The regulation of businesses selling digital currency in the US is inconsistent, and the only agreed-upon regulation of the industry treats the businesses as money transmitters. This regulatory approach is a poor fit—especially for exchanges—because many trades in cryptocurrency or other digital assets are arguably securities or commodities transactions.

But how to characterize specific transactions is a topic of heated debate between the industry and the government and within the federal government.

Federal legislation for national digital asset standards remains stalled, even for payment products like stablecoins, where a recent House hearing on the topic devolved. The current uncertainty regarding regulation has left much of the prudential regulation of sellers of digital currencies to state money transmitter regulators, where they have jurisdiction.

However, having the state money transmission regulatory system as the default source of capital and liquidity regulation leaves the market with ill-fitting rules that are, in the scale of the crypto firm life cycle, too slow. Eventually the debate over what is a security and how to regulate stablecoins will resolve, but until then, money transmission laws can’t be relied upon to save the day, and the risk of an exchange being grossly undercapitalized through market fluctuations or fraud remains.

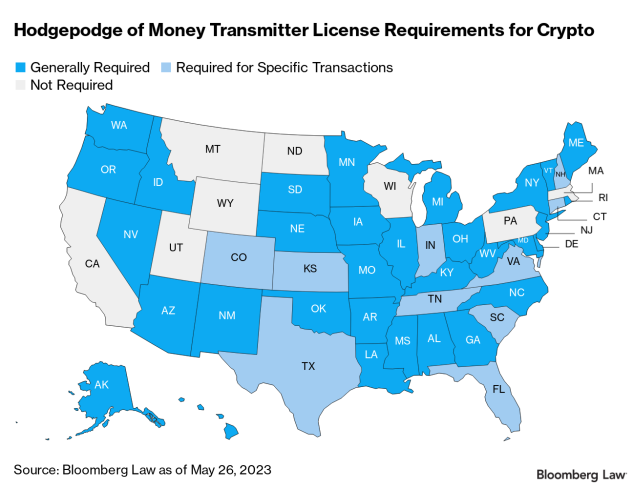

State Regulation of Crypto Transactions

Most states require domestic money transmitters to maintain a license, and of those states, the majority consider at least some, if not all, transactions in cryptocurrencies to be money transmission.

What kind of entity requires a license varies by state. For example, in Washington, regulations equate virtual currency to money for purposes of licensure. In Connecticut, cryptocurrency exchanges require licensure, but sales of digital currency from one’s own supply—often through an ATM-like machine—are exempted, expressly or by a no-action letter. In Texas, trading in digital currency generally is not considered money transmission, but stablecoins and third-party facilitation of digital currency purchase with sovereign currency are considered to be money transmission.

Regardless of the variations, the breadth of transactions on a cryptocurrency exchange like Coinbase or Binance.US will require a money transmission license in every state that mandates one for some digital asset activity. A money transmitter licensee needs to maintain certain prudential standards to ensure it can pay its obligations: a surety bond, a certain amount of assets exceeding liabilities, and a certain amount of assets in liquid or near-liquid “permissible investments” to immediately pay obligations.

The state money transmission regulatory system has functioned well for payment processors, even fintech ones like PayPal and Square. But so much of digital currency and digital asset trade is investment in a fast-moving marketplace, and the current regulations can’t keep up.

Reaction, Not Investigation

Crypto money transmitters can follow several business models, from retail store vending kiosks like those of Coinme and Cash Cloud, to web-based trading platforms and creators of complicated financial products like Bittrex, BlockFi, FTV, and Voyager Digital. But no matter the type of crypto exchange, regulators tend to be reactive rather than proactive when a problem arises, and there’s little consistency in what triggers enforcement actions.

Bitcoin ATMs

This year, the “Bitcoin ATM” firms Coinme Inc. and Cash Cloud Inc.—businesses where consumers can exchange cash for cryptocurrency—were each suspended by a state regulator for being in violation of money transmission net asset requirements.

In both cases, the regulators were aware of the violations long before the suspension, and each business was given time to clean up its books. But the initiation of a multistate investigation into ATM service Coinme prior to any adverse filings is one of the few times regulators claimed proactive investigation. For Cash Cloud, Florida learned about the business’s net asset deficiency from mandatory periodic reporting. Cash Cloud reported negative net assets in April 2022.

Major Crypto Exchanges

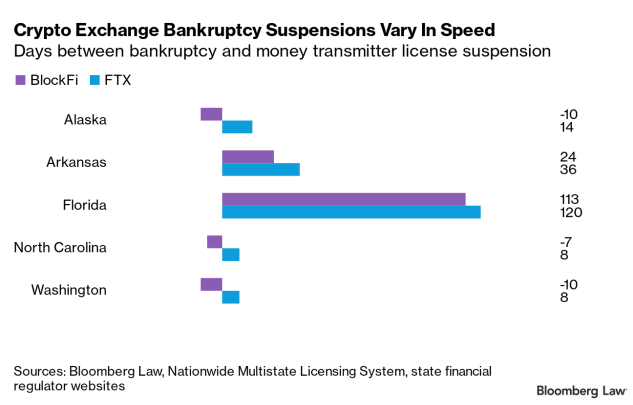

In the past year, four major cryptocurrency exchanges licensed as money transmitters have gone bankrupt: Bittrex, BlockFi, FTX US (the American trading arm of FTX), and Voyager Digital. They’ve all been suspended from money transmission by at least one state, but the timing of the suspensions has varied—in some cases drastically.

Texas began the investigation leading to suspension upon learning of a net asset deficit by Bittrex prior to its bankruptcy. Although the suspension order doesn’t specify when the state learned of the deficit, the most likely situation is that the deficit was disclosed in periodic reports.

For FTX and Voyager Digital, money regulators didn’t take enforcement action until the bankruptcy filings. BlockFi suspended its money transmission services upon FTX’s bankruptcy in November of last year, two weeks before its own, and regulators began enforcement from the pausing of customer withdrawals. For some states, BlockFi’s enforcement action was “early” in terms of its bankruptcy—some states filed suspension orders over a week before BlockFi filed for bankruptcy. But BlockFi received a bailout loan from FTX in June of 2022, which in hindsight should have triggered investigation into its finances.

For a cryptocurrency ATM or similar direct sale, reaction is not ideal, but the risk to consumers and the market is relatively small. The businesses often encourage customers to use their own crypto “wallets,” so the business doesn’t maintain custody after the purchase like a broker or exchange does. The number of customers potentially at risk when the business fails is therefore lower. The ATMs also aren’t market makers like exchanges, so the risk of market-wide contagion if one fails is lower.

State Reaction Time Is Inconsistent

Compounding the reactive nature of money transmission regulators is that, depending on the state, suspension orders for noncompliant crypto businesses may issue only after a long investigation or negotiation—if at all.

State money transmission regulators generally give businesses time to cure their issues prior to enforcement orders. Florida allowed Cash Cloud to attempt a plan of corrective action until its bankruptcy in February 2023, after which the state suspended its license. North Carolina found that Coinme’s net assets were under the state’s $250,000 threshold on the last day of August 2022, but gave Coinme until December to cure the issue. The six-month period between Voyager Digital’s bankruptcy and its settlement with five states to cease operations was the result of efforts to remain operational until it was sold, a process in which the states were involved.

Even assuming that it was prudent to allow half a year to determine that Voyager Digital couldn’t continue responsibly as a money transmitter, Georgia took another three months to separately reach a similar settlement this March.

Unless the states actively work together on enforcement—which happens occasionally but not consistently—each state issues an order on its own time frame, creating a wide disparity in the timing of license suspensions, as the cases of BlockFi and FTX illustrate.

BlockFi, FTX Failures Linked

The failures of BlockFi and FTX were intertwined, as BlockFi was dependent on capital from FTX and prevented customers from accessing their money shortly after FTX’s bankruptcy. As a result, BlockFi and FTX often had orders issued on the same day or within days of each other, which for some states was a week or so after FTX’s bankruptcy but about a week before BlockFi’s bankruptcy. For other states, however, it took weeks if not months after both bankruptcies for an order to issue.

In some cases, regulators seemed to be waiting for airtight cases for suspension. Arizona’s suspension of FTX is an example. The order, issued 73 days after FTX’s bankruptcy, stated in its findings of fact not only that FTX was bankrupt, but also that its “control persons,” individuals defined by statute as having significant influence over the business, changed and the surety bond would soon be canceled.

Florida issued its order on March 14, 2023, 120 days after FTX’s bankruptcy, and based it on the November bankruptcy, suspension of payments to customers, the December indictment of former FTX CEO Sam Bankman-Fried, and the February superseding indictment.

The week after it suspended FTX, Florida declared an “emergency” suspension of BlockFi, 113 days after its bankruptcy, waiting like Arizona in the FTX case not just for the bankruptcy, but also for withdrawal of the required surety bond. Waiting to suspend the license of an infamous bankrupt entity to “belt and suspenders” the action with numerous technical license violations may allow for a less contestable order—especially when the organization is no longer operational—but the order then serves not as a consumer protection measure but as a bookkeeping measure.

There were pronounced delays even when the license suspension orders were consented to by the bankrupt exchange.

Pennsylvania executed a consent order within two weeks of FTX going bankrupt last November. South Dakota issued a consent order with FTX at the end of December 2022. Michigan settledwith FTX to allow its license to expire without renewal on January 1; North Dakota settled on the last day of February 2023; and Rhode Island’s consent order with FTX was signed this March. Given the apparent willingness of the operators of the bankrupt entity to agree to suspension with some states, the lateness of the execution of orders with others is hard to understand.

License Surrender

In some states, there’s no official enforcement order and the bankrupt crypto exchange surrenders its license on its own schedule. While Texas took action against Bittrex, the exchange had already publicly announced that it was winding down its US business, and all its other state license records maintained by the Nationwide Multistate Licensing System (NMLS) have the status, “Approved – Surrender/Cancellation Requested,” indicating a voluntary request to end licensure.

According to NMLS, BlockFi made surrender requests in the five states that didn’t issue explicit orders, and Voyager Digital surrendered its license in four states without an order from the state authority. The status dates by NMLS on many of these withdrawals are well within the first quarter of 2023. FTX US is still actively licensed in Iowa and Vermont, according to NMLS and a review of state enforcement orders.

While there are some states that are relatively quick to suspend exchanges with problems, or at least quickly upon obvious insolvency, the tendency of many states is to take the path of least resistance in a digital asset exchange’s failure.

Some of this delay can be excused with a “damage is done” or a “business is effectively defunct, speed doesn’t matter” argument, but those arguments highlight the unsuitability of money transmission regulation to provide adequate protection to the consumers and the market.

Bloomberg Law subscribers can find related content on our Fintech Compliance Practice Center.

If you’re reading this on the Bloomberg Terminal, please run BLAW OUT <GO> to access the hyperlinked content, or click here to view the web version of this article.

{kind=link}