy to embark on a monetary easing cycle after raising rates sharply in 2021-22. Costa Rica is one of a handful of emerging markets to have cut rates (Vietnam did so the same week; some anomalous cases like Russia and Turkey have also been easing policy). In Latin America at least, more will follow, starting with Brazil and Chile.

Latin American economies raised rates earlier and more aggressively than the rest of the world in 2021-22, and that cycle is set to go into reverse as major central banks in the region look to bring nominal rates down from double-digit levels. Rate cuts will be made possible above all by easing inflation. Although headline consumer price inflation was still high in February in most of the region, monthly data show clear signs of moderation (with some exceptions, like Colombia). Moreover, disinflation will gather pace over the year as big Ukraine-related price spikes drop out of the index. Inflation expectations are falling too; in Chile, 24-month-ahead expectations have returned to the middle of the target range. Meanwhile, economic growth in the region has slowed significantly from its January-June 2022 peak. In this environment, we think that the stage is set for rate cuts.

Not every economy in the region will be in a position to cut early or aggressively. Of Latin America’s big five economies (we are excluding Argentina, as its monetary dynamics are anomalous), Brazil, Chile and Peru seem more likely to cut early (around mid-year or even earlier), reflecting better inflation dynamics and, in some cases, stronger concerns about growth. Mexico and Colombia will be more cautious, and their rates may not come down until the end of 2023 or 2024. Colombia was late to tighten and is not yet seeing particularly encouraging signs of disinflation. In Mexico, although policymakers have not kept completely in lockstep with the US Federal Reserve, they will be extremely cautious about narrowing the interest-rate differential with the US, and in our view will be slow to shift to monetary easing.

The pace and extent of monetary easing will depend on currency movements stemming from the narrowing of the interest-rate differential with the US, or from growing investor risk aversion amid jitters over banking sector health in the US and Europe. We have already pencilled currency weakening into our forecasts for 2023-24, but any dramatic overshooting will cause central banks to re-evaluate monetary policy. For this reason, we are already less bullish than consensus on the outlook for monetary easing in Latin America, and we regard currency volatility as the main risk to our interest-rate forecasts. Any greater than expected weakening of the US or global economy—triggered, for example, by growing concerns about developed-country banking sector health—could in theory help the region to cut rates (by producing more dovish developed-country monetary policy). However, this would be a net negative economically, and a flight to safety would, in this environment, be damaging for Latin American currencies, creating fresh concerns about exchange-rate pass-through to inflation. On balance, we think that this scenario would prompt the region’s central banks to exercise greater caution and would ultimately dampen the rate-cutting cycle.

The analysis and forecasts featured in this piece can be found in EIU’s Country Analysis service. This integrated solution provides unmatched global insights covering the political and economic outlook for nearly 200 countries, enabling organisations identify prospective opportunities and potential risks.

{kind=link}