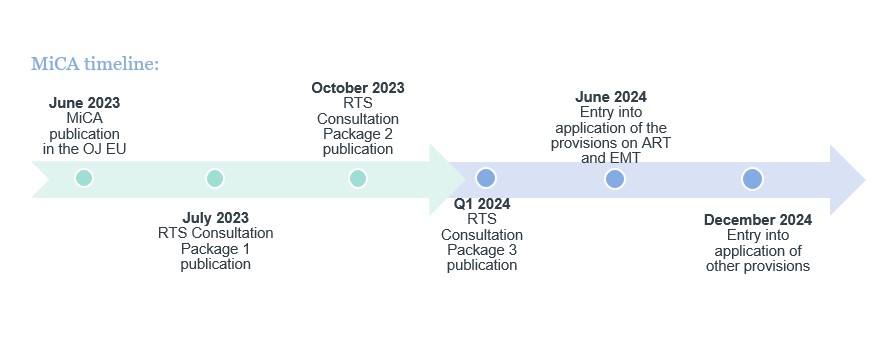

On 9 June 2023, MiCA was officially published in the Official Journal of the European Union (OJ EU L 2023, No. 150, p. 40 as amended; “MiCA”) .

The new regulation aims to foster use of innovative technologies by setting a regulatory framework that covers crypto-assets, crypto-assets issuers and crypto-asset service providers. EU regulations are directly applicable in all EU members states, so implementation procedures are limited.

MiCA was proposed as a part of the digital finance package which also included a digital finance strategy (COM/2020/591 final), the Digital Operational Resilience Act (DORA) (OJ EU L 2022, No. 333, p. 1; “DORA”), that covers crypto-asset service providers as well, and a proposal for a regulation on a pilot regime for market infrastructures based on distributed ledger technology (OJ EU L 2022 No. 151, p. 1; the “DLT Pilot Regime”).

MiCA entered into force on 29 June 2023 and will become applicable in part (provisions regarding asset-referenced tokens and e-money tokens) from 30 June 2024, and in other parts from 30 December 2024. Currently there are legislative procedures undertaken on the EU level related to MiCA delegated acts (Regulatory Technical Standards and Implementing Technical Standards).

Crypto-assets defined

The EU lawmakers decided to provide a general definition of a crypto-asset, stipulating that it is a digital representation of a value or of a right that is able to be transferred and stored electronically using distributed ledger technology or similar technology.

Then, MiCA divides crypto-assets into three categories:

- asset-referenced tokens (“ART”) – a type of crypto-asset that is not an electronic money token and that purports to maintain a stable value by referencing another value or right or a combination thereof, including one or more official currencies;

- electronic money token (“EMT” or “e-money tokens”) – a type of crypto-asset that purports to maintain a stable value by referencing the value of one official currency;

- tokens that are qualified as neither ART nor EMT; this category includes utility tokens – a type of crypto-asset that is only intended to provide access to a good or a service supplied by its issuer.

MiCA further divides ARTs and EMTs into significant and non-significant tokens based on several criteria, such as inter alia: the number of holders, the value of issued token, the significance of the activities of the issuer on an international scale (e.g., use of the token for payments and remittances).

What about NFTs?

MiCA explicitly excludes crypto-assets that are unique and not fungible with other crypto-assets. Therefore, in relation to most NFTs, MiCA will not apply. However, MiCA may apply to NFTs whose characteristics make it more likely to be fungible (e.g., NFTs issued in series or as a collection).

What is out of scope?

Even though MiCA forms a comprehensive regulatory framework for crypto-assets and related activities, not all assets that could potentially qualify as crypto-assets fall under the scope of MiCA.

Thus, the MiCA Regulation does not apply, for example, to the following types of assets , which qualify as:

- financial instruments;

- deposits, including structured deposits;

- funds, except if they qualify as e-money tokens;

- unique and not fungible with other crypto-assets (as stated above, that includes certain NFTs);

- non-life or life insurance products;

- social security schemes.

An issue worth noting in particular is the exclusion from the scope of MiCA of cryptocurrencies that qualify as “financial instruments”. This means that so-called “security tokens” are not covered by the MiCA Regulation. However, given that EU law does not contain a clear legal definition delineating the essence of “financial instruments”, distinguishing between crypto-assets falling under MiCA and those not falling under MiCA is difficult. Accordingly, ESMA has been required to issue guidelines by 30 December 2024 on the conditions and criteria for the qualification of crypto-assets as financial instruments.

Furthermore, MiCA does not cover crypto-asset services, which are fully decentralised . Thus, for example – the world’s most well-known cryptocurrency, that is Bitcoin – is not itself regulated by the MiCA Regulation.

CASPs

MiCA distinguishes a new category of entities within the EU financial regulatory framework, which are crypto-asset service providers (“CASP”). MiCA defines CASPs as legal persons or other undertakings whose occupation or business is the provision of one or more crypto-asset services to clients on a professional basis, and that is allowed to provide crypto-asset services (e.g., custody services, operating of a trading platform, exchanging crypto to fiat or providing advice on crypto-assets) in accordance with MiCA.

MiCA provides for licence requirements for CASPs, which is a novelty since up to now most EU countries required simple registration and compliance with local AML laws. The authorisation for CASPs is granted on an application submitted to the competent authority in the home country.

Regarding the territorial scope of the MiCA – of course it will apply to activities within the EU. However, interestingly – MiCA also explicitly provides for the provision of crypto-asset services by entities not licensed in the EU. Thus , a client established or situated in the EU may initiate at its own exclusive initiative the provision of a crypto-asset service or activity by a third‐country firm. In such situations, the requirements for authorisation envisaged in MiCA do not apply to the provision of that crypto-asset service or activity by the third‐country firm to that client . This model of providing financial services is known in EU regulations as “reverse solicitation”.

As of now, for the purpose of actively providing services in various EU member states, CASPs need to register in each EU member state. So, the good news is that, under MiCA, a CASP licence obtained in one EU member state may be passported to another.

ART issuers

ART issuers are obliged to obtain authorisation that is granted upon application submitted to the competent authority in the home country. There are also exceptions to the rule – authorisation is not required if: (i) the issuer is a credit institution or (ii) the value of issued tokens does not exceed a certain threshold or (iii) the offer is addressed solely to qualified investors and the asset-referenced token can only be held by such qualified investors.

Even though credit institutions are not required to obtain authorisation to issue ART, MiCA imposes certain obligations on credit institutions, such as inter alia drawing up a whitepaper and notifying the respective competent authority 90 days ahead of issuing ART.

EMT issuers

EMTs may only be issued by credit institutions or e-money institutions, provided that such institutions notified the whitepaper to the competent authority.

There are also several restrictions related to EMTs. Firstly, EMT issuers can redeem EMTs for their holders at any time and at par value, by paying in funds. Secondly, EMT issuers cannot grant interest in relation to issued EMTs.

Issuers of crypto-assets other than ART or EMT

MiCA also introduces requirements for the issuance of tokens that do not qualify as ART or EMT, though they are not as far reaching as the requirements for EMT issuers.

The requirements for issuers of crypto-assets other than ART or EMT do not apply if the crypto-assets are offered for free. In addition, the requirements for issuers of crypto-assets do not apply when:

- the crypto-asset is automatically created as a reward for the maintenance of the distributed ledger or the validation of transactions;

- the offer concerns a utility token providing access to a good or service that exists or is in operation; or

- the crypto-asset holder has the right to use it only in exchange for goods and services in a limited network of merchants with contractual arrangements with the offeror.

Investor protection

MiCA contains a number of measures aimed at protecting investors’ funds, as well as ensuring that the investor is well aware of what is the characteristic of the crypto-asset, such as inter alia:

- Whitepaper – issuers of crypto-assets are obliged to prepare and publish a whitepaper that contains certain information required under MiCA. Depending on what type of token it relates to, such information may include inter alia information: (i) about the offeror or the person seeking admission to trading, (ii) about the token, (iii) about the issuer, (iv) about crypto-asset project, (v) on the risks or (vi) on the underlying technology, etc.

- Marketing communications – all marketing communications relating to an offer to the public or admission to trading of the crypto-asset should comply with certain requirements, such as inter alia: (i) being fair, clear and not misleading, (ii) being identifiable as such and (iii) being consistent with the whitepaper.

- Honesty, fairness, professionalism – issuers and CASPs are obliged to act honestly, fairly and professionally.

- Own funds – ART issuers are obliged to keep the own funds on a certain level.

- Safeguarding of funds – EMT issuers are obliged to safeguard the funds received in exchange

for e-money tokens by depositing and investing them in a manner described in MiCA. - Reserve of assets – ART issuers are obliged to keep reserve of assets securing the claim against the issuer. MiCA also provides for certain restrictions related to the composition and management of such reserve of assets.

{kind=link}