(Bloomberg) — The Bank of England this week is likely to resist signaling imminent interest rate cuts despite the arrival of new data that is expected to show inflation sinking to a 2 1/2 year low.

Most Read from Bloomberg

Governor Andrew Bailey and his colleagues are expected to leave the key rate at a 16-year high of 5.25% at their meeting on March 21. He’s been more cautious than the US Federal Reserve and European Central Bank in talking about a pivot to lower borrowing costs.

However, a drop in wage pressures coming from the labor market and a recession at the end of 2023 have left investors betting the BOE will cut rates before the end of summer. The latest reading on inflation due Wednesday could add fuel to those bets with the BOE’s 2% target now expected to be reached within months.

Following are seven charts shaping the nine-member Monetary Policy Committee’s thinking on when to move:

Inflation Goal

Britain’s inflation rate peaked at over 11% in October 2022 and has eased slowly since. After little progress in the last three months of data, a sharp fall in February is expected to be confirmed just a day before the BOE’s decision.

Economists expect inflation to sink to 3.5%, the lowest in 2 1/2 years, from 4% in January, according to a survey by Bloomberg as of Friday afternoon.

Cooling food and goods inflation will help drive the rate lower before a plunge in energy bills triggers a more marked step down in April, when economists expect it to dip below the BOE’s 2% target. Even with the target in sight, the UK central bank will be reluctant to declare its mission accomplished and is expected to leave its policy guidance unchanged. That points toward May as the time when officials give more tangible signals on timing.

Wage Growth

Rapid wage growth remains the biggest hurdle to an earlier pivot toward interest rate cuts. Bailey has expressed concern the tight labor market is feeding domestic inflationary pressure.

Here the BOE and economists are seeing signs of progress. Private sector pay growth excluding bonuses — the key earnings figure being monitored on Threadneedle Street — has fallen from a peak of over 8% last summer to 6.1% in the three months through January. Further declines are expected in the coming months.

“My big concern was that this duration would fuel the embedding of second round effects,” Bailey said in his final comments before the MPC decision. “Now tentatively these concerns I think have reduced.”

Pay Settlements

What may cause Bailey and the MPC pause for thought is that firms still expect to be handing out massive pay rises to hold onto and attract staff in a tight labor market.

At 6.1%, regular pay growth is still at levels that the BOE believes is not consistent with inflation hitting its 2% target sustainbably. However, the BOE’s recent survey of chief financial officers showed that firms expect to be handing out pay rises of above 5% over the next 12 months. That expectation has barely changed since last summer, and the BOE will be watching pay settlements for April closely.

Services Prices

The resilience of services inflation has also proved a headache for the BOE, as its rate-setters monitor it for signs of domestically-generated price pressures.

Higher wage and energy bills have helped drive up prices in the UK’s largest sector, though the BOE expects its strength to begin fading to open the door to rate cuts later in the year.

“Headline and services inflation have surprised the MPC slightly to the downside since the Feb. 1 meeting,” said Rob Wood, chief UK economist at Pantheon Macroeconomics. “Weaker-than-expected inflation and wages likely raise MPC confidence in a summer rate cut.”

Job Losses

Those concerns over continued sharp rises in wage bills may be overstated as other signals from the labor market point to a loosening that could shift the power from workers back to employers.

Unemployment edged up to 3.9% in the three months to January, marking the first increase in the jobless rate since last summer.

There could be more job losses on the way after the redundancy rate hit 4.6 per thousand workers — the highest since early 2021 and a doubling in a matter of months. Vacancies also continued to fall to just over 900,000, though this remains well above pre-Covid levels.

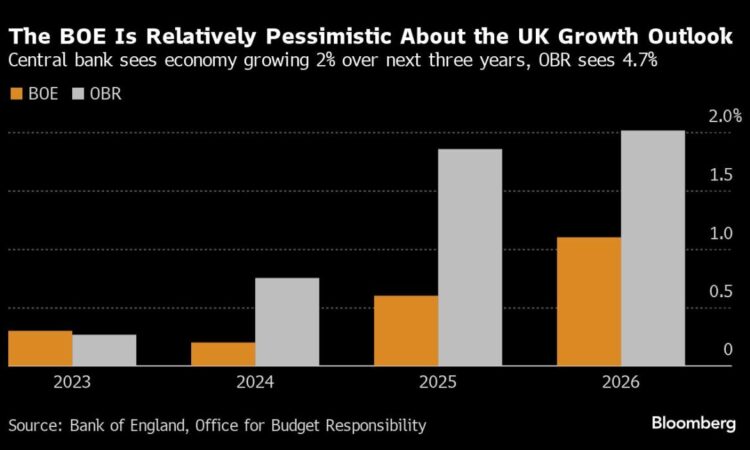

Sluggish Demand

While GDP data for January suggests that the UK economy quickly bounced back from 2023’s shallow recession, economists still expect a lackluster year for the economy.

Only a small pick-up from the meager 0.1% growth achieved last year is forecast in 2024 before the waning impact of its aggressive interest rate rises helps the economy accelerate in 2025 and 2026. Bailey played down the significance of the technical recession and pointed to signs of a modest recovery, though the subdued outlook for this year will help him contain wage and price pressures.

Inflation Bets

While market-implied inflation expectations are lower than they were in 2022 as CPI peaked, they continue to be above their long-term average. That point was made by the BOE in its Monetary Policy Report last month, which said it “will continue to monitor measures of inflation expectations very closely and act to ensure that longer-term inflation expectations are well anchored around the 2% target.”

Such market proxies have increased further above the BOE’s target since then, potentially warranting caution from officials. The five-year inflation swap rate — which measures the compensation investors demand to hedge against consumer price increase — has crept higher to 3%. That likely reflects investor expectations for fewer rate-cuts, with traders pricing only around three quarter-point cuts this year compared to six at the start of February.

–With assistance from Andrew Atkinson and Greg Ritchie.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

{kind=link}