By Atul Bhatia, CFA

Key points

-

Electronic payments are on the rise as cash usage declines across the

globe, leading an increasing number of governments to think about

launching digital versions of their currencies. -

Central bank digital currencies, or CBDCs, in theory offer faster and

cheaper payments, allow people currently outside the traditional

banking system access to financial infrastructure, and could reduce

settlement risk and delays on international trade. -

Despite the hype around CBDCs, we see a host of security, privacy, and

governance concerns that we believe outweigh the theoretical gains on

efficiency, and we think it would be quite challenging to line up the

necessary political support for an aggressive push toward a digital

dollar. -

We think the Federal Reserve will continue to emphasize incremental

technology improvements versus a risky push to transform the payments

infrastructure. -

Bottom line: Commercial bank accounts and physical cash are likely to

remain at the center of U.S. financial architecture for the

foreseeable future.

Cash may be king, but the crown seems to have lost some of its luster of

late. Survey data shows consumers across the world increasingly prefer

electronic payment over currency, with more than 70 percent of respondents

from countries as varied as Sweden and South Korea wanting to go cashless.

At the same time, producing and distributing currency – as well as fighting

counterfeit notes – is an expensive and difficult process. The solution, it

would seem, is obvious: have central banks distribute currency in

electronic format, an idea known as a central bank digital currency or

CBDC.

CBDC is a global phenomenon, with dozens of countries studying the idea

and a handful already implementing some version of a CBDC. Given the

global prominence of U.S. currency, we focus our discussion on the

potential for a digital dollar, and conclude with a brief discussion of

China’s experience as one of the leaders in rolling out digital currency.

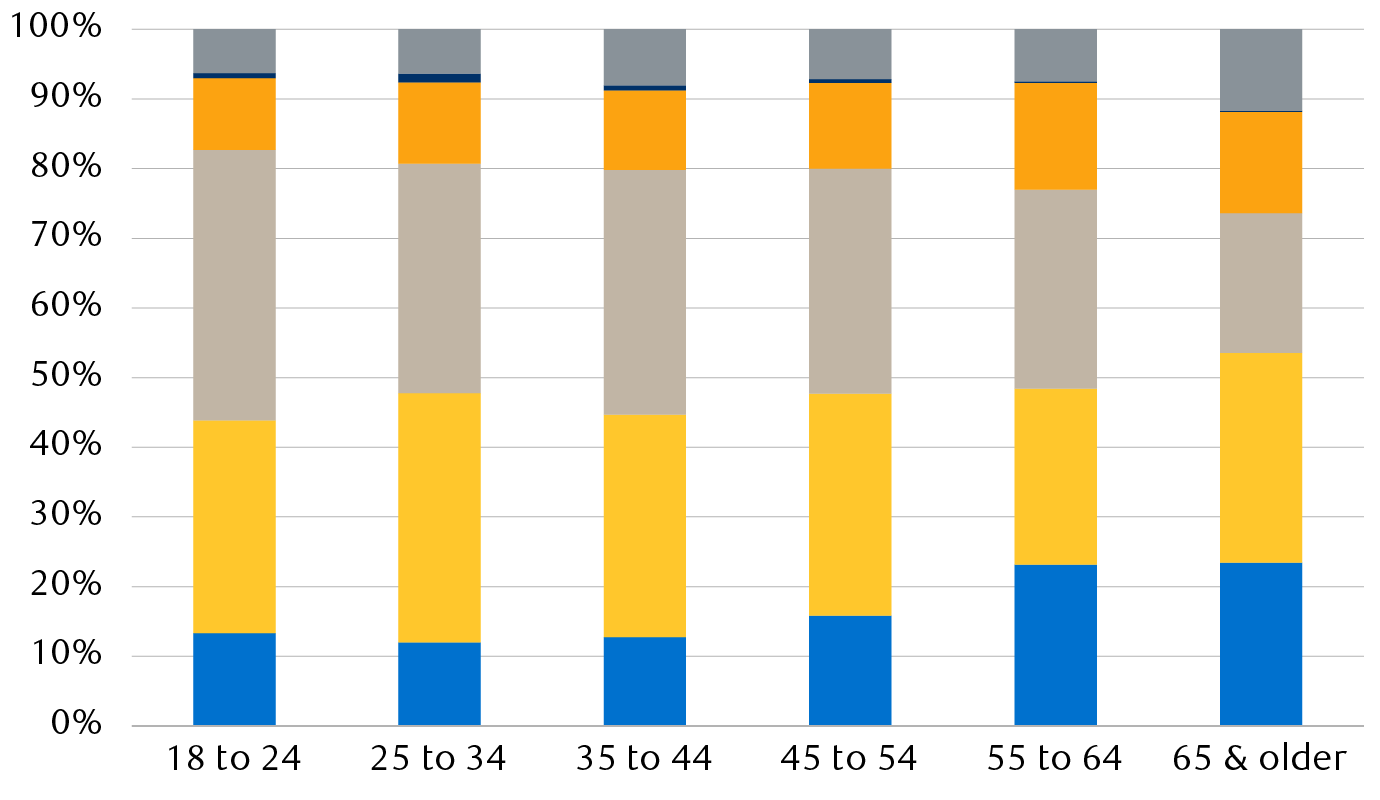

Showing its age? Younger people use cash less often

Percentage of payments made using various methods, by age cohort

Column chart showing how payments system usage varies with age and reflects an increased use of cash in older cohorts, with those 55 and older using cash 20% of the time. Individuals under 45 use cash about half as much as those over 55, with the difference being increased use of credit and debt by younger users.

-

Cash

-

Credit

-

Debit

-

ACH

-

Mobile Payment App

-

Other

Source – Federal Reserve Bank of San Francisco; ACH = Automated

Clearing House

Digital currency label breeds confusion

As with many financial innovations, we think rhetoric has outstripped

precision, so there are some differences in what people mean when they

talk about central bank digital currencies. For us, a true CBDC is a

system where individuals hold currency directly at a central bank, in

electronic format, with no means of converting their holdings into

physical currency.

Although digital, CBDCs are not cryptocurrencies. One hallmark of a

cryptocurrency is that the supply of money is not controlled by an

institution. Bitcoin, for instance, is created and paid out as a reward to

so-called miners, or the users who perform the background computational

work to keep the system going. CBDC, on the other hand, remains fiat

money, created or destroyed by a central bank as part of its monetary

policy decision-making. Some of the CBDCs being evaluated by central banks

rely on the digital architecture of cryptocurrencies, such as blockchain

verification, but that’s a distraction, in our view. At its core, a

digital dollar is still a dollar, and the number in circulation is set by

the Federal Reserve, not a formula.

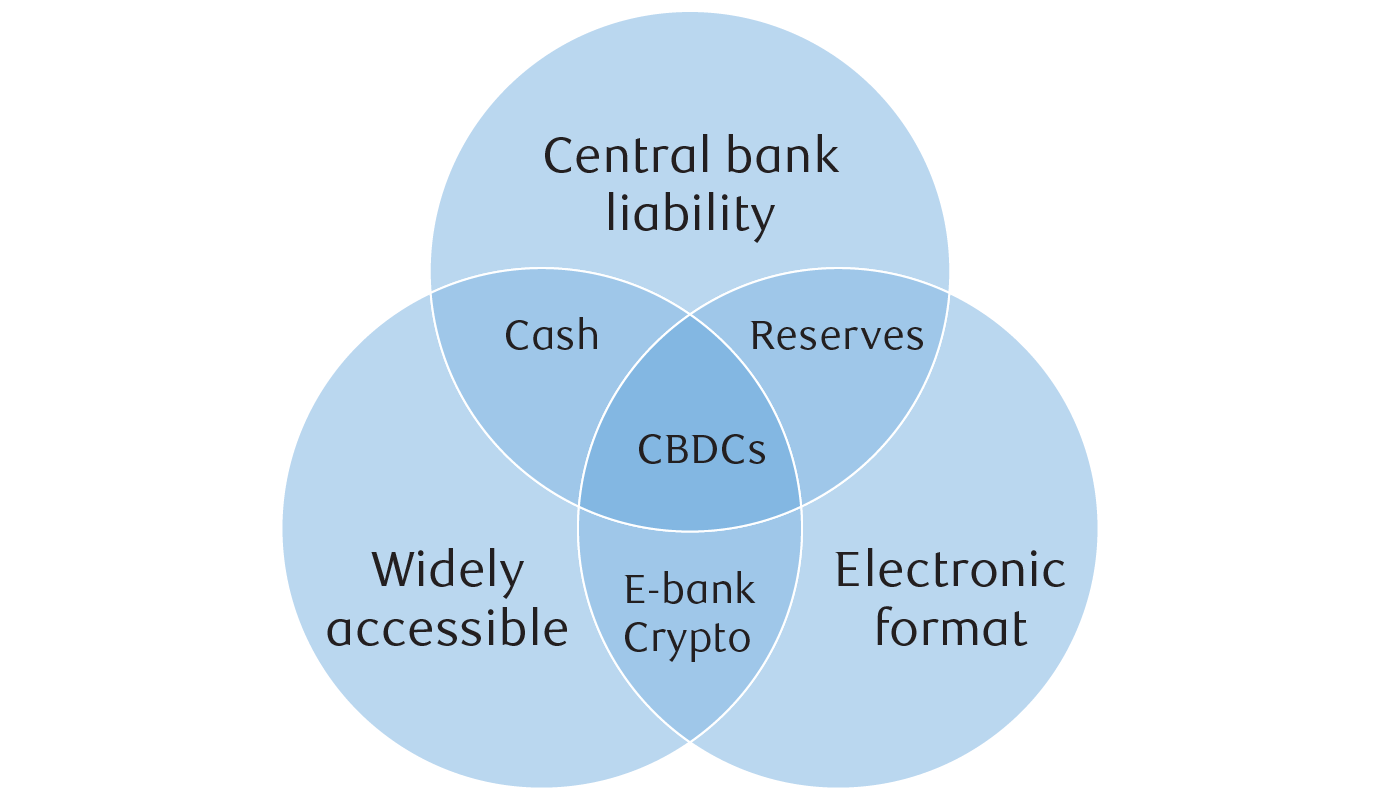

CBDCs’ place in the currency landscape

This is a Venn diagram showing the overlap between three characteristics of different payment types: central bank liability, electronic format, and widely accessible. CBDCs are at the intersection of all three, cash is in the overlap between widely accessible and central bank liability, reserves are in the overlap between central bank liability and electronic, and crypto and e-banking are at the overlap of electronic and widely accessible.

Source – RBC Wealth Management

In fact, despite the emphasis on the digital format, we believe the core

difference between a digital currency system and a physical one is how

records of ownership are maintained.

With physical dollars, ownership records are diffuse. The cash that an

individual has on deposit with a bank is largely known only to the bank

and the depositor. Funds can be transferred completely anonymously, via

cash, and even when transferred electronically, records of the movement

will be separated: the payer’s bank, for instance, will know which account

to debit, but it won’t know any information about the recipient. The

receiving bank will credit its customer yet knows nothing about the payer.

This system is gloriously inefficient, with a single transaction easily

requiring four separate institutions to update records and possibly taking

days to make the transfer final, but it has also functioned effectively

for centuries.

In the case of a digital dollar, efficiency is the watchword. Ownership

records are fully electronic and consolidated, making movements between

accounts simple and instantaneous. In practice, individuals and businesses

would likely have accounts directly at the Fed, and buying groceries, for

instance, would simply involve a customer moving CBDC from its Fed account

to the grocer’s. Since both accounts are held at the same institution, the

central bank can instantly and freely transfer the funds, eliminating the

delays inherent in our current, dispersed banking system.

This type of digitization is not new. The U.S. essentially went through

this process in the 1980s, when Treasury bond ownership went from being

physical securities to so-called book-entry format. Conceptually, that

move was identical to what’s being contemplated here: replacing a physical

asset – paper bonds with attached coupons – with a central database recording

ownership. Book entry made transfers simple and coupon payments routine,

generating massive efficiency in the Treasury bond market. The difference

between CBDCs and book entry bonds is one of degree, not kind.

McMoney – fast and cheap

Broadly speaking, we see two main benefits to countries that choose to

implement a CBDC.

First, it would reduce costs and increase access to payment services. In

the U.S., for instance, roughly five percent of the U.S. population does

not have a bank account and most small businesses pay between two percent

and five percent of revenues for payment processing, mainly credit card

fees. A CBDC would eliminate those costs and bring the entire population

into the banking system, creating savings and efficiencies that would be

felt positively, even in an economy the size of the United States’. For

countries with larger unbanked populations or higher payment fees, the

potential gains would be even more important.

Second, it would reduce transaction processing times and so-called float

risk, as suppliers wait for payments to clear. This is mainly an issue for

larger corporate transactions and international trade, but the ability to

create immediate transfers in a closed financial system can mitigate

certain types of fraud risk and can greatly reduce lost interest income.

There are other potential benefits that CBDCs can create by reducing

counterfeiting, cutting production and distribution costs, and potentially

helping policy implementation, but we think those are of secondary

importance. The economic case for a CBDC, we believe, begins and ends with

the efficiency of reducing financial friction costs across the economy.

Why a CBDC won’t be coming to a Federal Reserve near you anytime soon

Economists in general like efficiency, but the flipside is that efficient

systems lack the redundancy that make for stability. We think having a

single point of failure for dollar payments in a world that uses the

greenback for all manner of trade is, in a nutshell, a terrible idea. In

one move, we think the U.S. would create an unparalleled target for

hackers and thieves, not to mention terrorists or geopolitical rivals.

Even a cursory look at the history of electronic security shows the risks

of centralizing data and wealth.

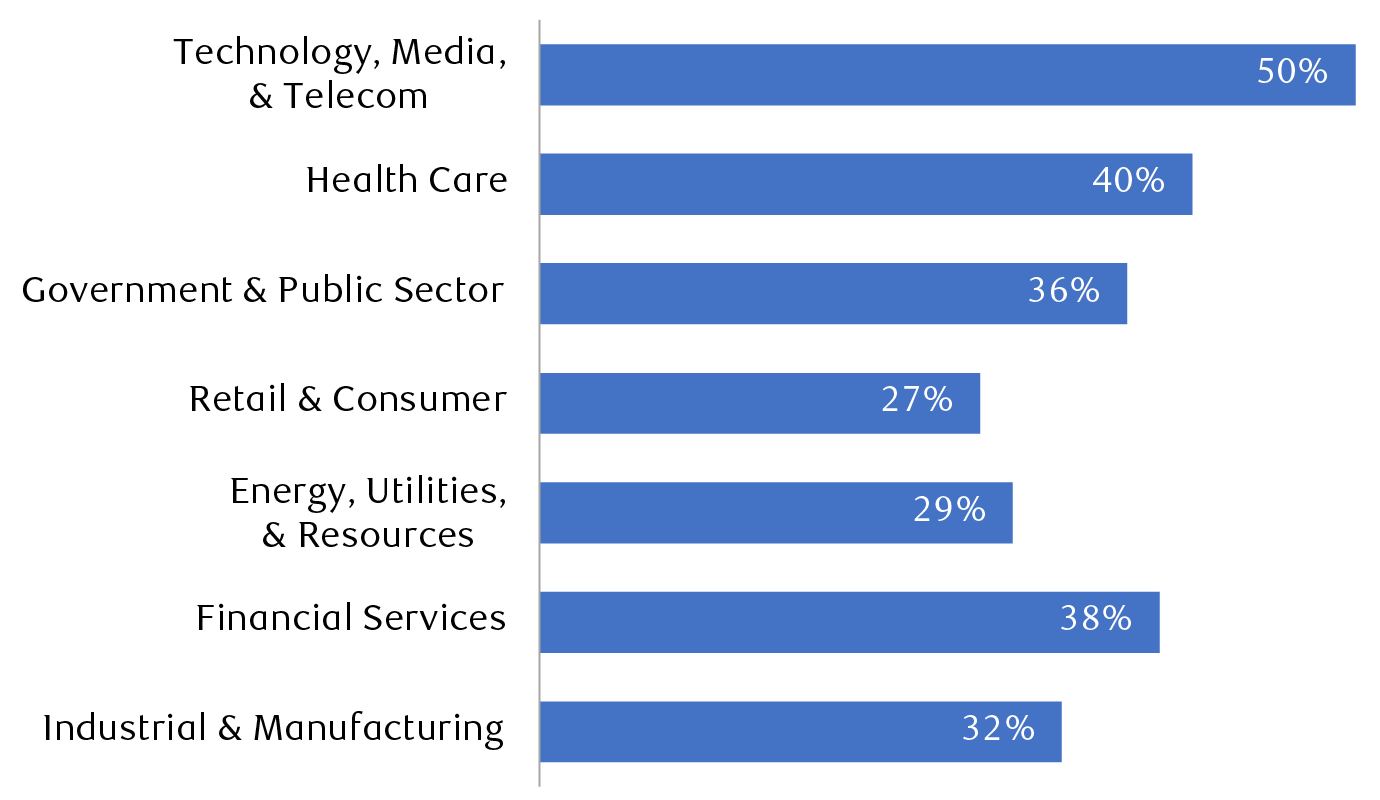

Existing levels of cybercrime highlight risks

Share of companies reporting cyberfraud events in previous two years, by

sector

Bar chart showing the percentage of companies reporting cyber fraud incidents in the previous 24 months. The chart shows values ranging from 27% for Retail to 50% for Technology, Media, & Telecom companies. Additional companies shown: Health Care: 40%; Government & Public Sector: 36%; Energy, Utilities, & Resource: 29%, Financial Services: 38%; and Industrial & Manufacturing: 32%.

Source – PwC Global Economic Crime and Fraud Survey 2022

Putting aside potential bad actors, what about a software update that goes

wrong? The U.S. has seen nationwide flight departures canceled because a

contractor accidentally deleted the wrong files in a critical Federal

Aviation Administration system. That was bad, but a world where dollarized

economic activity cannot take place for hours or days or even minutes

would be catastrophic.

The Fed already operates mission-critical payments systems, but these

generally offer connections only to depository institutions or regional

Federal Reserve banks. Trying to secure a system offering hundreds of

millions of access points to trillions of dollars on a 24/7 basis is a

Herculean task, and we believe current technology and practices are

insufficient to truly protect a CBDC environment.

Outside of security, there are also privacy concerns with centralizing

sensitive financial information and making it available to the government.

In the U.S., federal officials already have broad access to individual

financial data via subpoena powers, but combining all financial

information in one spot is a step-change higher in potential informational

abuses.

There are also concerns the government would be able to interfere with

certain transactions. Take, for instance, the U.S. states where marijuana

is now legal. Many of these businesses already struggle to find banking

services, but that fight is nothing compared to the potential impact of

being shut out by the Fed in a world where a CBDC is the only alternative.

A single decision to cut off marijuana spending would reduce those

businesses – deemed legal by the states where they operate – to bankruptcy or

the barter system.

Even with privacy guardrails, we believe the potential powers a CBDC would

give to the Fed – which is already a massively powerful institution – would

almost inevitably lead to politicization of the central bank. We shudder

to think of the U.S. Senate confirmation hearings for a Fed chair nominee

in a world where that person could exert practical control over the

payments system, and we believe those political considerations would

quickly override the monetary policy credentials for future nominees.

No, really, not anytime soon

On balance, our view is that it’s difficult to make a strong theoretical

case for moving to a CBDC infrastructure. The efficiency benefits are real

and meaningful, but they simply cannot justify creating a single point of

failure in critical payments infrastructure.

In practical terms, we see an even steeper climb for the digital dollar.

Historically, the U.S. has never been an early adopter of financial

innovation. It was one of the last countries to implement chip credit

cards, and the U.S. remains the largest user of paper checks in the world.

Over five percent of cashless payments in the U.S. still take place by

signing little chits of paper; it’s difficult to reconcile that with the

imminent arrival of digital currency wallets.

We also see significant pushback from existing players in the financial

infrastructure. Last year, the two largest U.S. credit card networks

reported over $50 billion in revenues – which would be under immediate and

severe threat if a CBDC offered a free alternative.

The broader banking system would not be immune from the impact of a CBDC.

At a minimum, we see a digital dollar raising funding costs for banks, as

zero-interest depositors would have no need to stay in the cumbersome

commercial banking system when the Fed offered an instant and free

alternative. If the Fed were to offer interest on deposits – broadening the

digital currency from a simple cash substitute to a digital money

supply – then the risk to banks increases exponentially. At that point, the

Fed would be a true competitor to deposit-taking and loan-making

institutions in their core businesses.

In congressional testimony on CBDCs in 2022, CEOs of large banks were

ambivalent-to-negative, mainly couching criticism on practical grounds.

Given the stakes to the well-heeled and politically astute financial

players, we would expect much more significant pushback if a digital

dollar ever moved closer to reality.

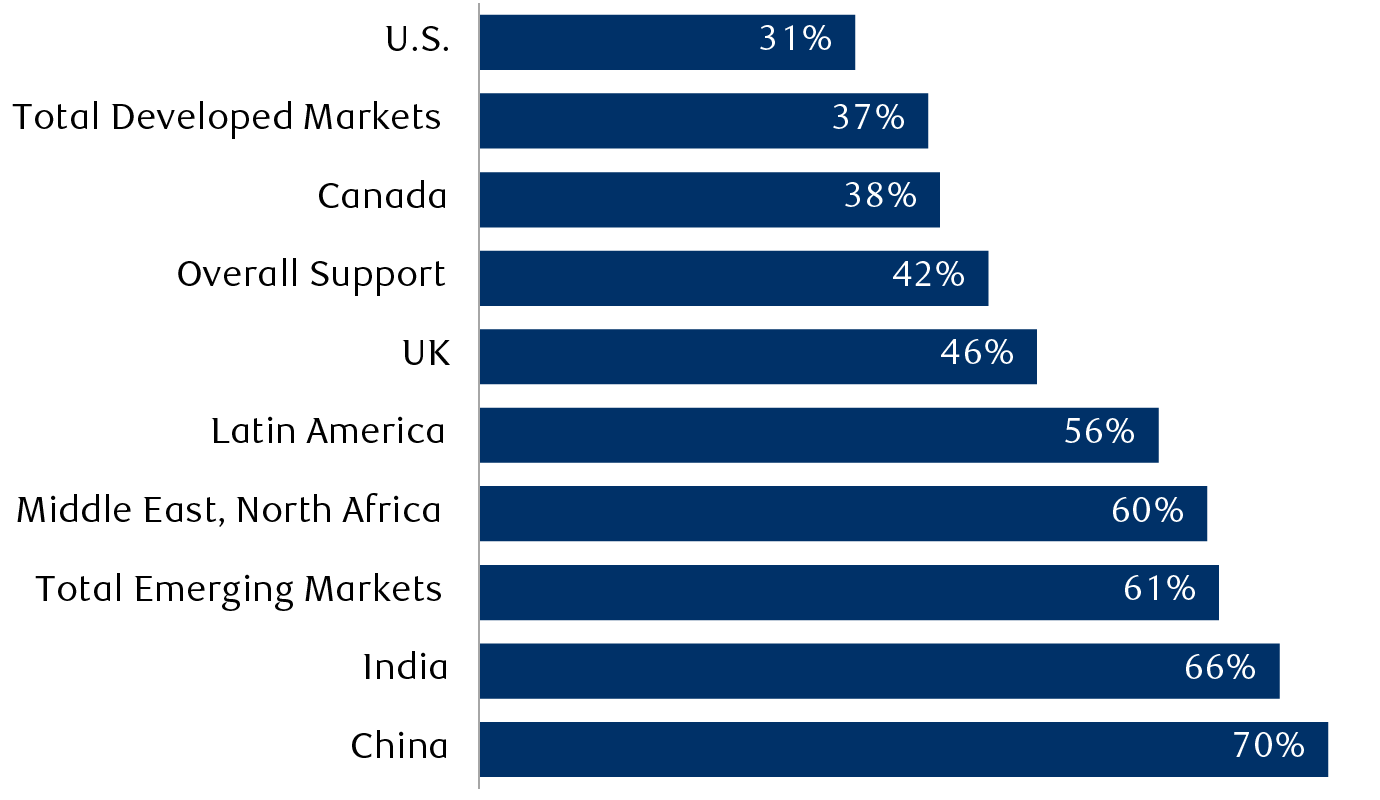

Geography heavily influences financial professionals’ support for a CBDC

Percentage of respondents in favour of launching a CBDC

Bar chart showing Chartered Financial Analysts’ support for CBDC based on geography. CFA charterholders in China have the highest level of support at 70%, while in the U.S. only 31% favour launching CBDC. Additional geographies shown: Total Developed Markets: 37%; Canada: 38%; Overall Support: 42%; UK: 46%; Latin America: 56%; Middle East, North Africa: 60%; Total Emerging Markets: 61%; and India: 66%.

Source – CFA Institute; respondents were CFA charterholders

The bottom line is that between privacy, security, and lobbying, we see a

CBDC as a tough sell to the U.S. Congress.

Incremental, not transformative, technology

Rather than fully transition to a CBDC, we expect the Fed and most other

central banks to take a more measured approach, closely integrating

technology to achieve efficiency but operating in parallel with existing

payment structures.

Take, for instance, FedNow, a new real-time payments system created by the

Federal Reserve. Like a CBDC, the system allows immediate, electronic

settlement, but, critically, it operates between depository institutions.

The limited scope reduces security concerns, while competitive forces

should eventually bring FedNow’s time and cost savings to individual

customers. This private-public hybrid approach, in our view, is both

better and more likely to occur.

The case for a CBDC is also weakened by the rise of large, global

commercial banks. Many of the benefits of centralizing payments are

already occurring, as trade between multinational companies is often

settled at one of the dozens of truly global banks. These banking services

are not free, but they have the potential to deliver many of the

efficiencies provided by a CBDC without the baggage of centralized

control.

We think the Fed is likely to continue studying a digital dollar and

running pilot programs. It would be unwise not to since the dollar’s

preeminent role in trade may someday require a digital currency. We

believe the Fed may even launch something it calls a digital dollar, even

if in practice it’s just a check-the-box exercise to show the U.S. also

has the latest shiny new toy.

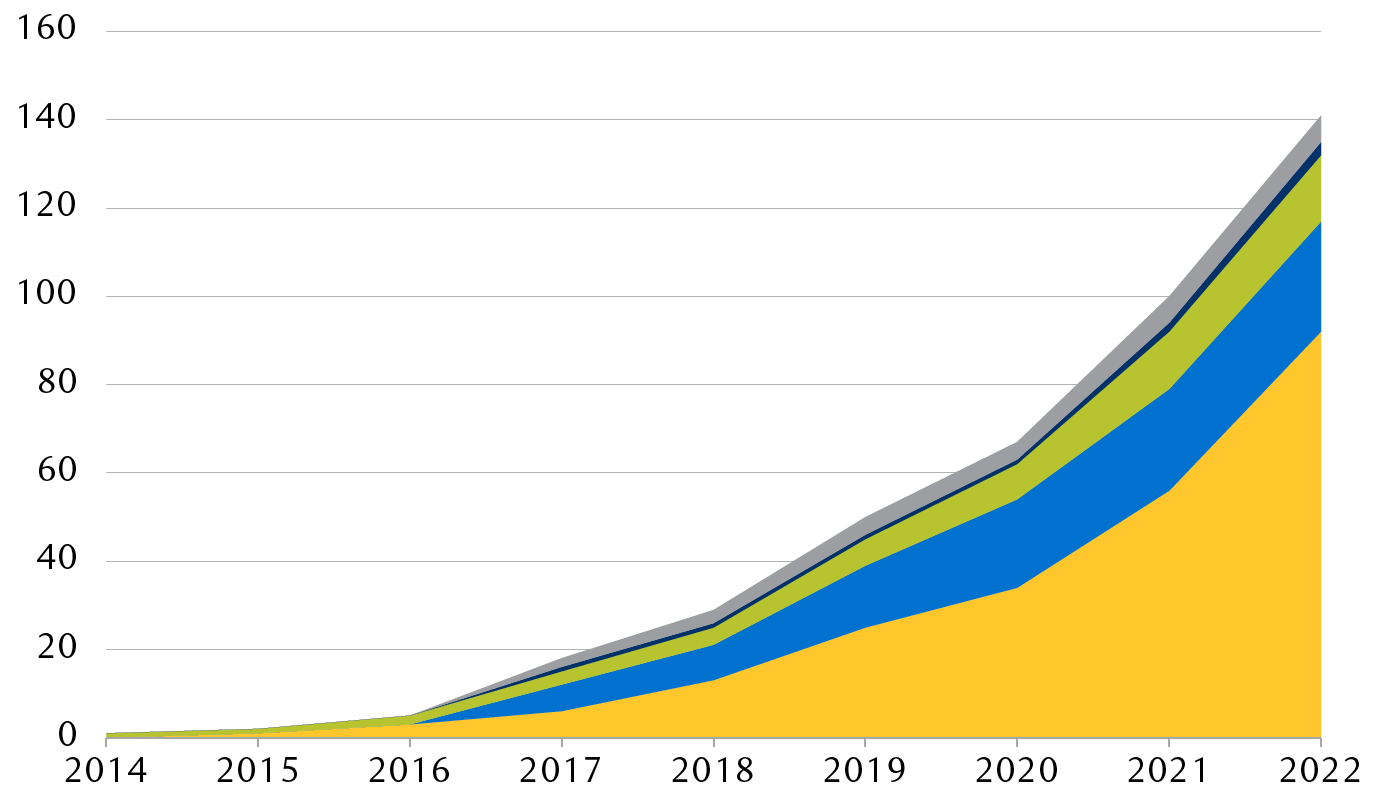

Central banks move forward, slowly, with CBDCs

Number of CBDC projects by stage of development

Area chart tracking the evolution of central bank actions on CBDC. In 2015, there were only two central banks active in CBDC, but by 2022, over 135 CBDC projects were active, with 92 of these being in the research phase, with the balance in proof of concept, pilot, or already launched.

-

Research

-

Proof of concept

-

Pilot

-

Launched

-

Canceled

Source – CBDCTracker.org, International Monetary Fund, RBC Wealth

Management

Realistically, however, we see physical currency and individual deposit

accounts at commercial banks at the center of the U.S. system for the

foreseeable future.

China in the lead

Unlike the U.S., China has been a leader in the digital currency field,

rolling out the digital yuan, also known as e-CNY, and actively

encouraging its use. The Chinese have implemented several interesting

twists on the CBDC concept. First, the e-CNY pays no interest, making it

much more of a pure cash substitute than other CBDCs under discussion that

allow for interest payments. In addition, the use of e-CNY is voluntary

and intermediated through large banks. These differences seek to reduce

the impact of the digital yuan on the traditional banking system, but they

also can reduce many of the potential efficiencies.

Uptake for e-CNY has been limited, with officials reporting less than 0.2

percent of cash has shifted into the digital format. One of the main

problems for e-CNY, in our view, is the prevalence, quality, and

integration of the existing digital payment platforms. Private sector

mobile payments in China go back nearly 20 years, and the two major

players control 90 percent of the country’s digital payments market. The

e-CNY has been growing, but the private-sector alternatives are already

low-cost and embedded in the user’s digital life. One advantage of e-CNY

is its ability to function when a user is offline, a key differentiator in

remote areas or during natural disasters, but one that has yet to

translate into broad usage of the digital yuan.

In essence, China has so far been taking an incremental approach, similar

to what we see the Fed doing. The difference is that the Chinese are

relying on the structure of the e-CNY to limit its potential as a

surrogate for the broader banking system, while we see the Fed eschewing

the concept of a digital dollar, at least for the near future.

China continues to push forward on the use of CBDCs for international

trade. The most recent step has been the launch of mBridge, a fully

digital trade settlement platform involving China, Thailand, the United

Arab Emirates, and Hong Kong. The infrastructure is important, but we see

limited uptake until the more widely held currencies such as the euro or

the U.S. dollar are in the system. The benefits of CBDC settlement are not

going to be sufficient, in our view, to shift investor and corporate

preferences around currency exposure.

Small steps on a long road

Central bank digital currencies, in some form, are likely to be adopted by

an increasing number of countries. Nations with a high percentage of

electronic payments, or a relatively concentrated and small banking

system, may find it easier to introduce some form of a CBDC. In time,

these countries or others may realize the efficiency potential of central

bank digital currency in a secure format. For now, however, we believe

CBDCs should be viewed as an adjunct to existing payment and banking

systems. We see evolution, not revolution.

{kind=link}