LONDON, April 21 (Reuters Breakingviews) – Early April in Washington is famous for two time-honoured rituals. The U.S. capital’s Tidal Basin hosts the National Cherry Blossom Festival. A few blocks further north you can hear the International Monetary Fund tell visiting finance ministers, central bankers and financiers about the dire economic outlook for emerging markets.

This year, the cherry blossom was spectacular. The IMF didn’t disappoint either. Its flagship Global Financial Stability Report noted that twelve emerging-market governments are already in financial trouble, and the foreign currency bonds of twenty more are trading at levels which have historically endangered countries’ ability to borrow. IMF Managing Director Kristalina Georgieva went further, warning that no fewer than sixty countries are at risk of debt distress.

The reason for the seasonal gloom is that the IMF and World Bank regularly raise capital from their shareholders to fund concessional lending. This year, the IMF is asking donors to stump up more than $6 billion of additional contributions before the multilateral lenders’ annual meeting in October. IMF bosses also remember the wilderness years of the early 2000s, when business dwindled to such an extent that the fund had to cut 15% of its staff and was nicknamed the TMF, or Turkish Monetary Fund, after its only sizeable remaining client. All in all, it never pays to paint too rosy a picture of emerging-market prospects.

This is why investors should beware of paying too much attention to the dismal mood music. The reality is that after many years of lacklustre returns, emerging-market sovereign debt has proved one of the best-performing asset classes over the past year. There are good reasons to think there is more to come.

Over the last twelve months, emerging-market currencies and bonds have passed two important tests. The first was the U.S. Federal Reserve hiking interest rates. Historically, monetary tightening in the United States has been kryptonite for emerging-market investors. Yet this time was different. Emerging-market currencies have been remarkably resilient over the past twelve months. The median major currency has weakened only around 2% against the U.S. dollar; the Mexican peso is up 10% against the greenback.

Bonds have done even better. The yield on benchmark 10-year U.S. Treasury notes has risen by 160 basis points since the Fed started hiking, inflicting hefty losses on bondholders. But the average yield on local-currency government bonds issued by major developing economies has increased by only half as much. In several markets, bond yields have fallen.

One reason for this resilience is that investors never cut these governments much policy slack in the first place. Unlike their counterparts in the developed world, less wealthy countries have not benefited from a decade and a half of near-zero interest rates. They could not rely on central bank bond-buying to help fund pandemic spending. Most important of all, many emerging-market central banks learned the lesson of previous cycles and raised rates early. Brazil hiked its official borrowing costs a full year before the Fed. By the end of 2021, two-thirds of the major emerging-market central banks were tightening monetary policy.

Emerging economies also appear to have avoided recent stress in the banking sector. Unlike their U.S. peers, emerging-market banks did not load up on long-dated assets which tumbled when policy rates rose. The IMF estimates that mark-to-market losses on securities currently held at par would shave 2.5 percentage points off the median U.S. bank’s core equity ratio if realised. For the median emerging-market bank, the same number is zero.

Yet if the surprisingly smooth navigation of the past year is noteworthy, the deeper structural changes in emerging countries are even more remarkable. The main reason emerging-market governments were so vulnerable to financial crises in the 1990s was their inability to develop local currency debt markets and their resulting reliance on dollar-denominated borrowing. This, coupled with chronic current account deficits and high levels of government indebtedness, invited periodic disaster.

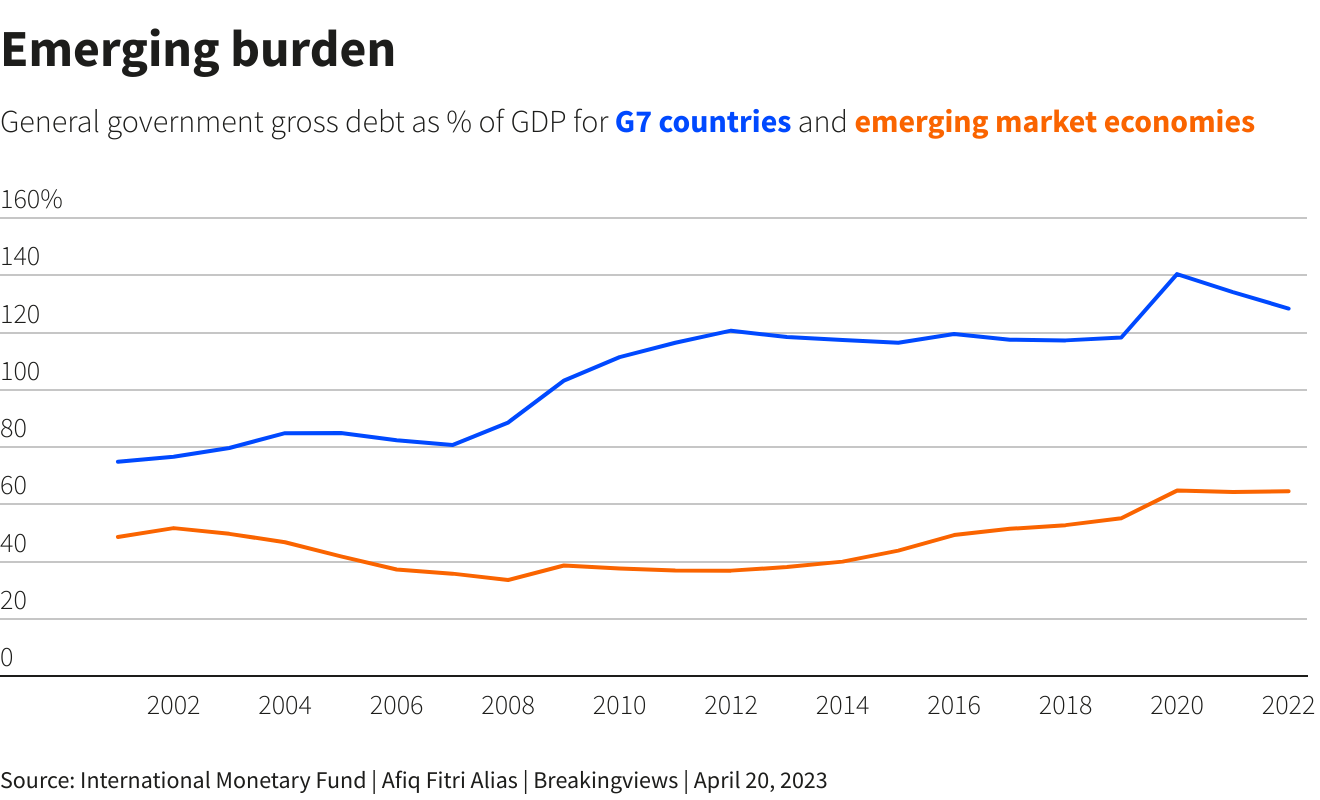

By last year, average emerging-market government debt was 65% of GDP, half the average of the Group of Seven leading economies, and most of it funded at home. Emerging markets ran a collective current account surplus of nearly 1.5% of GDP, compared to a 2% deficit for the G7. Back in 1996, the IMF and World Bank launched the Highly Indebted Poor Countries initiative, under which advanced economy creditors forgave 37 needy sovereigns more than $100 billion of debt. Perhaps the 2020s will bring a Highly Indebted Rich Countries initiative in which emerging-market countries return the favour.

Of course, aggregates and averages never tell the whole story. The IMF is quite right to raise the alarm over the plight of a subset of countries which have continued to borrow heavily in foreign currencies from official creditors over the past decade. Most of these troubled borrowers are in sub-Saharan Africa, and almost all have attracted only limited funds from foreign portfolio investors. Even their predicament shows how radically the centre of global economic gravity has shifted. The biggest creditor for most of these countries is typically China – itself the largest constituent of the benchmark emerging-market government bond indices.

With cheap valuations, much improved fundamentals and institutions which have earned their spurs over the past twelve months, the reality is that emerging-market sovereign assets don’t look too shabby when compared to their G7 counterparts.

It is no surprise that Georgieva painted the usual gloomy picture earlier this month. But when it comes to considering the investment case for the majority of emerging-market sovereigns, investors should not be swayed.

Editing by Peter Thal Larsen and Thomas Shum

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.

{kind=link}