ORLANDO, Florida, Aug 14 (Reuters) – In five years’ time the U.S. government’s annual interest bill on its debt is projected to reach $1 trillion, or 3% of GDP – impending fiscal catastrophe, as the first figure might imply, or manageable burden, as the second one indicates?

U.S. debt sustainability is back in the spotlight after Fitch downgraded the U.S. credit rating this month. High interest rates and bond yields are increasing the amount Washington must pay to service the federal debt, which neither economic growth nor inflation look like sufficiently eroding.

Managing the ballooning debt is more challenging now than when S&P stripped the United States of its AAA rating in 2011. The deficit before interest payments was lower then, economic growth was weak but still higher than prevailing interest rates, and the Fed was buying boatloads of bonds.

Conditions are far less benign now.

But as ever, the crux of the matter is the price at which investors will lend to Uncle Sam, not whether the debt will be serviced. On that score, history suggests their appetite for dollars and dollar assets will hold up well.

Doubts over the U.S. fiscal trajectory, the dollar’s relative value or status as the world’s preeminent reserve currency are nothing new. Consider this Business Week article from March, 1978:

“The role of the dollar as the world’s major reserve currency is beginning to be eroded by its weakness and the inability of the Carter Administration to check its fall. Investors … are hurrying to move cash into marks, Swiss francs, and Japanese yen. Foreign central banks are doing the same.”

Reuters Image

DOLLAR DEMISE GREATLY EXAGGERATED

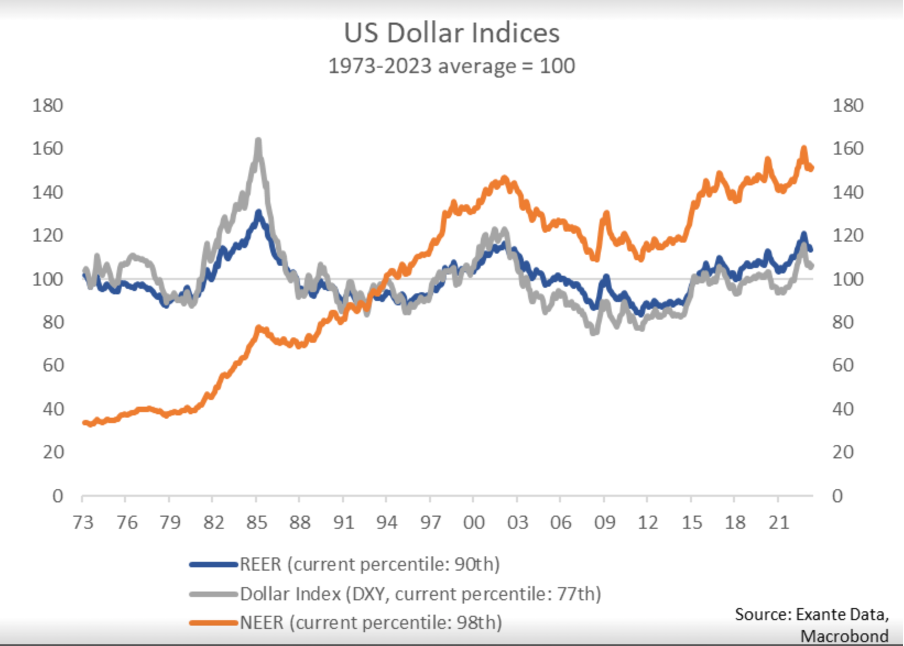

The U.S. currency has gone through many peaks and troughs since then, experiencing significant bouts of official intervention – dollar-buying and selling – along the way. In relative terms, it has more than stood its ground.

On a broad real effective exchange rate (REER) basis the dollar today is around 12% higher than its 50-year average going back to 1973, according to Exante Data. The dollar is in the 88th percentile relative to its history over the past half century, Exante Data also notes, meaning it has only been weaker 12% of the time since 1973.

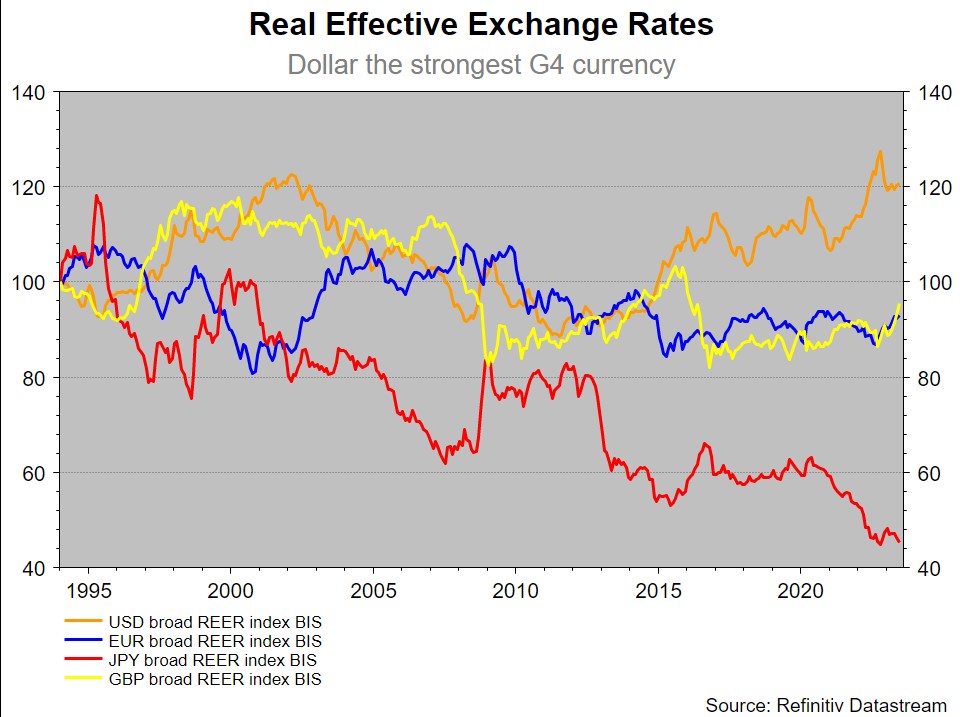

In the last 30 years, the dollar’s real effective exchange rate has appreciated around 20%, making it by far the best-performing of the G4 currencies over that period.

Reuters Image

The dollar is the number one destination for global savings and investment flows, and there is little evidence that its pre-eminent status is under threat. Investors want to hold the world’s reserve currency and be in the world’s deepest, most liquid capital markets.

“People are locked into these markets. What else are they going to buy? Dollar assets are the only game in town,” said Chris Marsh, senior adviser to Exante Data.

There is still no viable alternative. Germany’s 1.6 trillion euro bond market is a fraction of the $23 trillion U.S. Treasury market, Japan’s central bank and domestic investors own almost all Japanese Government Bonds, and the political risks and capital controls in China are significant.

Even if the dollar were to fall 15-20% over a few years, would that be cause for panic?

WARNING SIGNS

That said, America’s deteriorating fiscal health means there is less room for complacency than ever before. Interest payments as a share of federal revenue, spending, and the economy are set to reach historically high levels early in the next decade.

Fitch sees gross government interest payments as a share of revenue rising to 10% in 2025 from 7% last year, and the non-partisan Congressional Budget Office predicts net interest payments will reach 3% of GDP by 2028, a new post-1940s high of 3.2% of GDP a couple of years later, and 6% of GDP by the midway point in the century.

The CBO also expects the total fiscal deficit to reach 10% of GDP by 2053.

These are big numbers, running into trillions of dollars. Phil Suttle, founder of consultancy Suttle Economics, warns that appetite to hold U.S. Treasuries may not be as solid as meets the eye, especially with the Fed no longer buying and banks scarred by the regional banking shock in March.

“The problem with debt sustainability is there are so many moving parts. It’s not just the supply of debt that matters – demand to hold that debt is critical. Everything looks ok, until it isn’t,” he said, adding that any U.S. fiscal crisis will likely involve a weaker U.S. dollar.

Despite several scares and close calls over the years, this hasn’t happened yet. Until there are credible alternatives to the power and reach of the dollar, and depth and liquidity of Treasuries, U.S. deficits will be covered.

Just at a slightly cheaper dollar price or higher interest rate.

(The opinions expressed here are those of the author, a columnist for Reuters.)

By Jamie McGeever; Editing by Kirsten Donovan

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.