How much savings interest does YOUR bank pay? Average rate at big five revealed to still be dreadful…

- Five biggest banks pay an average of just 1.69% on £10,000 in easy-access

- This lagging the rest of the market average by a whopping 1.43%

- It is despite new rules which require them to offer savers ‘fair value’

The UK’s five biggest banks are still failing to offer competitive savings interest despite the Financial Conduct Authority’s Consumer Duty rules introduced last summer, new figures reveal.

Barclays, HSBC, Lloyds, Santander and NatWest are continuing to offer easy-access savings rates far below the market average, new figures from rates monitor Moneyfacts Compare reveal.

There is still an astonishing gap between the market-leading accounts, often offered by smaller banks and building societies, and the big banks’ easy-access rates.

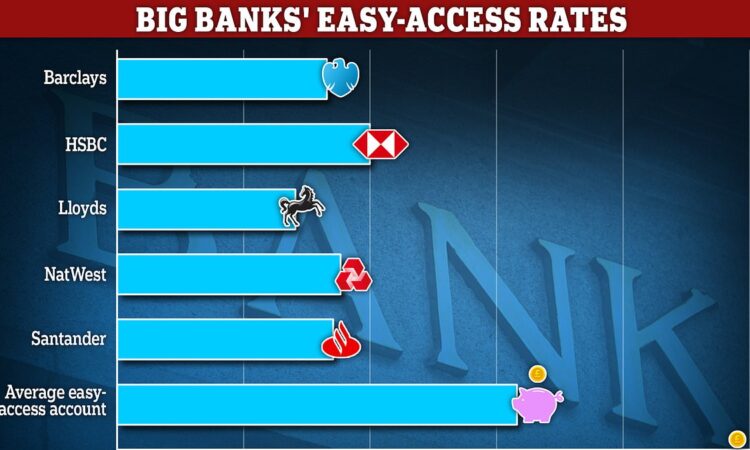

The five banks continue to offer savers easy-access accounts paying less than 2 per cent.

On £10,000 of savings, Moneyfacts figures show five of the UK’s biggest banks’ flexible easy-access accounts pay an average interest rate of just 1.69 per cent, lagging behind the market average for an easy-access account by 1.43 percentage points.

Lloyds Bank is the poorest performer, adding a mere 1.4 per cent to money savers tuck away in its easy-access deal, or £1.40 for every £100 saved.

HSBC’s flexible saver pays 1.98 per cent, while NatWest’s pays 1.74 per cent. Santander’s easy-access deal pays 1.7 per cent, while Barclays’ pays 1.65 per cent.

Related Articles

HOW THIS IS MONEY CAN HELP

This is despite the average easy-access rate being 3.12 per cent according to Moneyfacts. The best easy-access account pays 5.1 per cent.

It comes as the FCA is implementing its new Consumer Duty rules, which require banks and building societies to provide ‘fair value’ to savers.

James Hyde, spokesperson at Moneyfacts Compare said: ‘Consumer Duty regulations regarding existing products have been in effect since 31 July 2023, meaning companies have had almost a year now to review any previously uncompetitive products, and bring them into compliance with the rules laid out by the Financial Conduct Authority.

‘Unfortunately, the big five banks are still paying significantly sub-par variable savings rates. Their most accessible no-notice accounts all offer less than 2 per cent interest per annum – putting them all in the bottom fifth of the market.

‘Currently, a saver who put £10,000 in an easy access Isa offered by a big bank would lose out on £169 in interest each year (compared to the market average rate paid), or £344 (on a market-leading account).’

Banks are making more money on their OWN cash

Over 80 per cent of accounts on the market currently pay 2 per cent or higher on a £10,000 balance, according to Moneyfacts Compare.

This is Money analysed these banks’ easy-access rates in November and found that they paid savers an average easy-access rate of 1.85 per cent, so the average rate paid between them is now lower than November 2023.

Click here to resize this module

Lloyds’ easy saver rate of 1.4 per cent has not changed since November 2023. NatWest’s easy-access rate remains unchanged, as does Barclay’s and HSBC’s, while Santander’s was 2.5 per cent in November and is now 1.7 per cent.

Last month, figures from the Treasury Committee revealed NatWest, Barclays, Lloyds and Santander received more than £9billion in interest on Bank of England reserves in 2023 – a 135 per cent increase on the previous year.

Under quantitative easing, the Bank of England created £895billion of new money in the form of central bank reserves held by commercial banks, of which around £700billion remains in circulation.

The Bank pays interest on those reserves at Bank Rate, currently 5.25 per cent. This has generated considerable income for banks as a result of the sharp increase in interest rates since 2021.

What do bank bosses say?

Last month, four big bank bosses were asked by the Treasury Committee to set out the steps they had taken to provide better savings rates for customers.

Vim Maru, CEO of Barclays UK said: ‘Our pass-through rate is regularly assessed as part of pricing governance and has increased as the bank rate has risen.

‘Our product range offers varying interest rates for different savings goals, including our Rainy Day Saver (5.12 per cent up to £5,000) which incentivises customers to build a savings habit while maintaining instant access to their money.’

Click here to resize this module

Charlie Nunn, chief executive of Lloyds Banking Group said: ‘We already offer savings products with competitive rates of up to 4.25 per cent for instant access, up to 5.10 per cent on fixed-rate accounts and up to 6.25 per cent for monthly savings accounts.

‘We also continually assess all our accounts to ensure they offer fair value, and in doing so we consider the wide range of features and benefits customers look for before choosing a particular type of account.’

Paul Thwait, group CEO of NatWest said: ‘When you take a rounded view of our products, we offer competitive rates on savings products: 6 per cent-plus on our Digital Regular Saver, our fixed term accounts are currently paying up to 4.60 per cent for one year or 4.20 per cent for 2 years [fixed rate Isa rates], and we are paying up to 3.3 per cent on our instant access savings products.’

Mike Reigner, CEO of Santander UK said: ‘Since the Bank rate started rising, we have significantly increased the amount we have paid to our savers across our range. In 2022 we paid £195million in interest to customers on our range of savings products, but in 2023 we paid £1,399 million.

‘We have done this in a way that we believe is fair, adheres to the Consumer Duty, and permits us to compete for new business through flexible pricing on our on-sale rates.’

What to do if you’re getting 2% or less on savings

Many savers continue to remain loyal to the major banks despite the low easy-access rates on offer.

The best easy-access accounts are paying 5 per cent or more, so if your savings are getting a much lower rate than this you should think about moving your money elsewhere.

> See the best-buy easy-access savings rates using This is Money’s tables

Savers can find a 5.1 per cent easy-access account with Chase Bank, while Oxbury Bank is offering 5.02 per cent on easy-access savings.

James Hyde said: ‘Customers should proactively monitor savings rates, particularly if they’re on a variable rate which providers can adjust on a very reactive basis.

‘Be prepared to switch if you feel your loyalty is not being adequately rewarded.’

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.

{kind=link}