EU Crypto Customers Will Have Holdings Reported to Tax Authorities: How to Stay Compliant

- A recently adopted EU directive will force crypto firms to share information about their customer’s transactions with tax authorities.

- The new rules are designed to crack down on tax avoidance.

- While EU tax authorities will soon be able to share information on people’s crypto holdings, different rulebooks apply in each member state.

Tax authorities have often struggled to keep on top of the fast-moving, cross-border nature of cryptocurrencies. In the EU, this challenge is further complicated by the existence of multiple overlapping tax regimes and the increasingly mobile working lives of many EU citizens.

In the latest update to the European tax system, the Eighth Directive on Administrative Cooperation (DAC8 ) was formally adopted by member states on Tuesday, October 18. As part of the new rules, crypto exchanges will be obliged to report their customers’ holdings to tax authorities, who can then share the information with each other.

Cracking Down on Crypto Tax Avoidance

In a statement announcing the adoption of new tax rules, the EU said DAC8 “will improve Member States’ ability to detect and combat tax fraud, avoidance, and evasion, by requiring all EU-based crypto-asset service providers [to] report transactions from customers residing in the EU.” The updated directive is designed to complement the Markets in Crypto-assets (MiCA) regulation, the statement added.

The new crypto asset reporting framework established DAC8 will bring the EU crypto industry in line with the broader financial sector, where the automated sharing of information with tax administrations has been in place for years.

Going forward, tax authorities will now adopt practical arrangements for the new reporting and information-sharing regime.

What do New Rules Mean For Investors

For crypto investors, the new rules won’t change the underlying tax system or the amount of tax they have to pay.

However, once DAC8 is implemented, authorities will be better equipped than ever to catch accidental or intentional discrepancies in individuals’ tax filings. And many investors may want to update their accounting practices to ensure everything is in order.

In most EU countries, investors must pay capital gains tax on any profit they make selling cryptocurrency for fiat. Meanwhile, self-employed traders and people who receive their salary in crypto have to pay income tax.

When it comes to remaining tax compliant, the most important thing to remember is that EU citizens pay taxes in their country of residence. That means that regardless of where the crypto exchange or bank account you use to purchase digital assets is based, what matters is the rules where you are domiciled.

The Diverse Landscape of EU Tax Rules

While EU authorities are increasingly harmonized in their approach to reporting and sharing information, tax systems still vary wildly between member states.

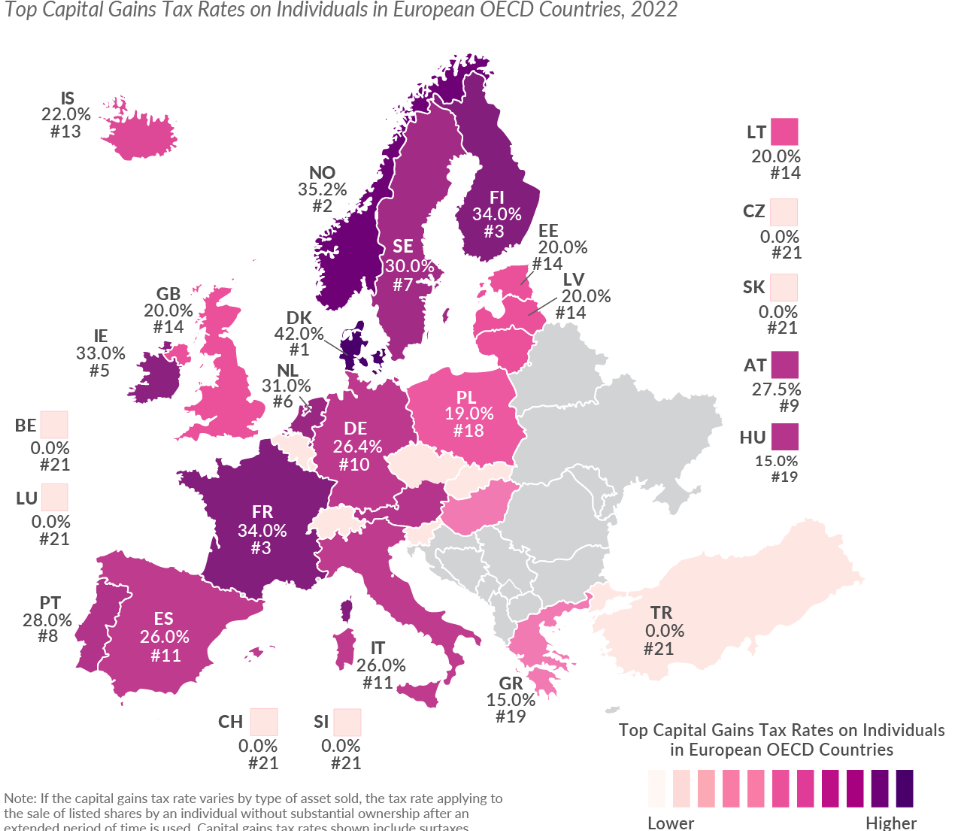

For example, Denmark levies the highest capital gains tax of all EU countries, at a maximum rate of 42%. At the other end of the spectrum, Hungary and Greece charge just 15% tax on all capital gains.

Meanwhile, countries including Belgium and Luxembourg subsume profits made from selling assets into income tax, which typically range from zero up to 40%-50%, depending on annual earnings.

Finally, although not generally known for low taxes, Germany actually operates one of the most favorable tax regimes for crypto investors.

Under German rules, assets bought and sold within the space of a year are subject to income tax, but cryptocurrencies held for longer than a year can be sold tax-free.

Was this Article helpful?

{kind=link}