The following is an extract from S&P Global Market

Intelligence’s latest Week Ahead Economic Preview. For the full

report, please click on the ‘Download Full Report’ link.

Inflation updates for the US, UK, Eurozone, Japan and

Canada

Into the final weeks of 2023, more inflation data will keep the

markets occupied with CPI numbers out of the UK, Eurozone, Japan

and Canada while the US updates core PCE data. Additionally, final

Q3 GDP updates will also be due from the US and UK while central

bank meetings in Japan and Indonesia are also anticipated.

The final Fed meeting of the year fuelled further rate cut

expectations with the market having almost fully priced in 50 basis

points of rate cut by May according to the CME FedWatch tool. This

was as the Fed signalled the possibility of easing monetary policy

by 75 basis points in 2024, recognising that inflation has eased in

recent months. Indeed, the latest S&P Global Flash US PMI

continued to outline the likelihood for CPI to head lower despite

the economy gaining some momentum in December amid loosened

financial conditions (see special report). US core PCE will

therefore be in focus while other high frequency releases,

including the US personal income and spending, durable goods

orders, and building permits, are also updated for a check on

November conditions. Separately, Q3 GDP will be updated, though

this will be a backward-looking piece of data.

Meanwhile November UK, Eurozone and Japan inflation figures are

anticipated with

PMI price data having hinted at further cooling of underlying price

pressures. Japan’s inflation figures will be among the

highlights, especially with the Bank of Japan (BoJ) widely expected

to exit their negative interest rate regime, albeit not in the

upcoming meeting on Friday, December 22. Rhetoric from the meeting

coupled with the upcoming inflation indications from Japan will be

closely watched for the yen – especially with the BoJ seen to be an

outlier central bank, set to hike rates while global central banks

including the Fed move in the opposite direction.

Besides the Bank of Japan, Bank Indonesia will also convene

though no changes are expected. Meeting minutes from the Reserve

Bank of Australia will also be due for insights into central

bankers’ thoughts amid still-elevated inflation in Australia and

softening growth conditions.

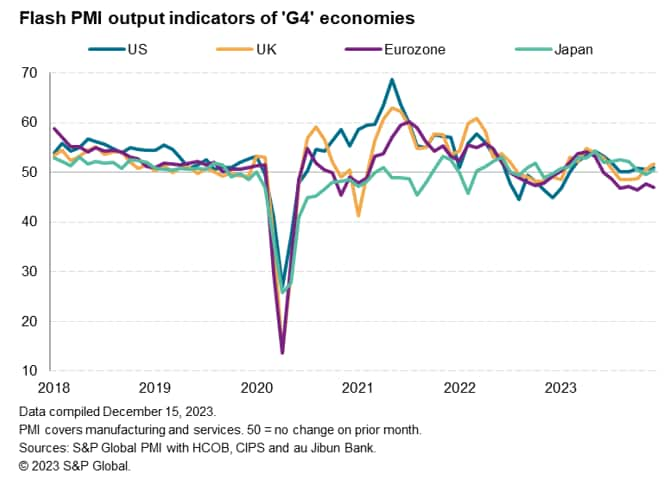

Flash PMI data signal widening growth divergences

Early PMI survey data for December from S&P Global showed

the major developed economies collectively stagnating. However,

trends varied, with the eurozone slipping deeper into decline to

signal a recession, but modest growth was seen in the UK, Japan and

US.

The surveys continue to indicate that service sector growth

remains very subdued in the G4 on average relative to the growth

surge seen in spring and summer, but looser financial conditions –

based on expectations of lower interest rates in 2024 – have

benefitted the US and UK in particular as 2023 draws to a close.

Manufacturing, in contrast, remains firmly in decline, with output

falling across all four economies, dropping most notably in the

eurozone.

Further falls in backlogs of work in both sectors meanwhile bode

ill for the near-term outlook, but also hint at some potential

further cooling of inflation. Service inflation remained elevated

by historical standards, most noticeably in the UK, and the

upcoming dataflow in this sector will be key to help assess policy

developments in 2024.

For our full recap of the PMIs in 2023, download our

“Shifting Sands” report.

Key diary events

Monday 18 Dec

Singapore NODX (Nov)

Germany Ifo Business Climate (Dec)

United States NAHB Housing Market Index (Dec)

Tuesday 19 Dec

Australia RBA Meeting Minutes

Japan BOJ Interest Rate Decision

Malaysia Trade (Nov)

Eurozone Inflation (Nov, final)

United Kingdom CBI Industrial Trends Orders (Dec)

Canada Inflation (Nov)

United States Building Permits (Nov, prelim)

United States Housing Starts (Nov)

Wednesday 20 Dec

Japan Trade (Nov)

China (Mainland) Loan Prime Rate (Dec)

Germany GfK Consumer Confidence (Jan)

Germany PPI (Nov)

Turkey Consumer Confidence (Dec)

United Kingdom Inflation (Nov)

Switzerland Current Account

Taiwan Export Orders (Nov)

Eurozone Current Account (Oct)

Eurozone Consumer Confidence (Dec, flash)

United States Current Account (Q3)

United States CB Consumer Confidence (Dec)

United States Existing Home Sales (Nov)

Canada BoC Summery of Deliberations

Thursday 21 Dec

Indonesia BI Interest Rate Decision

France Business Confidence (Dec)

Hong Kong SAR Inflation (Nov)

Turkey TCMB Interest Rate Decision

Canada Retail Sales (Oct)

United States GDP (Q3, final)

Friday 22 Dec

Japan Inflation (Nov)

Japan BoJ Meeting Minutes (Oct)

Thailand Trade (Nov)

Malaysia Inflation (Nov)

United Kingdom Retail Sales (Nov)

United Kingdom GDP (Q3, final)

France Consumer Confidence (Dec)

Spain GDP (Q3, final)

Taiwan Unemployment Rate (Nov)

Italy Business Confidence (Dec)

Canada GDP (Oct)

United States core PCE (Nov)

United States Durable Goods (Nov)

United States Personal Income and Spending (Nov)

United States New Home Sales (Nov)

United States UoM Sentiment (Dec, final)

* Access press releases of indices produced by S&P Global

and relevant sponsors

here.

What to watch

Americas: US core PCE, Canada inflation data and US

building permits, personal income and spending and final Q3 GDP

update

Post the December Fed meeting, US core PCE will be in focus in

the coming week. This comes after US CPI eased to 3.1% in November

while core CPI inched up slightly to show a 0.3% monthly increase,

though both figures were in line with consensus expectations.

Separately, the US also releases a Q3 GDP update, in addition to

building permits, durable goods orders, new home sales, consumer

confidence and personal income and spending figures.

Meanwhile in Canada, November’s inflation figure will be due

Tuesday. Encouragingly, price indicators from the

S&P Global Canada Composite PMI suggested that input cost

inflation had eased in November.

EMEA: Eurozone, UK inflation data, UK retail sales and

final Q3 GDP, German GfK, Ifo survey data,

In the UK, November’s inflation figures will be released

Wednesday. Likewise for the UK,

PMI price indicators have hinted at a slight easing of price

pressure into November, though some stickiness may be observed

thereafter. Retail sales and final Q3 GDP will also be released,

with the former closely watched for any improvements in activity

into the final months of the year.

The eurozone will also update November inflation figures

following the preliminary headline and core CPI readings of 2.4%

and 3.6% respectively. Also watch out for Spain third quarter GDP

release and producer prices in Germany.

APAC: BoJ, BI meetings, RBA meeting minutes, Japan

inflation and trade data

In APAC, final central bank meetings of the year unfold in Japan

and Indonesia. The Bank of Japan will be in focus despite no

changes to the current negative interest rate setting being

anticipated at the upcoming meeting, as hinted by officials. This

is as the BoJ is set to hike rates by the end of April according to

market expectations, though central bankers remain vigilant of data

developments, placing the focus also on Japan’s inflation and trade

releases in the coming week.

Special reports

US flash PMI ends 2023 at highest since July amid looser

financial conditions – Chris Williamson

APAC manufacturing sector rebounds in late 2023

– Rajiv Biswas

Purchasing Managers’ Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{kind=link}