A look at the day ahead in U.S. and global markets from Mike Dolan

The benign July investment environment gets tested on Tuesday by updates on U.S. retail sales and housing while the corporate earnings season kicks back into gear with another sweep of bank reports.

Wall St ended in positive territory on Monday after a quiet trading day in which much of the focus centred on China’s wobbling economic recovery – where disappointing second-quarter growth readings saw banks rush to cut 2023 estimates.

Returning from a weather-related closure on Monday, Hong Kong stocks (.HSI) dropped 2% as real estate sector worries mounted when the world’s most-indebted property firm Evergrande released overdue results showing steep losses and liabilities.

The anxiety there contrasted with another positive surprise on U.S. economic sentiment, with New York Federal Reserve’s manufacturing index comfortably beating estimates for July – with reported prices paid falling and new orders picking up.

Goldman Sachs became the latest to chime with the ‘soft landing’ economic thesis and cut its probability that a recession will start in the next 12 months to 20% from an earlier 25% forecast – not far from what would be a routine chance of a recession starting on that horizon at any time.

Treasury Secretary Janet Yellen said she did not see a recession unfolding.

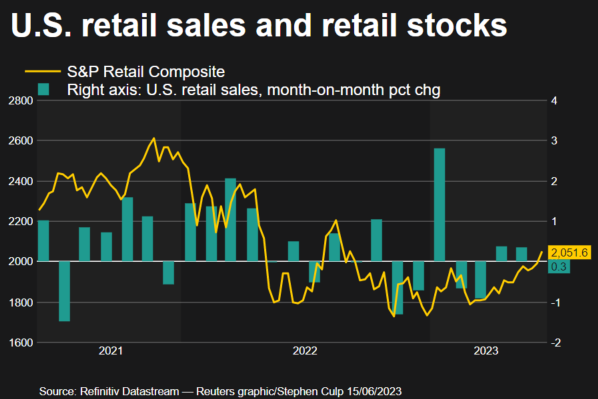

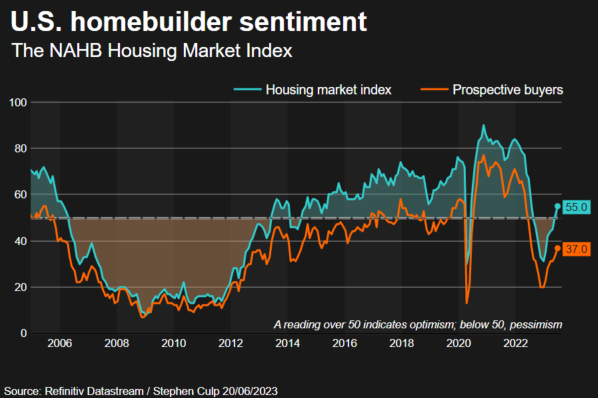

All that positivity will be held up to the light later on Tuesday as June retail sales data and a July homebuilder sentiment survey are released just as the latest sweep of corporate earnings reports from the likes of Bank of America, Morgan Stanley and Bank of New York Mellon emerge.

The first big bank releases last week showed reasonably rude health for the major firms in the second quarter, with some red flags about investment banking business, credit quality and real estate.

Consensus forecasts are for a modest rise in retail sales and industrial output last month, while the NAHB homebuilder index is expected to have ticked higher in July to underline the recent housing market recovery more broadly.

U.S. stock futures were flat going into the open and 10-year Treasury yields ticked down to their lowest level of the month so far. Crude oil prices tried to find their footing after Monday’s sharp drop and continue to sustain year-on-year losses of more than 25%.

The dollar (.DXY) was a fraction lower.

Elsewhere, Novartis (NOVN.S) climbed 2.7% after the drugmaker raised its full-year earnings guidance and mapped out a planned spin-off of its generic medicines division Sandoz.

Events to watch for later on Tuesday:

* U.S. corporate earnings: Bank of America, Morgan Stanley, Bank of New York Mellon, Lockheed Martin, Charles Schwab, PNC Financial, Omnicom, Prologis, Synchrony Financial, JB Hunt Transport

* U.S. June retail sales, industrial production, July NAHB housing market index, May business/retail inventories, May TIC data on overseas holdings of Treasuries, Canada June CPI inflation

* Federal Reserve Vice Chair for Supervision Michael Barr speaks

By Mike Dolan, editing by Christina Fincher, <a href=”mailto:[email protected]” target=”_blank”>[email protected]</a>. Twitter: @reutersMikeD

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.

{kind=link}