LONDON, Nov 17 (Reuters Breakingviews) – Tighter cryptocurrency regulation is inevitable after the collapse of exchange FTX. Even so, there will still be places that the rules don’t touch. Big players like Binance, as well as services based on so-called decentralised finance, may stay out of reach. That ensures the edgier aspects of crypto will live on.

Sam Bankman-Fried’s now-bankrupt company transferred $10 billion of customers’ money to cover losses at its sister hedge fund, according to Reuters, which also reported that at least $1 billion has vanished. That blows apart FTX’s pledge to users that their deposits “shall at all times remain with you.” The obvious regulatory fix is to force crypto companies in future to hold customer funds in whatever form they were deposited, rather than using the money to trade or make loans.

The European Union’s mammoth crypto regulation would help. Known as MiCA and recently agreed by lawmakers, the rulebook forces custodians to segregate clients’ crypto holdings from the firm’s own assets. Two bills introduced this year by U.S. senators also contain prohibitions against this practice, known as “co-mingling”. The common aim is to make sure that users’ assets, whether held in bitcoin or a token pegged to a real-world tender like the dollar, are available when they want to withdraw.

But it’s unclear whether watchdogs – which in the EU will be national financial regulators, and in the United States would most likely fall to the Commodity Futures Trading Commission – could enforce it across the board.

The first risk is that they won’t capture decentralised finance projects. This corner of crypto, where developers write software to facilitate automated trading and lending products typically over the ethereum blockchain, is by definition free from middlemen. According to the website DefiLlama, so-called DeFi has over $40 billion of total value “locked,” crypto-jargon for money deposited in decentralized exchanges and other services. It’s borderless and often pseudonymous, making it hard to police. Security firm Chainalysis reckons almost three-quarters of stolen crypto in 2021 was taken from DeFi services.

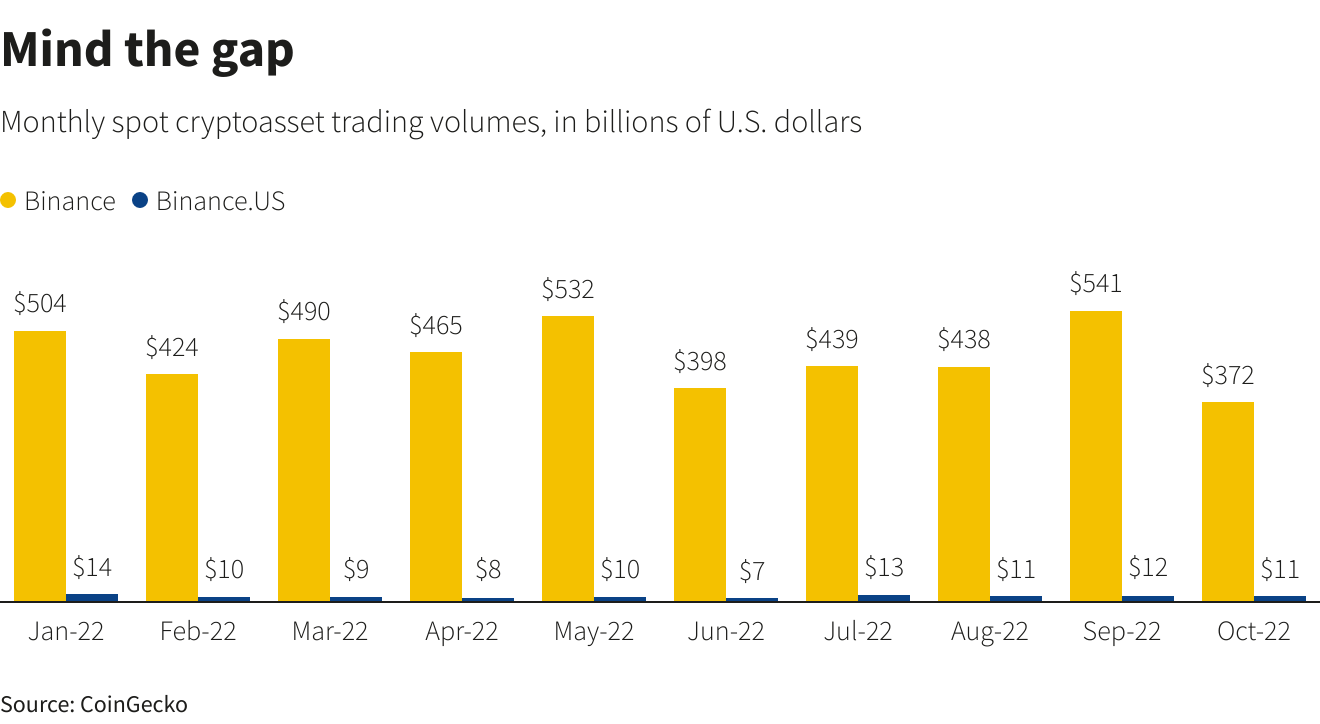

The second problem will be pinning down companies based elsewhere. Take Binance, by the far largest crypto exchange. It has an affiliated American business, Binance.US, but that company is tiny relative to the parent. The danger is that regulators in their back yard can’t see what’s happening in someone else’s. Global co-ordination has proved challenging on other issues like minimum corporate tax rates; a common framework for something as complex as crypto is a pipe dream.

The industry’s best hope is that regions with clear, customer-friendly rules will attract big institutional money and protect retail traders. But borders are porous, and money finds a way to where the biggest rewards are on offer. Bankman-Fried initially said the U.S. division of FTX was insulated from the problems at his Bahamas-based exchange. Still, on Friday it filed for bankruptcy alongside the wider group. The coming wave of regulation may protect the good, but it won’t stop the reckless.

Follow @liamwardproud on Twitter

(The author is a Reuters Breakingviews columnist. The opinions expressed are his own.)

CONTEXT NEWS

FTX suffered a “severe liquidity crisis” that led to its bankruptcy, according to court filings dated Nov. 14. The collapsed cryptocurrency exchange could have more than 1 million creditors.

FTX filed for bankruptcy on Nov. 11, after traders rushed to withdraw $6 billion from the platform in just 72 hours and rival exchange Binance abandoned a proposed rescue deal.

Bitcoin was trading at roughly $16,600 at 0835 GMT on Nov. 17, compared with around $20,500 at the start of the month.

Editing by John Foley and Streisand Neto

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.

{kind=link}