8.20am: FTSE 100 knocked by falls in the US

The FTSE 100 fell sharply in early exchanges on Friday rattled by heavy falls in US stocks amid fears over the health of the banking sector across the pond.

At 8.20am London’s lead index was down 119.53 points, or 1.5%, at 7,760.45 while the FTSE 250 slumped to 19,349.70, down 343.20, or 1.74%.

Investors wiped US$52.4bn off the market value of the four largest US banks by assets on Thursday amid a widespread sell-off of financial stocks that analysts linked to investor fears over the value of lenders’ bond portfolios.

The sell-off in JPMorgan Chase, Bank of America, Citigroup and Wells Fargo was sparked by difficulties at Silicon Valley Bank, a small, technology-focused lender.

In London, banks fell heavily. Lloyds Banking Group PLC (LSE:LLOY) fell 4.7%, HSBC Holdings PLC (LSE:HSBA) declined 4.3%, Barclays PLC (LSE:BARC) dipped 5.4% and NatWest Group PLC (LSE:NWG) slid 4.3%.

Insurance stocks also weakened. Legal & General fell 4.3% and Prudential by 3.3%.

Better news came from the Office for National Statistics which reported the UK economy grew 0.3% in January ahead of the City consensus for a rise of 0.1%.

Samuel Tombs, chief UK economist at Pantheon Macroeconomic, said the recovery in GDP in January comes as no surprise, he had forecast a 0.4% month-to-month increase, given that activity in December was depressed by several one-off factors.

He still thinks that a shallow recession is the most likely outcome. “Either way, the economy clearly is sluggish, and more importantly for the MPC, labour availability is improving and the rate of price increases is slowing.”

“The jump in markets’ rate expectations over the last month, therefore, looks detached from both the economic data and Governor Bailey’s recent comments,” he felt.

ING Economics said the increases was faster than expected, though underlying volatility in the data means that GDP is effectively flatlining.

“Lower gas prices mean that any recession is likely to be very modest now – and may technically be avoided altogether,” the suggested.

“Overall though, today’s figures raise the chances that UK growth could come in flat or only slightly negative in the first quarter overall,” ING said.

FirstGroup PLC (LSE:FGP) was little changed in early exchanges despite raising guidance for profit for the current financial year. The bus and rail operator said bus volumes had picked up in part reflecting the £2 fare cap introduced by the government and an improvement in the supply of bus drivers.

Housebuilder Berkeley Group PLC said trading was in line with the levels outlined back in December, when sales from the end of September were around 25% lower than the first five months of its financial year, which ends in April. It reaffirmed targets of pretax profit of £600mln with at least US$1.05bn in aggregate to follow over the next two years. Cash due on exchanged forward sales is anticipated to be above £2.0bn at year-end, down slightly from £2.17bn a year before. Shares fell 0.4%.

7.34am: UK economy grows in January

The UK economy grew in January and there were no revisions to December’s figures meaning the recession headlines can thankfully be put away for a few months at least.

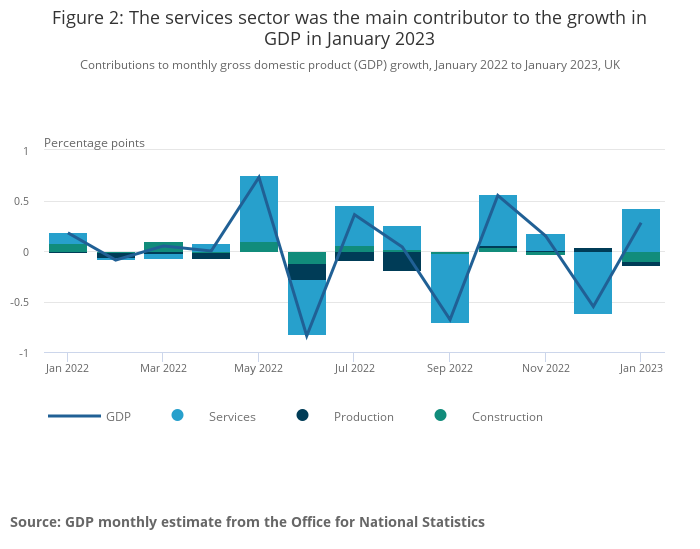

Monthly real gross domestic product (GDP) is estimated to have grown by 0.3% in January 2023, after falling by 0.5% in December 2022, according to figures from the Office for National Statistics (ONS). Analysts had expected a rise of 0.1%.

Looking at the broader picture, GDP was flat in the three months to January 2023.

.png)

The services sector grew by 0.5% in January, after falling by 0.8% in December, with the largest contributions to growth in January coming from education, transport and storage, human health activities, and arts, entertainment and recreation activities, all of which have rebounded after falls in December.

Output in consumer-facing services grew by 0.3% in January; this follows a fall of 1.2% in December.

Production output fell by 0.3% in January, following growth of 0.3% in December while the construction sector fell by 1.7% in January after being flat in December. There are no revisions to previously published data in this release.

7.28am: FirstGroup sees higher profits

FirstGroup PLC (LSE:FGP) said on Friday it anticipates profits for the 2023 financial year to be ahead of previous expectations following strong trading in its bus and rail operations.

In a statement the FTSE 250 listed firm said an improved performance at First Bus was driven by higher passenger volumes in second half of the financial year and driver resource pressures easing in certain locations.

Bus passenger volumes have increased to 83% of 2020 equivalent levels, with commercial and concessionary volumes at 87% and 75% respectively. The increase in demand has partially resulted from the £2 bus fare cap scheme introduced in England in January 2023, the company said.

First Rail open access operations benefited from stronger than anticipated passenger demand over the winter months, the company said.

As a result FirstGroup expects 2023 adjusted operating profit and adjusted attributable profit will be ahead of previous expectations. Company compiled consensus estimates adjusted operating profit and adjusted attributable profit are currently £137.4mln and £58.6mln respectively.

Expectations for the financial year 2024 remain unchanged.

FirstGroup said the final earnout consideration from the sale of First Transit by EQT Infrastructure is anticipated later in 2023.

7.00am: Bank rout in the US to weigh on London

The FTSE 100 is expected to nurse heavy losses at the open after US stocks tumbled hit by big falls in banking share prices.

Spread betting companies are calling London’s lead index down by around 116 points.

The Dow closed Thursday down 542 points, 1.7%, at 32,256, the Nasdaq Composite dropped 238 points, 2.1%, to 11,338 and the S&P 500 declined 74 points, 1.8%, to 3,918. The small-cap Russell 2000 index lost 51 points, 2.7%, to 1,828.

The S&P financial sector fell about 4%, its worst day since June 2020. Shares of SVB Financial slumped 61% after the firm announced a US$1.75 billion stock sale, and Silvergate stock tumbled 30% on news that it’s shutting down operations. Two bigger bellwethers, Bank of America and Wells Fargo, saw shares drop more than 6% each.

Ipek Ozkardeskaya senior analyst at Swissquote Bank noted “a severe rout in banking stocks spoiled what could’ve been a calm session on Thursday.“

“The collapse of Silvergate Capital and a severe rout in SVB stock plunged the banking sector into darkness yesterday. While Silvergate Capital’s fall was mainly crypto-related and didn’t spur worries for the rest of the banking sector, SVB’s plunge fueled fears that the rest of the banks could also experience similar issues.”

Asian markets were also weaker.The Nikkei 225 index in Tokyo closed down 1.7%, after the Bank of Japan left its ultra-easy monetary policy unchanged in Governor Haruhiko Kuroda’s last policy-setting meeting. In China, the Shanghai Composite was down 1.1%, while the Hang Seng index in Hong Kong was down 2.5%.

The early focus in London will be the GDP figure for January to see how the UK economy fared at the start of 2023. Panmure Gordon expects growth of 0.2% month-on-month. A trading statement from housebuilder Berkeley is also in the calendar.

Later today US non-farm payrolls figures take centre stage.

{kind=link}