(Bloomberg) — European stocks rose, while US index futures and Asian equities fell, as investors hunted for pockets of value amid hawkish central banks, disappointing earnings and further power consolidation in China.

Most Read from Bloomberg

The dollar gained before data on the Federal Reserve’s preferred inflation measure. The Stoxx Europe 600 Index climbed for a second day. Contracts on the S&P 500 and Nasdaq 100 slipped at least 0.2% each. Chinese technology stocks led a selloff in Asia amid signs price wars and cash burns are undermining profits. The yen drifted lower after the nominee for the Bank of Japan’s top job signaled continuity of loose monetary policy.

Traders are contending with a complicated investment landscape as they navigate the era of tighter monetary policy. The risks surrounding central banks’ continued fight against inflation are compounded by decelerating growth and corporate performance, growing geopolitical tensions from Russia to North Korea, and regulatory curbs in China.

“Rising tensions certainly increase the safe haven flows to the US Treasuries and interfere with the hawkish Fed pricing,” Ipek Ozkardeskaya, a senior analyst at Swissquote Bank, wrote in a note.

Europe’s Stoxx 600 gauge rose for a second day, almost erasing its weekly losses, as investors continued to show a preference for the region known for value stocks over the US or China where growth equities are more dominant. Energy and construction companies were the best-performing industry groups on the benchmark index.

A gauge of Chinese technology stocks listed in Hong Kong tumbled 3.3%. NetEase Inc. slumped after a profit miss, while Alibaba Group Holding Ltd. fell as analysts remained cautious about its sales growth prospect. Meanwhile, Chinese President Xi Jinping was set to bring decision-making of the financial system further under his control with the revival of a powerful committee.

The dollar advanced for the third time in four days before Friday’s release of the personal consumption expenditures index — the Fed’s preferred price gauge — which is expected to show acceleration amid robust income and spending growth. Treasuries were mixed.

German yields slipped after gross domestic product in Europe’s biggest economy contracted 0.4% in the fourth quarter, more than expected.

In commodities, oil extended Thursday’s advance, when it snapped its longest losing streak since December amid strength in commodity currencies and signs of appetite for risk taking.

Bitcoin was on pace for its second monthly advance, breaking with stocks and other riskier assets that have slid amid renewed concern about rising interest rates.

Key events this week:

-

US PCE deflator, personal spending, new home sales, University of Michigan consumer sentiment, Friday

-

Russia’s invasion of Ukraine hits the one-year mark, Friday

Some of the main moves in markets:

Stocks

-

The Stoxx Europe 600 rose 0.4% as of 8:43 a.m. London time

-

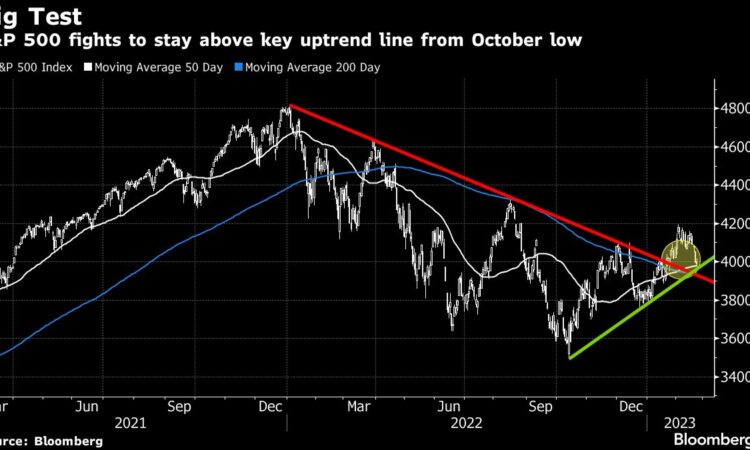

S&P 500 futures fell 0.2%

-

Nasdaq 100 futures fell 0.5%

-

Futures on the Dow Jones Industrial Average fell 0.1%

-

The MSCI Asia Pacific Index fell 0.6%

-

The MSCI Emerging Markets Index fell 1.3%

Currencies

-

The Bloomberg Dollar Spot Index rose 0.1%

-

The euro was little changed at $1.0594

-

The Japanese yen fell 0.1% to 134.88 per dollar

-

The offshore yuan fell 0.5% to 6.9527 per dollar

-

The British pound rose 0.2% to $1.2039

Cryptocurrencies

-

Bitcoin rose 0.1% to $23,905

-

Ether rose 0.5% to $1,653.78

Bonds

-

The yield on 10-year Treasuries was little changed at 3.88%

-

Germany’s 10-year yield declined three basis points to 2.45%

-

Britain’s 10-year yield declined three basis points to 3.56%

Commodities

-

Brent crude rose 1.2% to $83.22 a barrel

-

Spot gold rose 0.2% to $1,825.35 an ounce

This story was produced with the assistance of Bloomberg Automation.

–With assistance from Tassia Sipahutar, Rob Verdonck, Richard Henderson and Matthew Burgess.

Most Read from Bloomberg Businessweek

©2023 Bloomberg L.P.

{kind=link}