Exclusive: Open Banking’s strategic working group finds “limited agreement” on the future UK direction of open banking

The draft report, seen by AltFi, details “very stark differences” in industry views on consumer protections, the levels of fraud caused by open banking payments, API reliability and much more.

Image source: AltFi/Shutterstock.

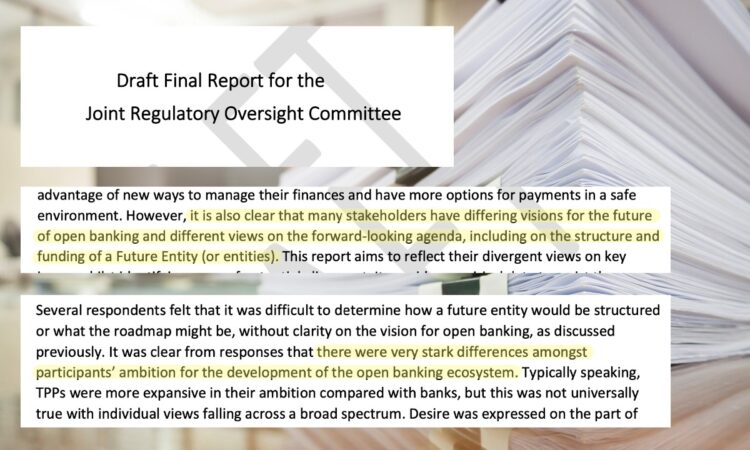

A crucial report that will help determine the future direction of open banking in the UK has found “limited agreement” among key financial industry players on what that open banking future should look like, AltFi can exclusively reveal.

This confidential 186-page draft final report, seen by AltFi, was created by open banking’s Strategic Working Group (SWG) at the request of the Financial Conduct Authority, Payment Systems Regulator, Competition and Markets Authority, and HM Treasury.

Its findings are intended to guide the decisions of the Joint Regulatory Oversight Committee (JROC), which is co-chaired by the above institutions.

However, after a vast programme of industry engagement spanning several months with 189 written submissions and over 21 hours of meetings, the SWG’s report found “very stark differences” exist between the retail banks, Third Party Providers (TPPs) and fintechs which together form the UK’s open banking ecosystem.

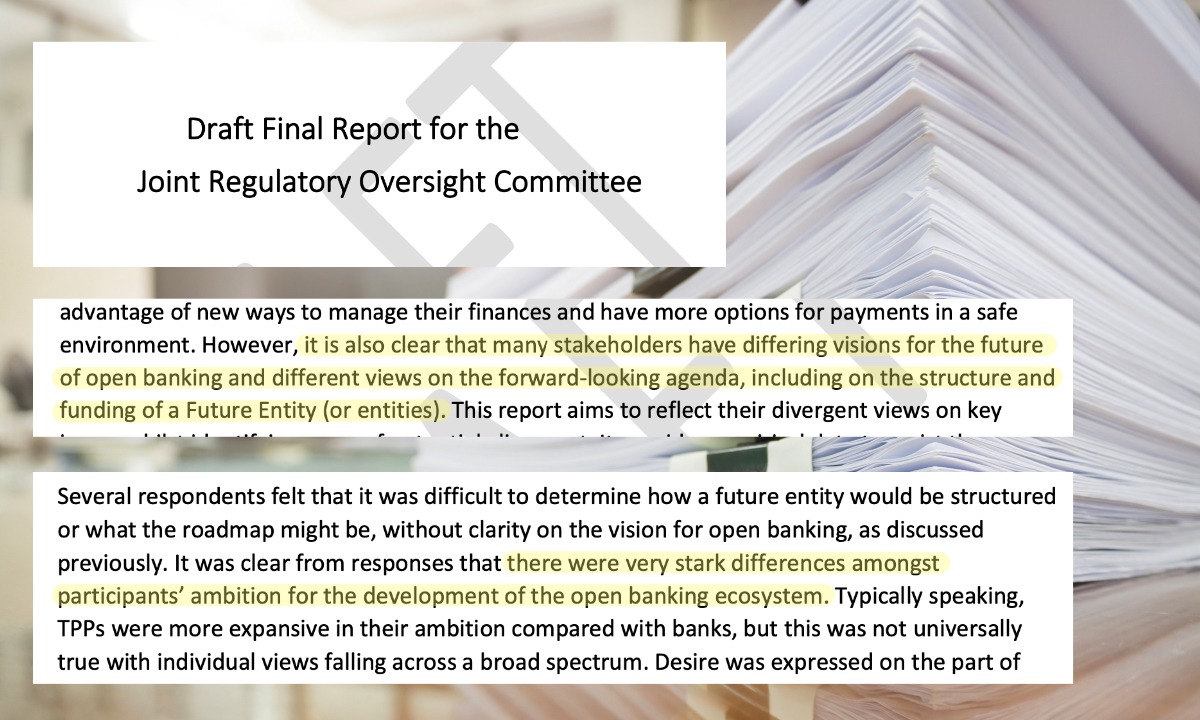

The report’s executive summary explains how the SWG had found “differing visions for the future of open banking and different views on the forward-looking agenda, including on the structure and funding of a Future Entity (or entities).”

Differing Visions

Across the draft document, feedback from the industry was split between Third Party Providers (TPPs) who were “more expansive in their ambition” for how open banking should be developed, including beyond current accounts and into other financial products, versus the retail banks which remained more conservative.

“This was not universal, however, with one bank in the ecosystem strategy sprint discussion meeting promoting a very expansive vision for open banking data sharing,” the SWG wrote in its draft report.

Looking towards the future, TPPs called for a future direction that “dovetailed with the Government’s broader agenda regarding Smart Data and would support maintaining the UK’s international standing as a leader in open banking and a global hub for Fintech.”

Large retail banks meanwhile argued that “further evolution of the open banking ecosystem needs to be underpinned by reasonable commercial returns and for the market to determine the development path.”

These commercial motivations mean “there is limited incentive for banks to invest further funds to achieve above the regulatory minimum” while, on the other hand, the SWG found “some TPPs would question the extent to which parity has been achieved and many more wanted further improvement in performance to support wider adoption of open banking.”

The SWG report also identifies five main points for improvement (referred to in the report as gaps) “between the current state and what many respondents suggested was a more optimal future state for the UK open banking ecosystem”.

These five points include improvements around the reliability of open banking’s APIs, the level of fraud attributed to open banking payments, if and how a customer protection regime should be implemented, how existing open banking standards should be improved and how open banking should be extended.

However, as the SWG found such “limited consensus” on what the future state of open banking entails, these five points and even the perception of them as points for improvement “are often contested, with stakeholders harbouring different views on their relevance or extent.”

Figuring Out The ‘Future Entity’

With regards to the Open Banking Implementation Entity (OBIE) and a proposed ‘future entity’ that will oversee open banking going forwards, the SWG found slightly more agreement.

A “strong preference” was expressed by many stakeholders that the future entity should be a central standard-setting body, with a remit that extends beyond just open banking as it exists today “supporting the development of long-term smart data capabilities and digital financial infrastructure for the UK economy”.

Ultimately the SWG recommended a “possible model” for the future entity which limits its role to a number of core services (standards development and monitoring), with “non-core activities” like promoting open banking and supporting implementation to be spun off either to another entity (or entities) or achieved via the market.

The specifics of how this future entity is funded are far less clear, however, with the SWG finding “no consensus on an optimal approach” and with suggestions ranging from membership fees to regulatory levies and pay per usage.

AltFi understands that while the findings of this draft report dated 21 December 2022 are near-final, there may still be changes in the final version submitted to the JROC and due to be published on the OBIE’s website in the coming weeks.

“A lot now rests on JROC, and we are looking for clarity and a resolution to these issues so all participants in the ecosystem can plan with confidence,” one director of a major open backing provider told AltFi, who asked not to be named as the contents of the SWG’s report are still confidential.

“Certainty would be good for jobs and investment in UK fintech.”

AltFi has reached out to the Financial Conduct Authority and the Payment Systems Regulator as co-chairs of the JROC for comment. The OBIE, which serves as the secretariat of the SWG, declined to comment.

Analysis – Another Kick Of The Can Down The Road

If anyone was hoping the SWG report would provide clarity on the future direction of open banking in the UK… I’m afraid there’s relatively little to be found here.

The splits and disagreements between banks and TPPs are already well-documented and widely known, so the SWG report now leaves JROC in the unenviable position of having to weigh in on these fundamental differences.

There are big questions still to be answered around what the future entity looks like, if a new funding model will work, and how open banking will expand into “open finance”, the answers to which are all intrinsically linked to whatever the UK’s future vision for open banking will be.

Indeed it’s only by agreeing on a strong, ambitious vision of the future of open banking that JROC can even begin making those decisions.

Luckily, the political will for such a vision appears to be growing, as the government’s City Minister, Andrew Griffith MP, wrote in City AM last week:

“My task now is not just to lock in this progress – but to build on it to ensure the benefits of open banking technology and broader innovation are felt by as many people and businesses in the UK as possible.”

Yes, the SWG’s report is yet another kick of the open banking can down the road, and many calling for “urgent clarity” will feel further frustration that we still don’t have answers.

But the end of the road is now in sight, and sooner rather than later JROC will have to set out its vision.

Sign up for our newsletters

{kind=link}