LONDON, April 19 (Reuters) – The euro and pound are being whisked along by a conveyor belt of interest rate hikes in Europe just as U.S. rates near a peak, a reversal of the trends that drove them to multi-decade lows last year.

The two currencies have rallied 4-5% against the dollar since March as market ructions triggered by banking stress die down and signs of resilience in Europe’s economies draw investors back.

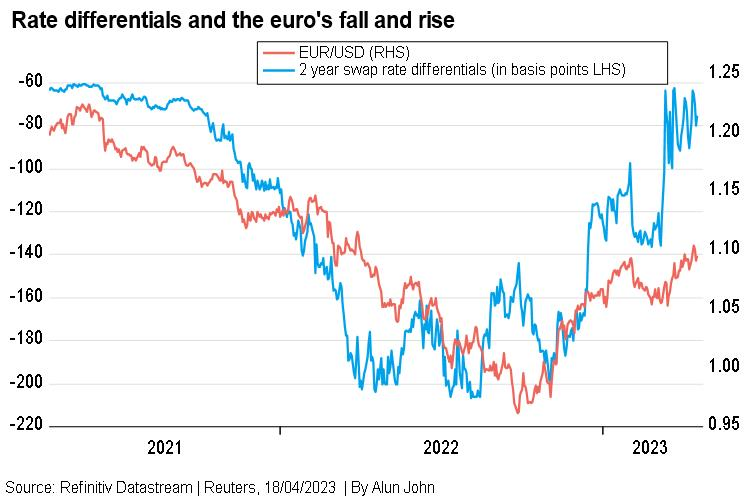

The euro , which traded below $1 in September, a two-decade low, is now worth around $1.10, close to its highest in more than a year.

Sterling has rallied 20% from record lows hit in September to trade near 10-month highs above $1.24. Europe’s other major currency, the Swiss franc, is also near its strongest in over two years .

Driving the momentum, and likely future strength, is the view that U.S. interest rates are close to peaking, while borrowing costs in Europe – where inflation is stickier – have further to climb.

“In the U.S. you’re starting to price for (rate) cuts pretty soon, in the second half of this year, whereas you have modest pricing for that in Europe and the UK,” said Tim Graf, State Street Global Markets’ head of macro strategy for EMEA.

Traders are pricing in one more 25-basis-point U.S. rate hike in May, followed soon after by cuts. But markets expect another 75 bps of European Central Bank rate hikes, with the deposit rate rising to a peak in the autumn.

Data this week showed British wages and inflation both rose faster than anticipated last month, with inflation over 10% – the highest in western Europe.

As a result, Morgan Stanley analysts now expect a 25 basis point rate hike from the Bank of England in May, and see “clear risks of a June move too”.

Expectations for higher official interest rates typically drag money market and government bond yields higher, attracting investor cash into a country and boosting its currency.

Higher rates can also reflect the health of an economy – central banks try to keep rates low in times of stress.

State Street’s Graf said historically it is changing rate differentials that particularly affect currencies, not just the outright yield level.

The gap between 10-year bond yields in Germany, the euro zone benchmark, and U.S. Treasuries narrowed 15 bps last week to around 103 bps, its tightest since April 2020 and down from over 200 bps in November .

The U.S. and German two-year bond yield gap last week reached its smallest in 17 months, while the gap between dollar and euro two-year swap rates, closely tracked by currency analysts, is near its lowest in two years. ,

“The case for continued narrowing is strong. European wage and price inflation is higher than the U.S., which historically is equivalent to European yields being at least as high as the U.S. across the yield curve,” Deutsche Bank Research said.

“An interest rate differential that is flat between the two regions would be equivalent to a euro/dollar move up to around 1.20.”

BMO Capital Markets forecasts the euro at $1.12 and the pound at $1.27 in the next three months because of the gap between U.S. and European rate expectations.

Nomura forecasts the euro will surge to $1.14 by the end of June and tips sterling to hit $1.30 this year.

TURNAROUND

The Federal Reserve’s relentless rate hikes sent the dollar to 20-year highs last year as other big central banks moved more slowly.

The U.S. currency was further boosted by demand for safe-haven assets following Russia’s shock invasion of Ukraine, fears about economic growth, particularly in Europe, and high costs for energy, which is priced in dollars.

After lifting rates to 4.75-5% from near zero in 2022, the Fed began slowing the pace of its tightening towards year-end. Markets now bet it will soon pause, before starting to cut borrowing costs by year-end as U.S. inflation falls and banking woes raise recession risks.

That should help the euro strengthen further against the dollar, M&G Investments fund manager Eva Sun-Wai said, while noting that any new crisis could give the greenback fresh impetus: “We also have the question of what dominates: rate differentials or safe-haven status?”

In Britain, still-high inflation means further rate hikes are almost certain.

It’s an outlook that is finally benefiting sterling, which took a beating last year but has been a standout performer among G10 currencies in 2023 even with March’s market turmoil.

“The UK is an open economy and has a very open financial system so it would by definition be affected (by a big systemic global shock), said Barclays’ head of currency research Themistoklis Fiotakis.

“But interestingly last month has seen the pound stronger, because of limited spillovers and declining U.S. and European rate expectations.”

Additional reporting by Naomi Rovnick, Editing by Dhara Ranasinghe and Catherine Evans

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}