(Bloomberg) — A seismic shift in capital flows is playing out in Europe’s bond and currency markets as investors adjust to a world without central bank stimulus.

Most Read from Bloomberg

Three hundred basis points of interest-rate hikes by the European Central Bank since July have halted the years-long exodus from the region’s fixed-income funds. Net outflows that hit €818 billion ($872 billion) in late 2021 — the most in at least two decades — have now been reversed, data compiled by Deutsche Bank AG show.

The juicier bond yields, as well as relief that the war in Ukraine hasn’t sparked a deeper energy crisis, are also removing a fundamental drag on the single currency as capital shifts from higher-yielding markets like the US into euro-denominated assets.

“Underlying flow dynamics are turning dramatically more positive for the euro this year,” said George Saravelos, the bank’s global head of FX research. “Money managers are telling us they’re seeing waves of investment flows into European fixed income for the first time in a long while.”

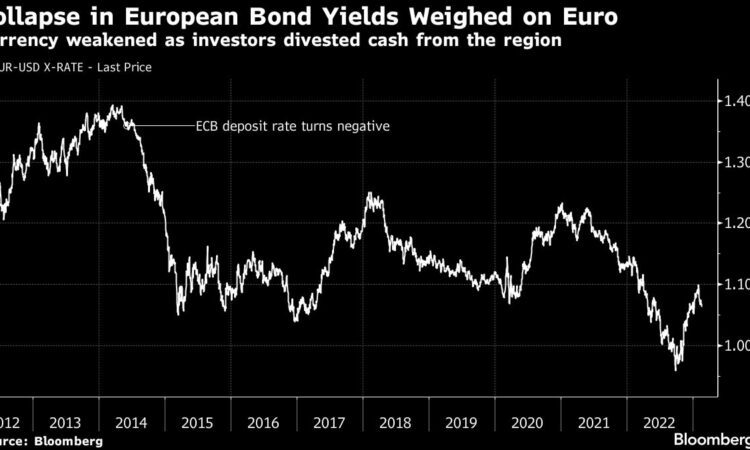

The ECB kept interest rates negative for years to slash borrowing costs and hoovered up trillions of bonds, first to battle stagnant growth and then the Covid outbreak.

Investors balked, cutting the share of euro-denominated bonds in European investment funds by 14 percentage points between 2014 and 2021 — ultimately creating an underweight position equivalent to half a trillion euros, according to Deutsche Bank’s strategists.

Closing the Gap

Now, with yields at their highest in years and sentiment toward fixed income far more positive as the ECB catches up with the Federal Reserve’s rate increases, net flows are poised to turn positive, the Deutsche Bank data suggest. Money markets are pricing almost 125 basis points of further ECB hikes compared with an additional 75 basis points in the US.

“There will be a closing of the gap between the Fed and ECB rates,” said Paul Jackson, global head of asset allocation research at Invesco Asset Management Ltd. “That is why the euro probably will continue to strengthen throughout this year.”

The u-turn in flows is a key factor underpinning Deutsche Bank’s bullish long-term view, even as a resurgent dollar has forced the pair lower this month. The euro was trading around $1.07 on Friday, down from a recent peak of $1.1033 on Feb. 2.

The bloc’s December balance of payments, published on Friday, pointed to an improving euro flow picture, said Jordan Rochester, FX strategist at Nomura. In addition to portfolio inflows, the current account — boosted by lower energy prices — ticked up further to a €16 billion surplus.

To be sure, any repatriation of capital to the euro area is likely to be a multi-year process that will ebb and flow: outflows were easing in the years before the pandemic, only to accelerate under a new round of stimulus that drove down yields once again.

And common debt sales — seen as another potential catalyst for a major inflow of capital — are likely still years away. That’s even as calls for joint issuance ramped up after the Ukraine war underscored the urgent need to boost investment in defence and energy security.

Other positive factors are still in play.

The cost for foreign investors to hedge US debt holdings has rocketed, eroding their returns just as yields in their home markets start to look more attractive. That’s likely to drive a repatriation of capital to Europe just as it has for Japan, where investors offloaded a record amount of overseas debt last year.

With lower energy prices helping the EU’s current-account surplus grow back, it’s not unthinkable the euro could eventually return to its pre-QE trading range, according to Kit Juckes, chief global FX strategist at Societe Generale SA. The shared currency hit a decade-high of $1.40 in 2014.

“The ECB crowded European investors out of European bonds, and is now effectively letting them back in,” he said.

Next Week:

-

Focus will be on February surveys of purchasing managers in the UK and the euro area, with investors looking for clues on how far central-bank hike cycles might extend

-

Bank of England officials making an appearance include Catherine Mann, Jon Cunliffe and Silvana Tenreyro and the European Central Bank will hold a non-monetary policy meeting in Finland

-

Euro-zone sovereign issuance is set to slow to around €25 billion, according to Commerzbank AG strategists, with auctions scheduled in countries including Germany and Italy

-

In the UK, it will be a heavy week of supply, with the BOE undertaking medium- and short-dated gilt sales under its quantitative tightening program alongside government auctions of bonds maturing in 2029 and 2053

–With assistance from Libby Cherry.

Most Read from Bloomberg Businessweek

©2023 Bloomberg L.P.

{kind=link}