Key takeaways

- The BIS global liquidity indicators (GLIs) show a slight drop in US dollar-denominated foreign currency credit overall in Q4 2023; US dollar credit to EMDEs, however, grew by $12 billion.

Global liquidity indicators at end-December 2023

The BIS global liquidity indicators (GLIs) track total credit to non-bank borrowers, covering both loans extended by banks and funding from global bond markets. The latter is captured through the net issuance (gross issuance less redemptions) of international debt securities (IDS). The focus is on foreign currency credit denominated in the three major reserve currencies (US dollars, euros and Japanese yen) to non-residents, ie borrowers outside the respective currency areas.5

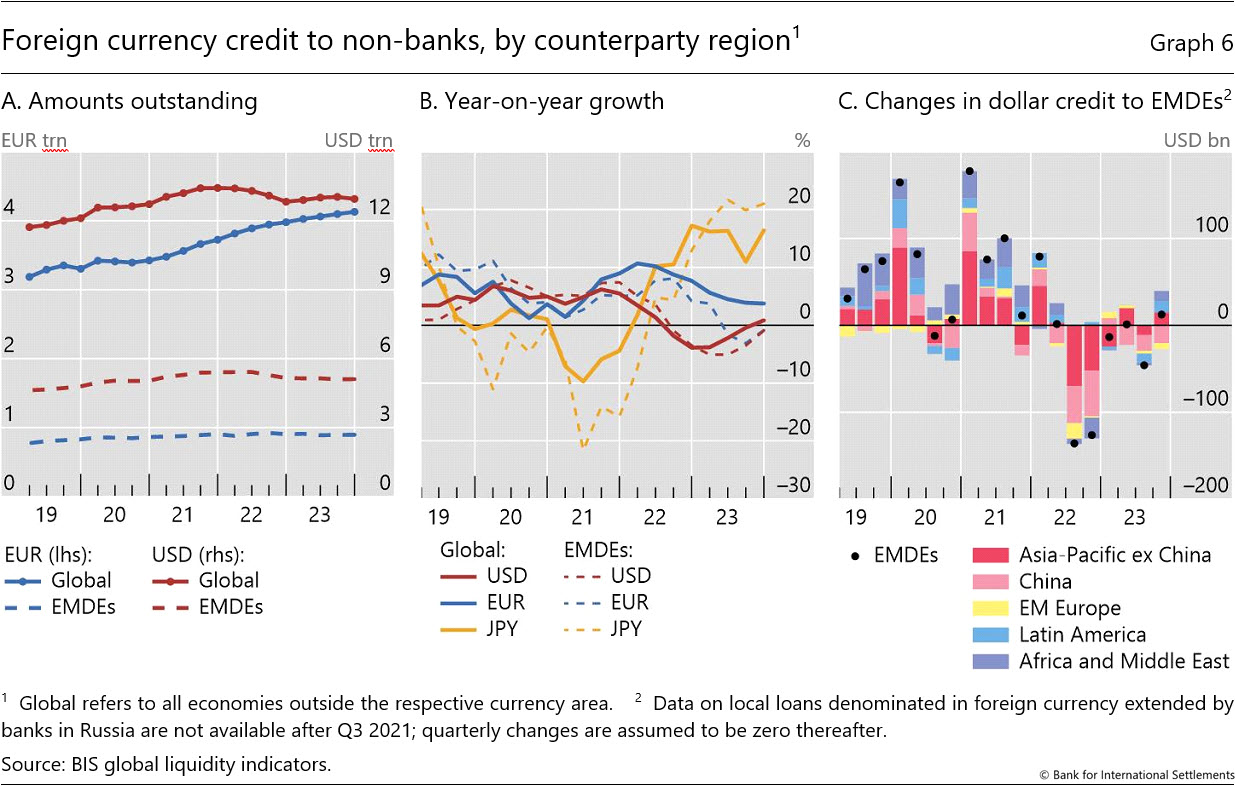

Foreign currency credit in US dollars inched down in Q4 2023, while euro- and yen-denominated credit increased. The $87 billion quarterly decline in US dollar-denominated credit to non-banks outside the United States left the outstanding stock just below $13 trillion. Nonetheless, the yoy growth rate turned positive due to base effects (Graph 6.B, red lines). Euro-denominated credit to non-banks outside the euro area increased by €31 billion, which pushed the stock of credit just above €4.1 trillion ($4.6 trillion), or 4% higher than a year earlier (Graph 6.A, blue lines). Following a pause in the previous quarter, yen-denominated credit outside Japan accelerated in Q4 due to a surge in bank loans. The outstanding stock, at ¥64 trillion ($451 billion), was up 16% from a year earlier (Graph 6.B, solid yellow line).

Dollar-denominated foreign currency credit to non-banks in EMDEs showed signs of recovery in Q4 after several quarterly declines since 2022. The $12 billion increase in credit left the amount outstanding at $5.1 trillion (Graph 6.A, dashed red line). Nevertheless, yoy growth remained negative at -0.9% (Graph 6.B, dashed red line). Looking across regions, dollar credit to borrowers in Asia-Pacific excluding China rose the most in Q4 (+$15 billion), followed by credit to those in Latin America (+$13 billion) and Africa and the Middle East (+$12 billion); by contrast, credit to China fell by $20 billion (Graph 6.C).

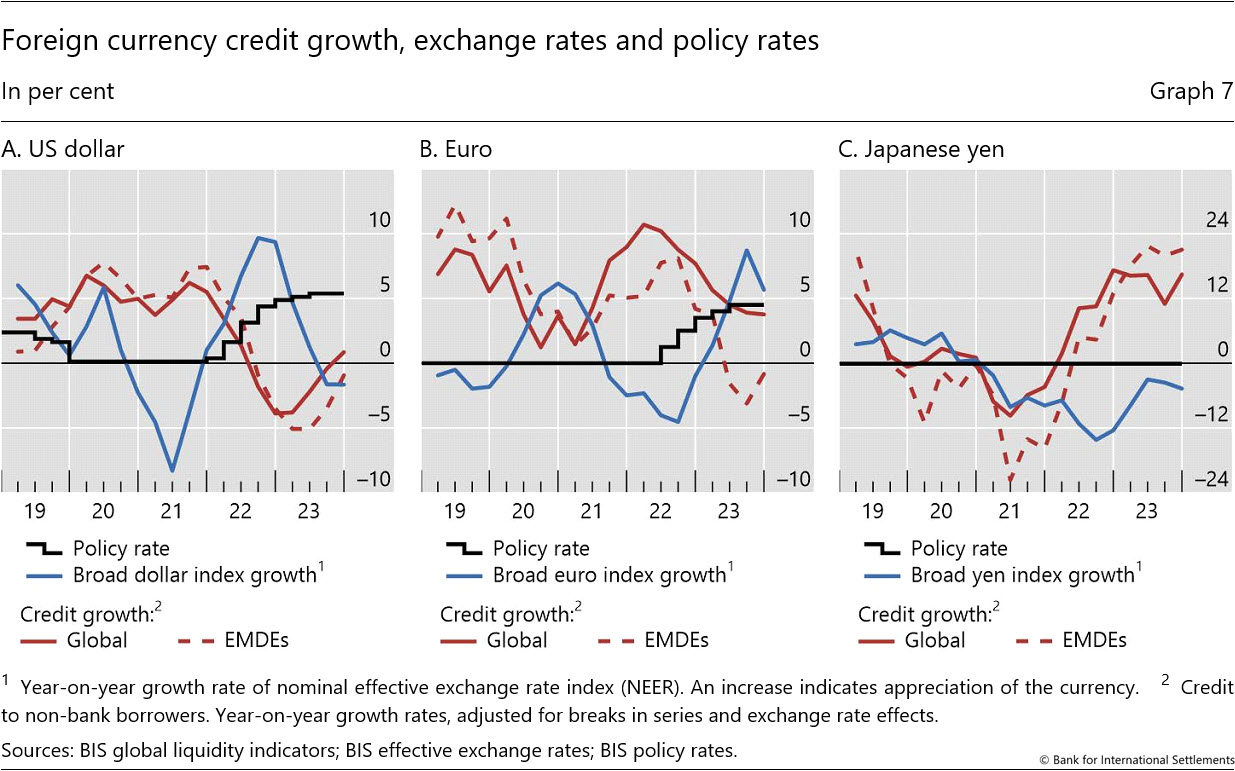

The differences in credit growth across the dollar, euro and yen reflect their respective funding costs and associated exchange rate developments. The negative co-movement between exchange rate indices and credit growth has been salient over the past few years (Graph 7). Monetary policy tightening by the Federal Reserve led to a stronger dollar throughout 2022, weighing on dollar-denominated bank lending and bond issuance. The European Central Bank’s policy tightening triggered a similar pattern in euro credit growth from mid-2022 onwards. Moreover, brisk growth in yen credit from early 2022 onwards went hand in hand with sustained yen depreciation as the Bank of Japan kept interest rates below zero.6

The negative co-movement between exchange rates and credit growth was particularly evident for EMDEs. The 0.9% yoy decline in dollar credit to EMDEs at end-Q4 2023 stood in contrast with the 0.9% global increase. The discrepancy was more striking for euro credit. In Q4, euro credit to all borrowers outside the euro area grew by 3.8% yoy, yet euro credit to EMDEs shrank by 0.8% yoy. Finally, yen credit to EMDEs continued to grow at 21% yoy, compared with a global pace of 16% yoy. Nevertheless, as monetary policy tightening slowed in the United States and euro area in 2023, annual growth rates of credit began to converge towards those of the global aggregates.

{kind=link}