Jan 5 (Reuters) – Silvergate Capital Corp (SI.N) reported a sharp drop in fourth-quarter crypto-related deposits on Thursday as investors spooked by the collapse of FTX pulled out more than $8 billion in deposits, sending shares down more than 42%.

The crypto-focused bank also said it would cut its workforce by 40%, or about 200 employees, as it tries to rein in costs amid a deepening industry downturn. Its stock was last trading at $12.55.

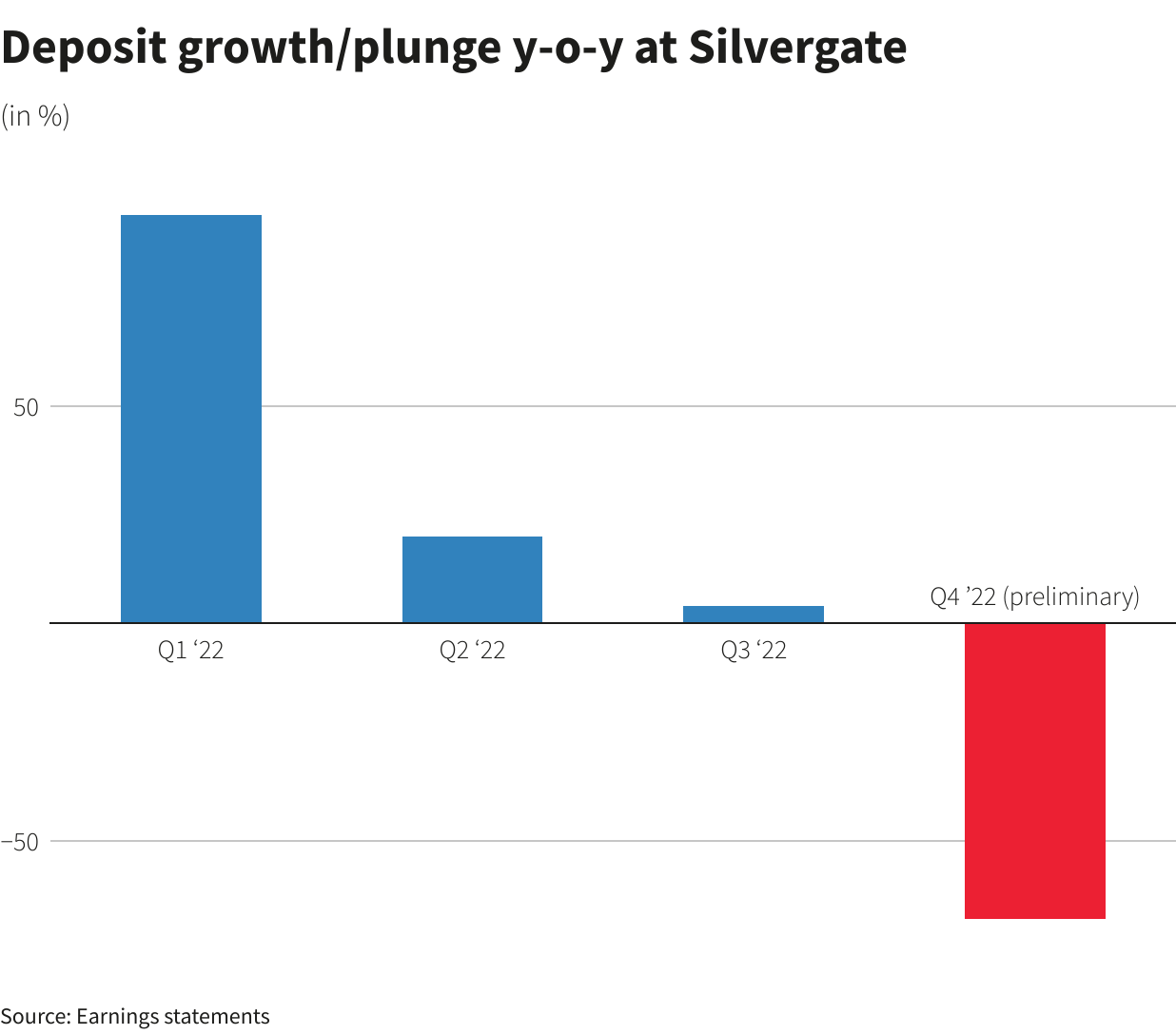

The dire preliminary earnings report shows the extent of the impact on the digital asset industry from the downfall of crypto exchange FTX, which filed for bankruptcy in November after failing to cover customer withdrawals, marking a stunning reversal of fortunes for what was one of the world’s biggest crypto exchanges.

Total deposits from digital asset customers at Silvergate declined to $3.8 billion at the end of December, compared to $11.9 billion at the end of September. The company sold $5.2 billion of debt securities at a loss of $718 million in the fourth quarter to maintain liquidity.

Silvergate had said earlier it had no outstanding loans or investments in FTX, but its shares have shed 69% of their value since the exchange’s meltdown, which sparked a wild crypto sell-off.

A U.S. attorney told a bankruptcy court on Wednesday that prosecutors had seized U.S. bank accounts at Silvergate and Farmington State Bank affiliated with FTX’s Bahamas-based business, known as FTX Digital Markets.

Court records show the accounts at Silvergate Bank and Farmington State Bank, which does business as Moonstone Bank, held about $143 million.

On Tuesday, FTX founder and former chief executive officer Sam Bankman-Fried pleaded not guilty to eight criminal counts including wire fraud and money laundering conspiracy. The 30-year-old is accused of looting FTX customers’ deposits to support his Alameda Research hedge fund, buy real estate and donate millions of dollars to political causes.

“We are in a period of ‘shoot first, ask questions later’ for any bad news related to crypto and crypto-related businesses,” said Thomas Hayes, chairman and managing member at investment firm Great Hill Capital.

“We expect this carnage to continue for some time as there is no way to value the underlying asset.”

Slowing the expansion of its business, La Jolla, California-based Silvergate is also delaying the launch of a blockchain-based payment solution it had purchased from Meta Platforms Inc-backed Diem Group last year.

The bank said it would take an impairment charge of $196 million in the fourth quarter on assets purchased for the payment solution venture.

Total deposits from digital asset customers at Silvergate declined to $3.8 billion at the end of December, compared to $11.9 billion at the end of September. The company sold $5.2 billion of debt securities at a loss of $718 million in the fourth quarter to maintain liquidity.

Several U.S. lawmakers have questioned the relationship between Silvergate and Bankman-Fried’s crypto firms.

In a December letter to Silvergate CEO Alan Lane, Senators Elizabeth Warren, John Kennedy and Roger Marshall expressed concern that Silvergate may have facilitated the transfer of FTX customer funds to Alameda, and requested information on the bank’s anti-money laundering compliance program.

In a conference call with analysts on Tuesday, Lane said Silvergate “absolutely” follows all know-your-customer and Bank Secrecy Act requirements, which instruct banks to report suspicious activity.

“The misinformation out there is candidly very frustrating,” Lane said. “We follow the Bank Secrecy Act, the USA Patriot Act for every account that we open, and we conduct ongoing monitoring.”

Given the reduction in headcount, the impairment charge and “future potential for regulatory actions as it relates to FTX/Alameda wires, I would imagine Silvergate is definitely exploring strategic options at this point, including a potential merger/sale,” said Ben McMillan, chief investment officer at IDX Digital Assets.

Silvergate declined to comment on whether it would pursue any strategic options.

On Tuesday, U.S. bank regulators issued a joint statement warning banks of risks associated with cryptocurrency, adding that they had concerns with the safety and soundness of bank business models that are highly concentrated in crypto.

Founded in 1988, Silvergate ventured into crypto in 2013. The bank counts major exchanges like Coinbase Global Inc (COIN.O) and Kraken among its customers.

The bank had also operated a mortgage warehouse business, but announced in December that it would be winding down that division, citing the rising interest rate environment and reduction in mortgage volumes.

Reporting by Manya Saini and Niket Nishant in Bengaluru and Hannah Lang in Washington; Editing by Subhranshu Sahu and Nick Zieminski

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}