Eurozone banks may suffer billions of euros in lost profits and be forced to deal with tighter liquidity from a potential increase in the reserves they are required to hold at the European Central Bank.

The ECB is reviewing banks’ minimum reserve requirements (MRR) as part of a wider review of its operational framework. The MRR is currently set at 1% of a bank’s overnight deposits, deposits with an agreed maturity or notice period of up to two years, debt securities issued with maturity of up to two years and money market papers. Historically that rate has been set at 2%.

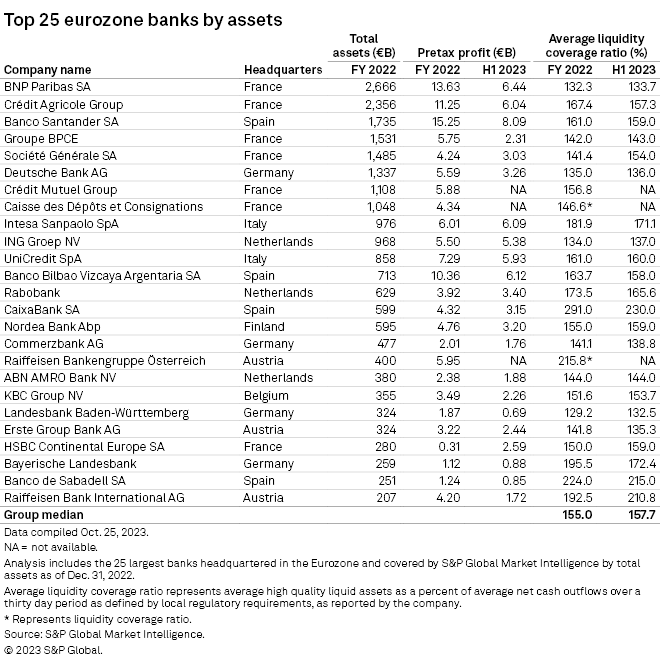

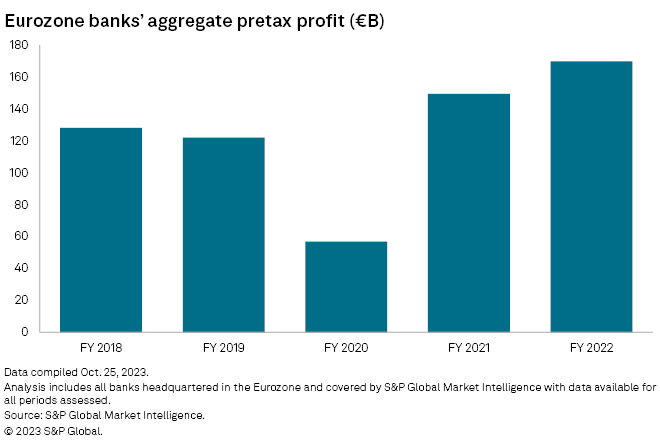

A one-percentage-point increase in the MRR could mean an immediate gross impact of 3.3% on the aggregate pretax profit of eurozone banks, according to analysts at S&P Global Ratings. The aggregate pretax profit of eurozone banks hit €170 billion in 2022, according to S&P Global Market Intelligence data. By Ratings’ estimates, that profit could drop by about €5.61 billion in the event of an increase.

The ECB stopped remunerating banks for their MRR in September; a higher MRR would drag on banks’ net interest income (NII), ING analyst Suvi Platerink Kosonen said in a report. A 1% increase in the MRR would dent banks’ NII by 1.7%, based on full-year 2022 figures, Ratings analysts said.

The ECB did not discuss the MRR during its Oct. 26 monetary policy meeting. ING analysts expect the issue to be addressed once the central bank presents the outcome of its operational framework review, likely in spring 2024.

The ECB declined to comment and only pointed to previously published comments by officials on the matter.

Liquidity woes

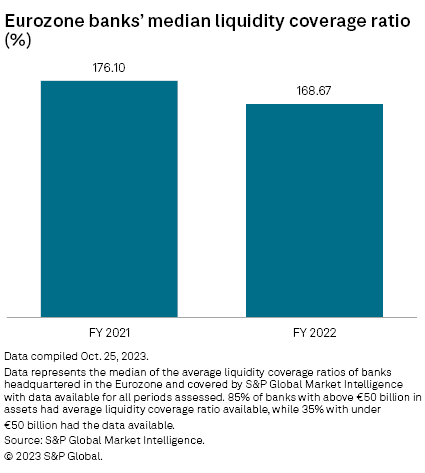

A higher MRR would reduce the amount of excess liquidity held by lenders at a time when buffers are already falling, and recent bank failures in the US and at Credit Suisse Group AG have brought the issue into focus. The median liquidity coverage ratio (LCR) of eurozone banks decreased to 168.67% at the end of 2022 from 176.10% a year before, Market Intelligence data shows.

Banks’ aggregate LCR, which is a measure of the level of reserves a bank must hold to fund outflows for 30 days, would decline by 4.7% in the event of a one-percentage-point MRR increase, according to Ratings.

While banks broadly have sufficient liquidity to handle an increase to the MRR, it could result in tighter lending conditions and weigh on investor sentiment around the sector, according to Ratings. Furthermore, when taken alongside upcoming repayments of targeted longer-term refinancing operations (TLTRO), a higher MRR could “meaningfully deplete” some banks’ liquidity buffers, Ratings said.

‘Craziest’ proposal

Some members of the ECB’s rate-setting governing council supported increasing the MRR back to its pre-2011 level of 2%, according to minutes of their July meeting. Joachim Nagel, the president of Germany’s central bank, has signaled backing for an increase. His counterpart in Austria, Robert Holzmann, suggested a steeper increase to as much as 10%.

The head of the Association of German Banks, Heiner Herkenhoff, has criticized the idea of raising the MRR, saying it would be tantamount to a tax. Commerzbank AG CFO Bettina Orlopp is also against the proposition, calling Holzmann’s suggestion “the craziest proposal.”

German banks would feel the highest absolute impact on profitability from a higher MRR, followed by French, Italian and Spanish banks, ING’s Platerink Kosonen warned. In relative terms given the size of their banking systems, lenders in the Baltics, Cyprus and Slovenia could be hardest hit, she said.