At a Glance

- Fintechs and digital financial platforms have expanded in the small and midsize enterprise market, taking share from traditional banks.

- Banks could regain ground by understanding the pressing jobs to be done in each client’s industry and geography, and addressing those priorities rather than pushing products.

- Success here entails a customer-first perspective, seamless integration of different databases, and extensibility to incorporate many functions and capabilities within one system.

Banks have long struggled to serve small and midsize enterprises (SMEs) effectively, despite the prominence of these companies in national economies, as SMEs recently represented just over half of gross value added in the European Union and just under half in the US (see Figure 1).

Small and midsize businesses account for a major share of most national economies

Banks’ shortcomings opened the door for new fintechs and financial platforms, which in some cases have developed a better understanding of SMEs’ challenges around money management.

Banks tend to sell off-the-shelf financial products to SMEs without a deep understanding of their clients’ priorities and pain points. Although many bankers still believe they are at the center of the relationship with SMEs, most data shows a different reality. In 2022, for instance, digital challengers and specialists provided SMEs with £65.1 billion, or 55% of UK gross bank lending, estimates the British Business Bank.

Fintechs and digital financial platforms understand that a small firm looking for a loan considers more than just a low APR. Just as important is a loan delivered quickly and with repayment terms tailored to the company’s revenue flows. SMEs want to simplify their financial management through automated yet personalized digital experiences, an area where banks have been struggling.

The knowledge gap

Given the gap between the solutions that most banks offer and the challenges of cash flow and complexity that SMEs face, our experience working with the industry suggests that banks often don’t register top of mind for smaller firms choosing providers. For example, when Bain & Company interviewed almost two dozen business owners about how they managed their business finances, we found that all of them managed their cash flow in a software application different from their bank.

The Bain research suggests that the companies providing the most value to SMEs consist of accounting and payment platforms with a holistic view of money flows and critical business insights. Examples include QuickBooks and Xero for service-led customers and payments platforms Stripe and Square for retailers. These platforms have gradually expanded in the SME market because they design digital experiences around critical jobs such as managing cash flow and controlling expenses. Selling a financial product becomes a by-product embedded in the digital experience.

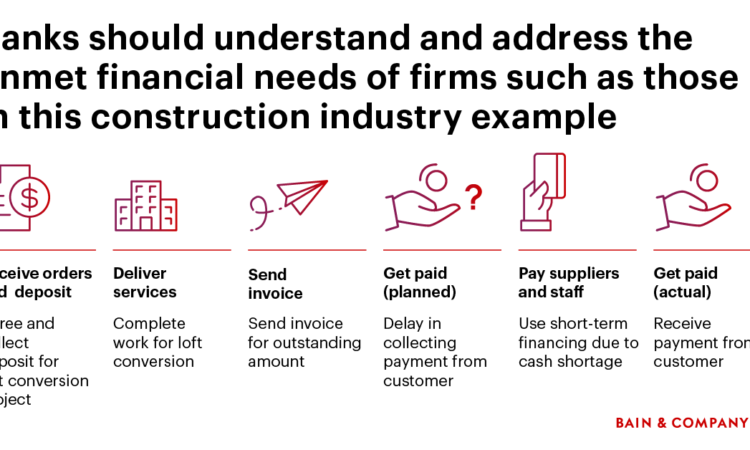

The pressing jobs to be done vary by the type of SME. Service-led businesses such as construction struggle with tracking invoices and getting paid on time, so they often use accounting tools to help shorten delays (see Figure 2). Transaction-led businesses such as e-commerce focus on making payments more efficient, because of their large transaction volumes. Very small enterprises prioritize cash flow management to ensure day-to-day survival. Midsize enterprises require support with data management and analysis because of the higher transaction or data volume. And international businesses contend with getting paid and paying in multiple currencies, along with meeting multiple countries’ regulations and tax rules.

Banks should understand and address the unmet financial needs of firms such as those in this construction industry example

The most successful digital-first challengers have made intelligent use of data and offer products emphasizing speed, flexibility, and accessibility. Critical to the design of products, whether they involve cash management or lending, is using data from the inflows and outflows of money. Having a holistic view of SME finances also provides data for more accurate risk scoring and loan pricing. Square’s success with SMEs thus derives in part from a full view of a client’s payment activities, which informs tailored loans with a repayment schedule that fits the client’s cycle.

Established banks do have ways to regain their footing. Even though fintechs have innovated heavily, they have not been able to solve all issues for SMEs. Many fintech offerings remain narrow, target niche customer segments, and often cannot meet the growing capital needs of more mature SMEs due to balance sheet constraints.

Most banks still possess diamond-in-the-rough assets: their large customer base, robust balance sheet, and mature teams in sales, finance, and operations. They can leverage these assets, while drawing inspiration from the best digital propositions developed by fintechs, to strengthen their competitive profile. But they will need to tailor their proposition to SME-specific needs and invest in an end-to-end digital experience informed by reliable data.

Succeeding with SME customers involves solutions that rely on three core characteristics:

With these characteristics incorporated into a more joined-up proposition, it’s easy to imagine how banks can improve their relevance among SMEs. Ambitious banks could even consider extending beyond strictly banking to help SMEs run their business. For a property rental company, such services could include tenant credit reports, rent collection, finding and purchasing a new investment property, and real-time analytics on key metrics with local benchmarks to help maximize investments.

As the legions of SMEs continue to grow, only banks that change their approach from product centered to customer and data centered will be able to tap into that growth.

{kind=link}