Nicht auf Deutsch verfügbar.

Published as part of the The international role of the euro, June 2023.

This box presents an early assessment of the changing role of the City of London for euro-denominated financial activities since Brexit.[1] Since its introduction in 1999, the City of London has been the leading financial centre for the international use of the euro in several market segments.[2] The decision of the United Kingdom in June 2016 to leave the EU was therefore seen as the portent of a potential change in the central role of the City of London for global financial markets.[3] This event was particularly relevant for euro financial activities that benefit from a harmonisation of rules and standards with the EU, such as trading in foreign exchange and OTC derivatives and banking services.[4] Data on these activities thus far, however, show no major shifts in the importance of the City of London for euro-denominated financial market segments, with some exceptions.[5]

In international banking, the expiry of the Brexit transition phase at the end of 2020 implied the discontinuation of the passporting regime. This directly impacted cross-border financial services – including euro-denominated services – provided to the EU single market. From a regulatory perspective, the United Kingdom’s exit from the EU in early 2021 implied its immediate reclassification as a non-EU country. This meant that UK-based banks wanting to provide services in the EU could no longer do this via passporting. Instead, they either would need to set up a subsidiary within the EU or alternatively rely on non-EU branches operating under national supervisory regimes, which cannot, however, provide services across the EU. In addition, the EU-UK Trade and Cooperation Agreement includes very limited commitments on financial services. The United Kingdom and UK-based international banks and financial service providers set up new subsidiaries in the EU-27, some of which fall under the direct supervision of European banking supervision, and to a lesser extent rely on third-country branches.[6] In that context, European banking supervision strictly follows its set of supervisory expectations, developed in 2018, on the relocation of international banks to the euro area.[7] This particularly concerns the “no empty shell” policy, under which foreign banks are requested to have suitable risk management capacities in line with their subsidiary’s level of risk.

More generally, in areas where an equivalence framework exists, cross-border financial services depend on unilateral equivalence decisions. Currently the EU has only granted temporary equivalence for UK central counterparties (CCPs) until June 2025, in line with the 2019 European Commission’s Communication on equivalence and based on recommendations by the European Supervisory Authorities.[8] In the future, further relocation of euro-denominated clearing activities from London to the EU can be expected in relation to measures aimed at reducing dependence on systemic non-EU CCPs and building EU-based clearing capacity.[9]

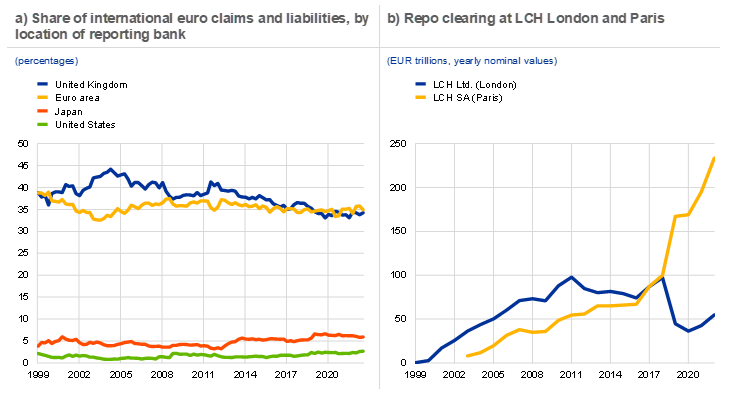

Banks that are resident in the United Kingdom continue to play a major role. Special Feature C signals that UK-resident banks remain central to the international network of loans denominated in euro, with potential signs of a Brexit effect in lending to non-bank financial intermediaries. In addition, they account for the largest share of euro-denominated cross-border assets and liabilities outside the euro area (see Chart A, panel a). The latest observation gives UK-resident banks a 34% share of euro-denominated international positions, only slightly (2 percentage points) below the level observed at the time of the Brexit vote in 2016.

However, euro area countries combined outstripped London in 2019, which can be attributed to the shift in euro repo clearing from London’s LCH Ltd. to its French subsidiary LCH SA in Paris (Chart A, panel b). This move is largely motivated by commercial considerations to consolidate euro repo and bond clearing in Paris to leverage on synergies with TARGET2-Securities.[10] In addition, following the decision of London’s ICE Clear Europe Ltd. to close down its clearing service for credit default swaps, a significant migration of euro-denominated credit default swaps to LCH SA in Paris has taken place.[11]

Chart A

Evidence on the impact of Brexit on international banking and euro-denominated repo clearing

Sources: BIS locational banking statistics, LCH Group and ECB calculations.

Notes: Banks’ cross-border and local (in euro) claims and liabilities combined, including loans and debt securities, but excluding derivatives. Figures have been adjusted to remove the impact of a break in series in the first quarter of 2018, when LCH SA joined the population of reporting institutions.

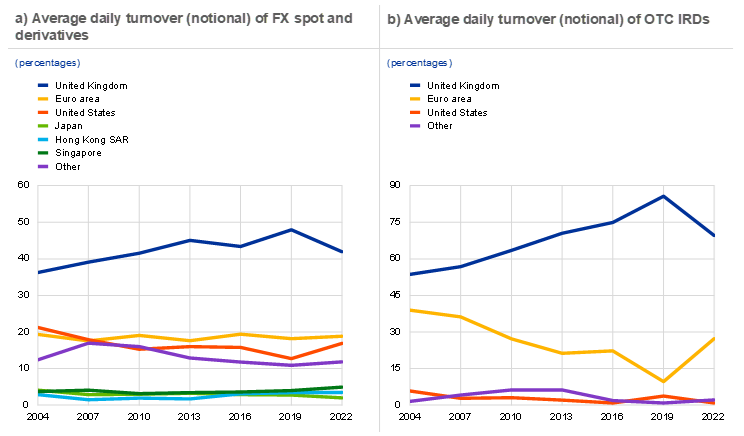

Turning to foreign exchange transactions, the latest BIS Triennial Central Bank Survey confirmed London’s dominant position in euro foreign exchange trading (Chart B, panel a). The UK financial markets accounted for around 42% of total transactions involving the euro in 2022. That is 6 percentage points lower than in the 2019 survey, but close to the level prevailing at the time of the 2016 Brexit referendum. This points to the City of London’s strengths in foreign exchange markets in terms of liquidity, legal system, market infrastructure and time zone. The United Kingdom remains more important for euro-denominated foreign exchange trading than the next five most significant financial centres (the United States, Singapore, Switzerland, Hong Kong and Japan) combined. The combined share of euro area financial centres in foreign exchange trading involving the euro increased from 13% in 2019 to 16% in 2022, in third position after the United Kingdom and the United States in this market segment.

One market segment which has seen notable decreases in euro-denominated activity since Brexit is the trading of OTC interest rate derivatives (IRDs). In line with its leading role in global foreign exchange markets, the City of London is still the principal trading centre for euro-denominated IRDs (mainly swaps and options; Chart B, panel b). However, its share in global trading of these instruments declined by almost one-fifth between the 2019 and 2022 surveys, to a level last seen ten years ago.[12] To a large extent, euro area financial centres have replaced the United Kingdom in this segment, increasing their share by the same margin.

To conclude, the role of the City of London for the international role of the euro is likely to evolve over the coming years, driven by future regulatory considerations both in the United Kingdom and the EU.[13] So far, there seem to be no major changes in market segments in which the United Kingdom is the largest non-euro area financial centre for the euro, with the potential exceptions of equity trading of EU-listed corporates, cross-border bank lending to non-bank financial intermediaries and euro OTC IRDs. This might, as regards central clearing, reflect the temporary regulatory arrangements which remain in place, such as the temporary regulatory equivalence for CCPs until June 2025. Future developments will depend (i) on the outcome of the ongoing EU legislative process that aims to reduce excessive reliance on UK CCPs and build up EU clearing capacity, (ii) on the extent to which EU and UK regulators can move towards more formal cooperation, and (iii) on the degree of divergence by EU and UK legislators with respect to regulatory changes ahead.