BRUSSELS, July 11 (Reuters Breakingviews) – Europe wants to keep its home-grown innovators from going abroad in search of new funding, not just new sales. Yet national barriers make the European Union’s single market more of a dream than a financing resource. Far from adding red tape, joined-up supervision is a benefit the EU could offer its entrepreneurs.

EU leaders regularly pay lip service to the importance of the “capital markets union” – a sought-after single market for finance – in their quest to boost competitiveness and rally economic resources. Rising trade tensions with China, and the EU’s own desire to bolster its economic security after the pandemic and the Ukraine war, have only underlined the importance of the project.

Yet the EU today is a long way from uniting its capital markets. Instead, innovators and established companies face a funding maze, split along national lines. Growing companies simply turn elsewhere, like Ireland’s exercise software maker Glofox, which sold out to Arkansas-based ABC Fitness Solutions in a 2022 deal.

European equity markets are less than half the size of their U.S. counterparts by market capitalisation, but the bloc has more than three times as many exchange groups, according to a 2021 report by London-based New Financial. The think tank calculated that Europe, including trading partners like the UK and Switzerland, has 22 different stock exchange groups operating 35 different exchanges for listings and 41 exchanges for trading. There are also nearly 40 different securities depositories and central counterparty clearing houses to look after the “plumbing” of financial markets. By comparison, the United States has seven exchange groups, three listings exchanges and 16 trading exchanges, along with one clearing house and one depository.

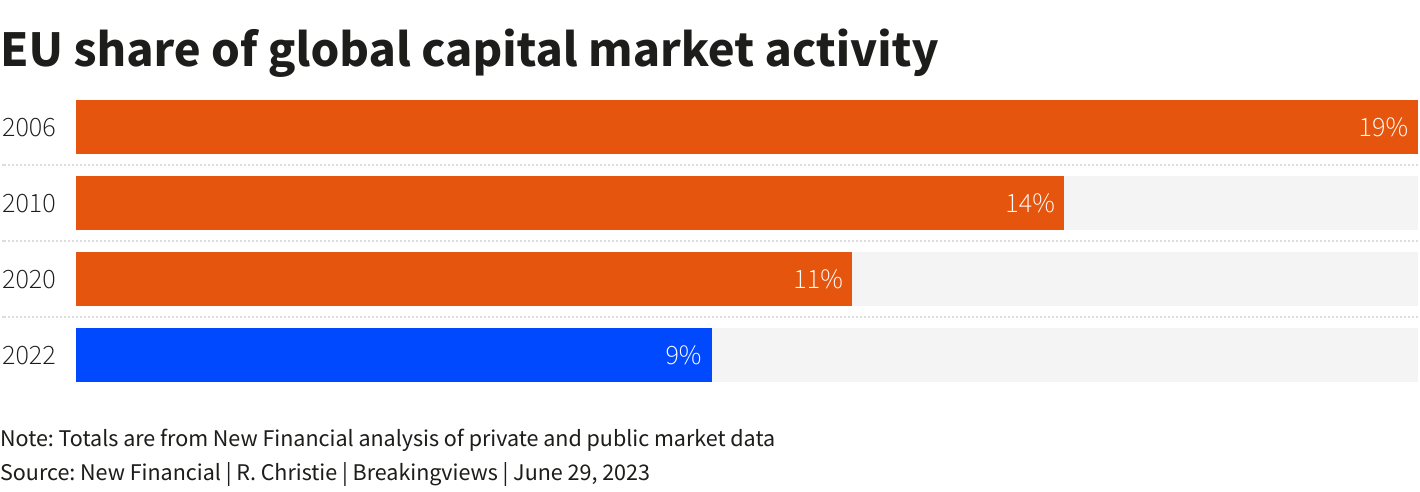

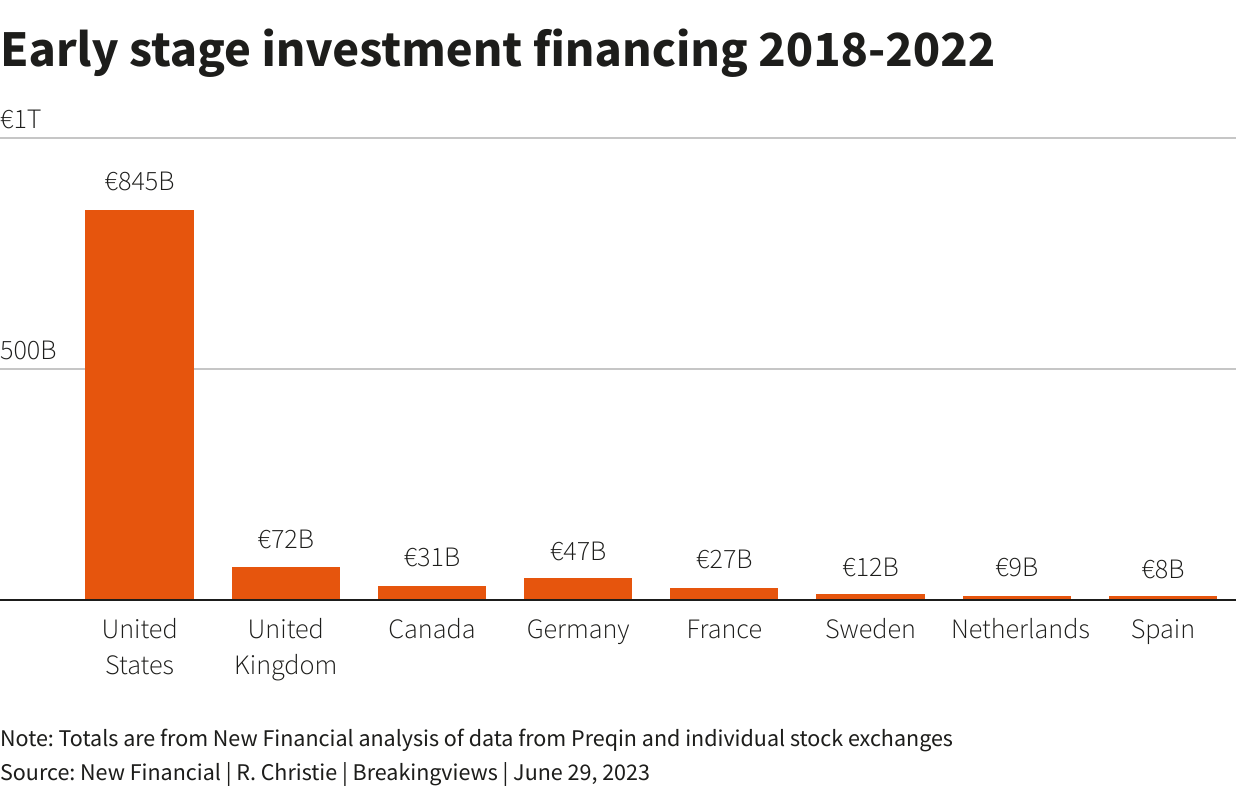

Fragmented markets mean less trading and fewer initial public offerings. That, in turn, pushes promising companies elsewhere when it’s time to grow. The EU’s share of global capital markets fell from 19% in 2006 to just 9% in 2022, according to New Financial’s analysis of sectors including venture capital, IPOs, pension funds, stocks and bond markets. Early-stage financing in Europe totalled 131 billion euros between 2018 and 2022, compared to 949 billion euros combined for the U.S., UK and Canada. Europe’s long-standing culture of risk aversion, dependence on bank loans and fragmentation have prevented its markets from keeping up with its economy, the world’s third biggest in terms of GDP.

Even when Europe does create unicorns, defined as a startup with a valuation of $1 billion or more, such as direct-retail aggregator Berlin Brands Group, Belgian software maker Collibra or French auto-sharing firm BlaBlaCar, they tend to be backed by outside money. A 2022 report from Austria’s i5invest found that there were 130 unicorns in Europe, including the UK, in 2021 – about a quarter of the U.S. total – but nearly half the funding came from non-European venture capitalists, mostly U.S.-based.

Unravelling Europe’s mind-boggling patchwork of national interests will take years of investment and political will. But regulation would be a good place to start. At present, core market oversight rests with EU member states, who also wield considerable influence over decision-making at the European Securities and Markets Authority, a Paris-based agency set up in 2011 that mostly coordinates rather than directly regulates.

This messy set-up contrasts with the EU’s successful switch to common oversight for big banks in 2014, a move that many credit for shielding the bloc from spillovers from the latest round of U.S. financial failures.

Proponents of the status quo say ESMA’s relative youth, combined with its over-reliance on national regulators, means it would not provide top-class independent supervision. So far, countries have only ceded power around the edges, for functions like credit ratings and trade repositories. The important players, such as broker-dealers, asset managers, exchanges and clearing houses remain supervised along country lines.

Yuriko Backes and Magdalena Rzeczkowska, the finance ministers from Luxembourg and Poland, wrote in May that more joint supervision would be “counterproductive” by constraining national expertise. Bigger countries have similar reservations: Spanish Deputy Prime Minister Nadia Calviño said she was “very favourable” towards common supervision – just not now.

“I don’t know if I would start by saying ESMA should be a supervisor, frankly,” Calviño said on June 7 in Brussels, even as she called for broader and deeper capital markets that could attract private money.

It’s true that supervision won’t create a central marketplace on its own, but it’s hard to see how the EU can move forwards without it. European policymakers talk a good game. A common market supervisor has been an official end goal since a 2015 report by the heads of the EU’s major institutions. A 2020 roadmap likewise called for integrated oversight. Yet political obstacles ranging from long-standing French and German rivalries to a broader distrust of Brussels in national capitals get in the way.

Getting private investors to step up means giving them room to work. In the area of sustainable investing, where the EU is a global leader, centralisation has shown promise. The European Commission itself is on track to be the world’s largest issuer of green bonds, and on June 13 Brussels proposed that ESMA should take over supervision for providers of environmental, social and governance (ESG) ratings.

Giving ESMA more powers over audit firms, cross-border market intermediaries and EU-based clearing houses would be a significant move towards allowing the regulator to grow up. The next step would be to change its governance. Right now, only national supervisors can be voting members of ESMA’s board. In the long run, it deserves to have a panel of independently appointed voting members, similar to the European Central Bank’s single supervisory mechanism for banks.

Changes like these would create a virtuous circle: if ESMA had more authority, it would attract better talent from EU member states. It also would help the EU put its money where its rhetoric is.

The EU needs innovation more than ever, to wean itself off fossil fuels and risky dependence on Chinese supply chains. Bringing capital markets together through better regulation, as well as better market incentives, could keep the next generation of unicorns home.

(The author is a Reuters Breakingviews columnist. The opinions expressed are their own.)

Follow @rebeccawire on Twitter

CONTEXT NEWS

European Union leaders called for the EU to improve capital markets as part of a push for competitiveness at summits in March and June.

The European Commission on June 13 proposed giving the European Securities and Markets Authority new powers to oversee providers of environmental, social and governance (ESG) ratings.

ESMA is an independent agency that sets regulatory standards, supervises some specific market areas, and coordinates among national securities regulators. It began operations in 2011.

Capital markets union is an EU endeavour launched in 2014 as a long-term project to boost investment across borders. A 2020 action plan calls for a move to integrated supervision.

Editing by Francesco Guerrera and Oliver Taslic

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.

{kind=link}