Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

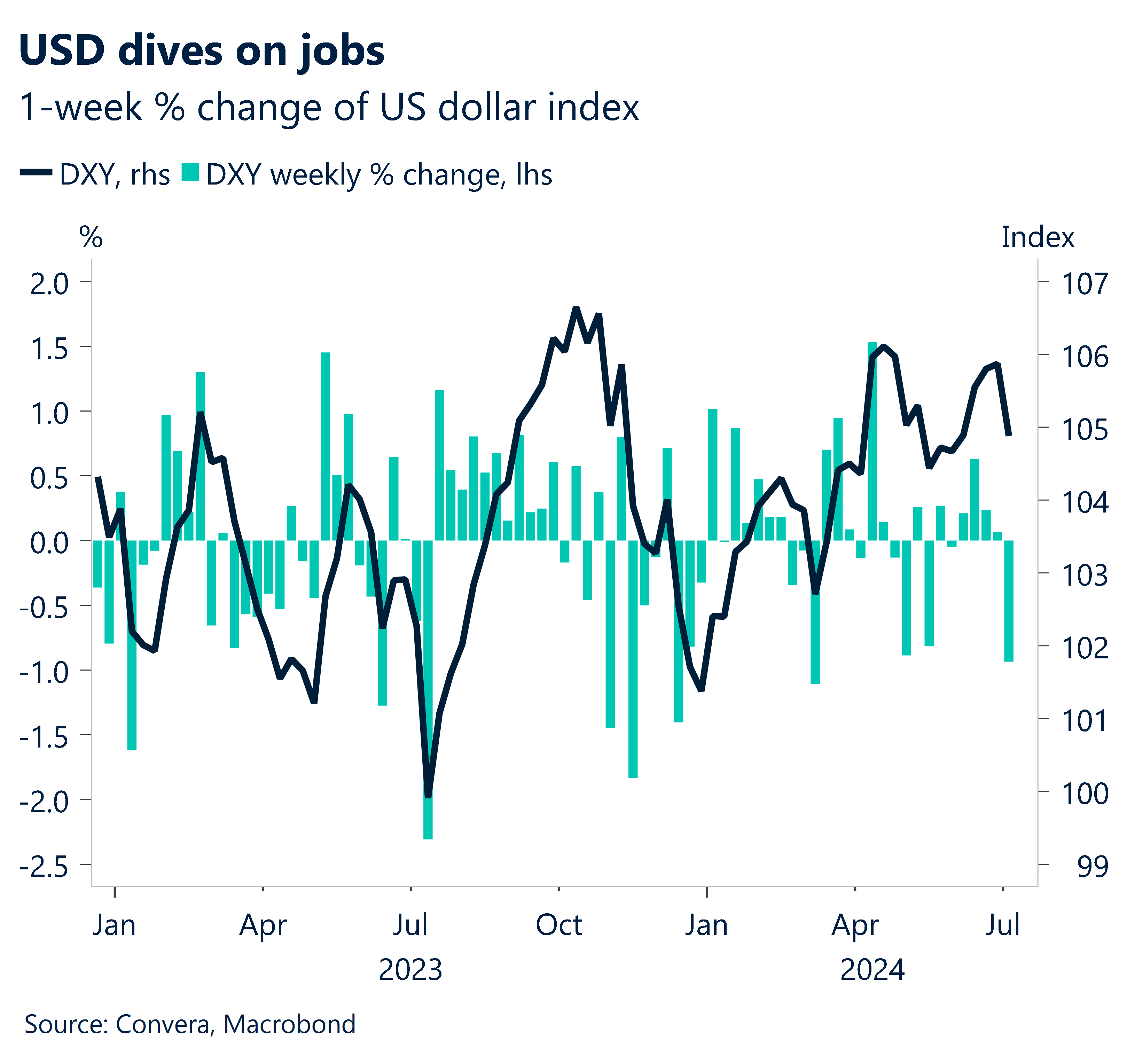

Greenback lower as jobs market shows cracks

A higher-than-expected US jobs report on Friday wasn’t enough to help the US dollar with a jump in unemployment, a fall in wages growth and revisions to previous numbers weighing on the greenback.

While the official jobs number came in at 206k versus 191k expected, the USD index fell to three-week lows with an increase in the unemployment rate from 4.0% to 4.1% – the highest number since November 2021 – causing markets to speculate that the Federal Reserve is likely to cut cuts twice before the end of 2024.

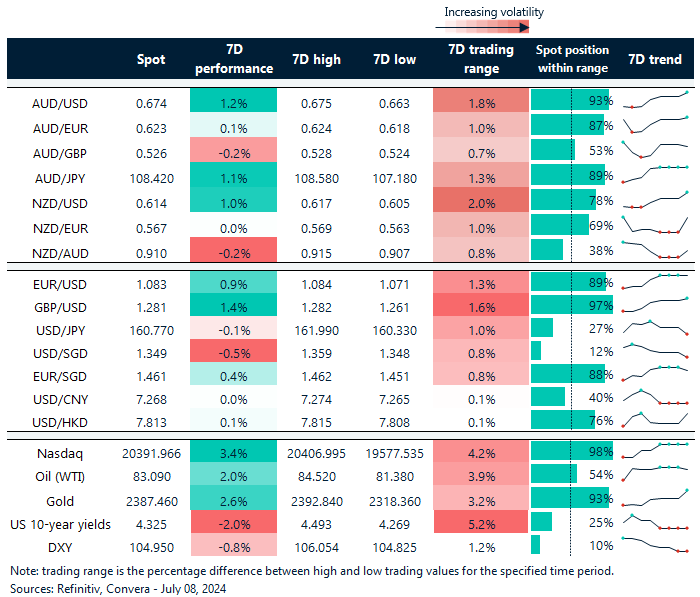

The AUD/USD jumped 0.4% as it reached the highest level since early January.

The NZD/USD gained 0.5%.

In Europe on Friday, the GBP/USD continued to gain after the Labour party won a record-breaking majority on Thursday with the pair up 0.4%.

The euro extended recent gains with the EUR/USD up 0.3% on Friday, but the EUR eased early Monday after a surprise result in the second-round of French parliamentary elections saw a win for the left-leaning coalition. The win was not enough for the left to form government, with president Emmanuel Macron’s centrist party coming second and some negotiations needed from here.

In Asia, the USD/JPY fell 0.3%, while USD/SGD lost 0.2%. The USD/CNH was flat.

US inflation key this week

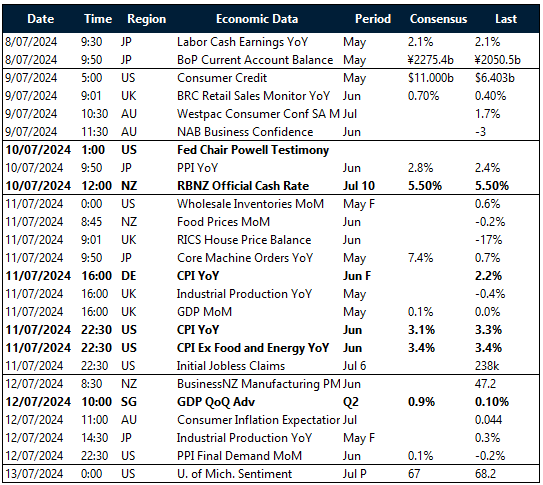

Looking forward, FX markets will be driven by central bank decisions and important economic data releases this week, with notable events from major economies including China, the United States, and Japan.

The week ahead features several key economic indicators that could influence currency movements, including inflation data from China and the US, trade balance figures from multiple countries, and industrial production reports from various economies.

In the United States, Federal Reserve Chair Powell’s speech and the CPI data will be closely watched for insights into the Fed’s monetary policy stance and inflationary pressures.

China’s CPI and trade balance data will be crucial for assessing the state of the world’s second-largest economy and its potential impact on global trade and currency markets.

In other markets, Japan’s economic indicators, i.e. the machinery orders, will be important for gauging the country’s economic health and potential policy shifts.

INR climbs from record lows

In India, Prime Minister Narendra Modi will still remain the PM for a third term, albeit through a coalition government, and investors are looking for clarity on policy continuity.

We expect continued choppiness in equities, while large cap and defensive-like staples could be in focus.

The new government will likely need to focus efforts on attracting manufacturing through the China plus 1 strategy along with creating more employment in labor-intensive industries. Focus will turn to budget details in July in particular around pace of fiscal consolidation. Near-term rates and FX impacts are likely to be muted by active Reserve Bank of India (RBI) management and passive flows related to index inclusion.

Aussie nears 2024 highs

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 8 – 13 July

All times AEST

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? AskMarketInsights@Convera.com

{kind=link}