Wall Street giant Goldman Sachs plans to layoff 4,000 ‘low performing’ staffers in January as it’s hit by the rough economic downturn.

As many as 8 percent of the bank’s workforce could be canned after the firm asked managers to draw up a list of candidates, sources told Semafor.

The insiders said the layoffs will impact every division in the bank and will happen around January, the same time bonuses are usually distributed.

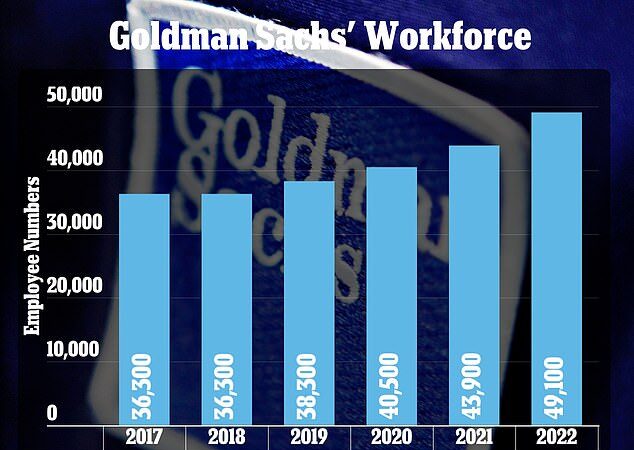

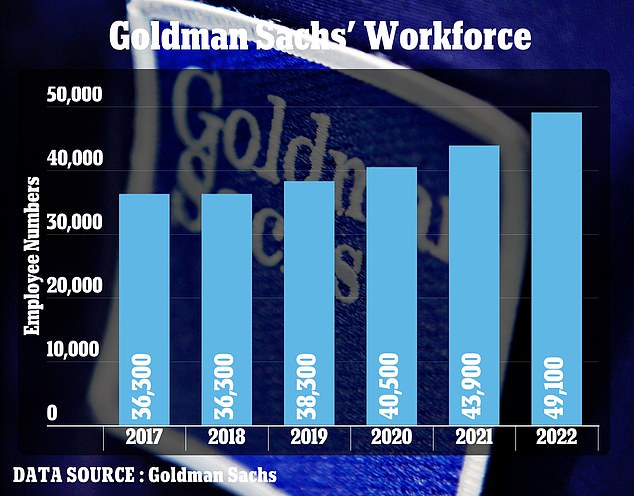

The layoffs would see the company trim its 49,1000 workforce for the first time since 2019, as its usual two to five percent annual culling was halted during the pandemic.

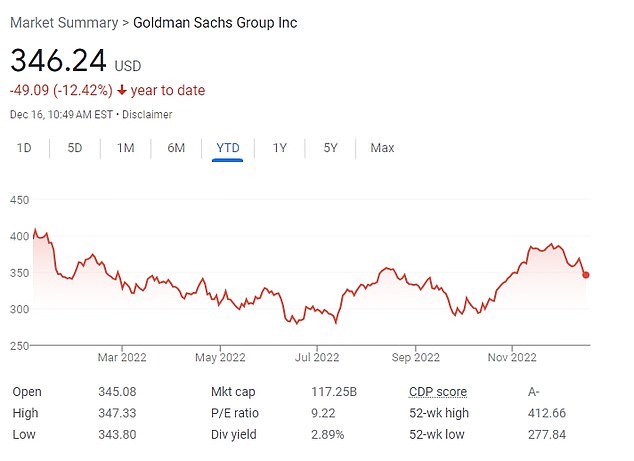

It comes amid a tumultuous year for the investment bank, which has seen its stock price drop by more than 12 percent since December 2021.

Goldman Sachs is the latest large employer looking to cut back on white collar jobs after PepsiCo announced last week that it was laying off hundreds in New York, Texas and Chicago.

Goldman Sachs plans to lay off about 4,000 people from its 49,100-strong workforce, an 8 percent cut amid a rough economic downturn

The company had enjoyed a growing workforce since CEO David Solomon (pictured) took over in 2018. The bank had halted its annual culls during the pandemic

Even if Goldman Sachs cuts it workforce by 4,000 staffers, it would still have more employees than it did in 2021.

The company has been in a sorts of hiring spree ever since CEO David Solomon took over in 2018, when Goldman Sachs retained 36,300 employee positions, the same as the previous year.

The workforce then rose to 38,300 in 2019, and 40,500 the following year. After hitting 43,900 in 2021, number swelled by more than 5,000, one of the largest spikes in the bank’s recent history.

Solomon, however, previously warned that the bank needed to cut down on costs, with the looming staff reduction among the long-planned initiatives to save money.

‘We continue to see headwinds on our expense lines, particularly in the near term,’ Solomon said while speaking at a conference last week. ‘We’ve set in motion certain expense mitigation plans, but it will take some time to realize the benefits.

‘Ultimately, we will remain nimble and we will size the firm to reflect the opportunity set.’

Goldman Sachs declined to comment on the layoffs.

Solomon has eyed measures to save money as the companies stock has fallen by more than 12 percent over the last year

The investment banks’ layoffs would come as PepsiCo, Walmart, Gap, Zillow, Ford and Stanley Black & Decker have recently cut their white collar workforce.

The industry-wide moves are leading to fears the US is racing towards a ‘white collar recession’.

In normal downturns, blue collar employees tend to lose their jobs first but now office workers are facing mass redundancies.

A report by KPMG said more than half of US chief executives are considering job cuts in the next six months.

Dave Gilbertson, VP at software maker UKG, told the Financial Times: ‘I wouldn’t at all be surprised if white-collar workers do end up being the first to be let go in a recession scenario.

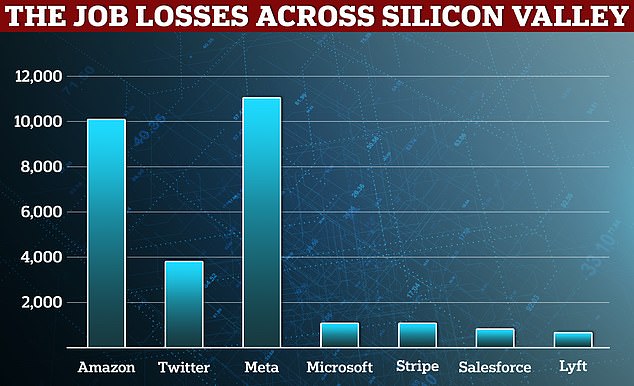

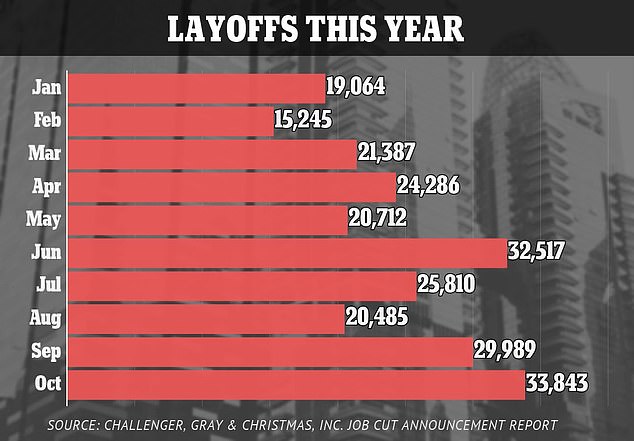

US-based tech companies have scrapped over 28,000 jobs so far this year, more than double a year earlier according to a report by Challenger, Gray & Christmas, which tracks such announcements

‘If you look at where the lay-offs have been already, it really hasn’t driven to the blue-collar markets yet. That is because there’s such a severe labor shortage in these blue-collar roles.’

Last month, Meta, which owns Facebook, Instagram and WhatsApp, revealed that it will cut 13 per cent of its workforce, while Elon Musk axed half of Twitter’s employees following his successful takeover of the social media site.

Experts have warned industries are facing a ‘triple whammy’ of a slowing economy, inflation and an end to pandemic-driven growth.

Overall, US-based tech companies have scrapped over 28,000 jobs so far this year, more than double a year earlier according to a report by Challenger, Gray & Christmas, which tracks such announcements.

In October, layoffs increased by 13 per cent – the highest jump since February 2021. US employers also eased their hiring in November, with job creation slowing the most it has since January 2021.

Just 127,000 jobs were created last month, much less than analysts expected and nearly half the 239,000 jobs created in October.

Companies that enjoyed huge growth during the pandemic, particularly those in tech and e-commerce, are starting to pare back on spending ahead of what financial chiefs fear will be trying times.

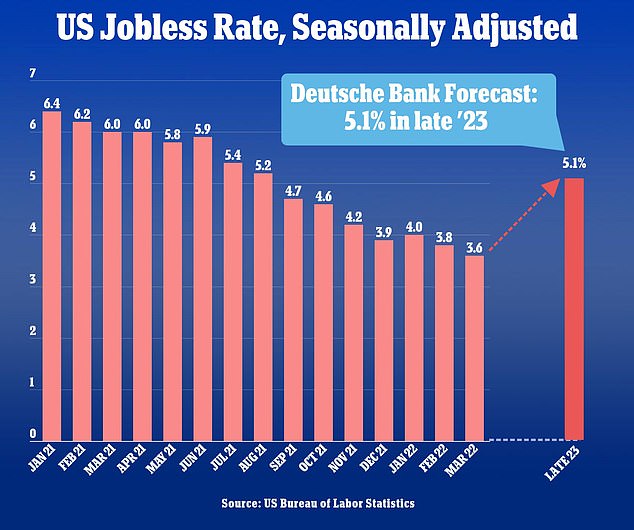

Unemployment rates are currently sitting at 3.7 percent, according to the US Department of Labor statistics.

{kind=link}