LONDON, Jan 26 (Reuters Breakingviews) – European banks undeniably earned their reputations as financial ne’er-do-wells. Their low stock-market valuations were hard-won through years of risky lending, trading slip-ups and excessive financial engineering. But investors might be missing how much lenders like Deutsche Bank (DBKGn.DE) and others have, over the years, mended their ways.

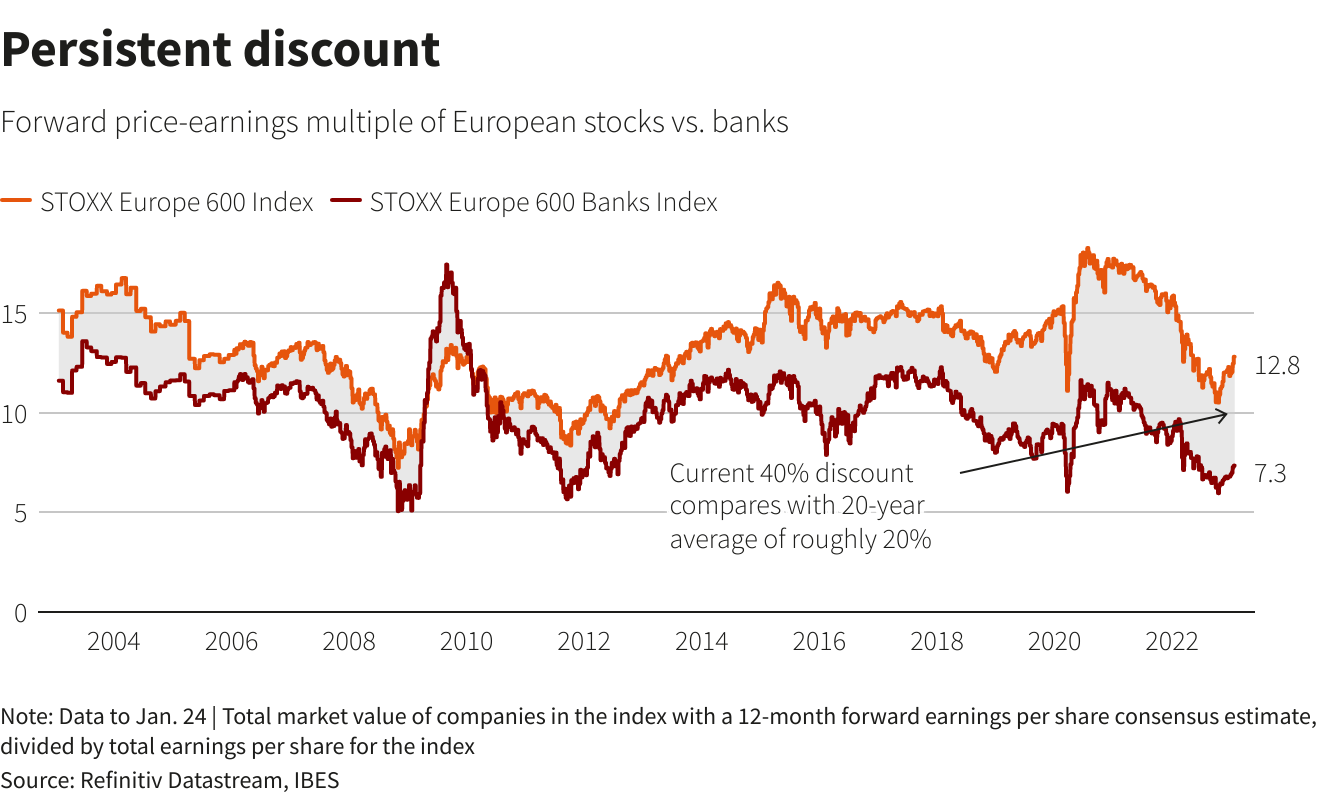

Major euro zone and UK banks are trading at a 40% discount to the region’s wider benchmark index, using price to forward earnings multiples tracked by Refinitiv. In one sense that’s unsurprising: history says it’s a bad idea to own lenders in an economic downturn such as the one that’s coming. Banks were at the epicentre of the 2008 crash, and many needed a bailout. The subsequent euro zone crisis in 2012 prompted a wave of bad debt that weighed down earnings.

With growth slowing, and chief EU bank watchdog Andrea Enria warning of rising customer defaults, investors seem to be assuming that the same will happen again. But the banks arguably deserve more credit for their rehabilitation – which might be thought of as a kind of six-step recovery programme.

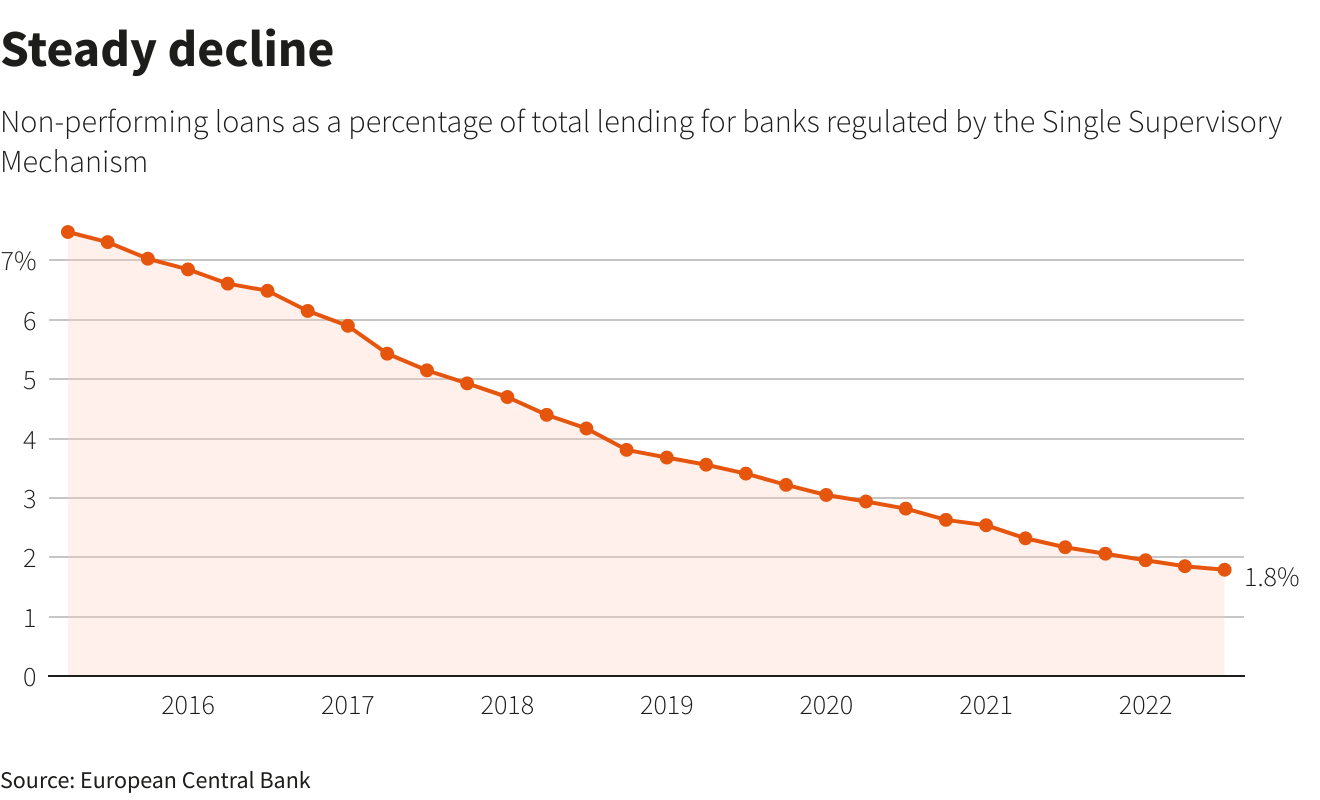

First, Europe’s banks have purged many bad loans. A decade ago, about half of banks’ so-called credit losses actually came from deterioration in lending that had previously gone bad but still sat on the balance sheet, according to Bank of America analysts. More recently, though, euro zone lenders have been facing up to their past sins, and offloading non-performing loans. Credit goes to regulators, who egged them on, and governments, who often guaranteed the sales. That cleanup will now help chief executives like UniCredit’s (CRDI.MI) Andrea Orcel.

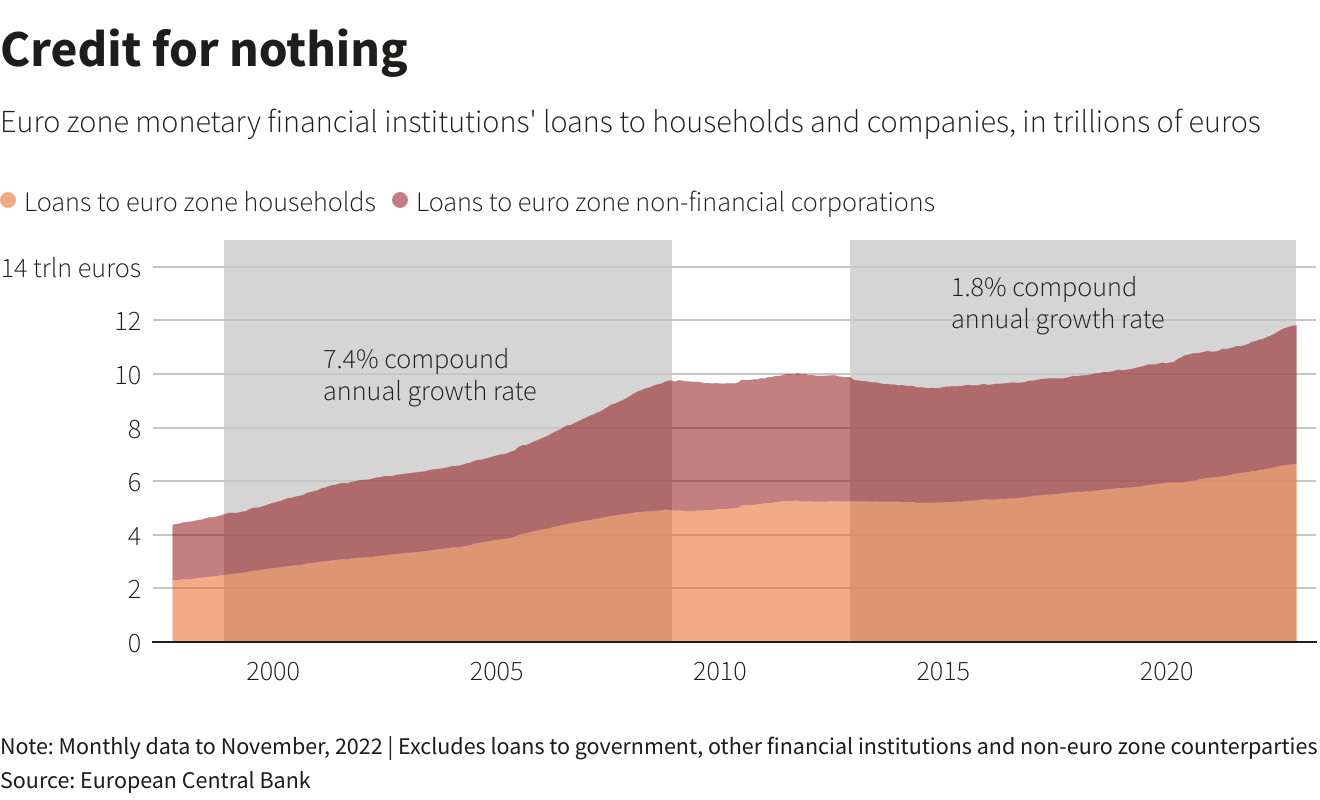

Second, they’re being more careful in making new loans. There’s no evidence of a bank lending splurge, despite years of rock-bottom interest rates. Between November 2012 and November 2022, euro zone banks’ total lending to households and companies grew at an annual clip of under 2%, a fraction of its pre-2008 pace. Meanwhile Britain’s biggest bank back then, Royal Bank of Scotland – now called NatWest (NWG.L) – has a balance sheet just one-third of its former size.

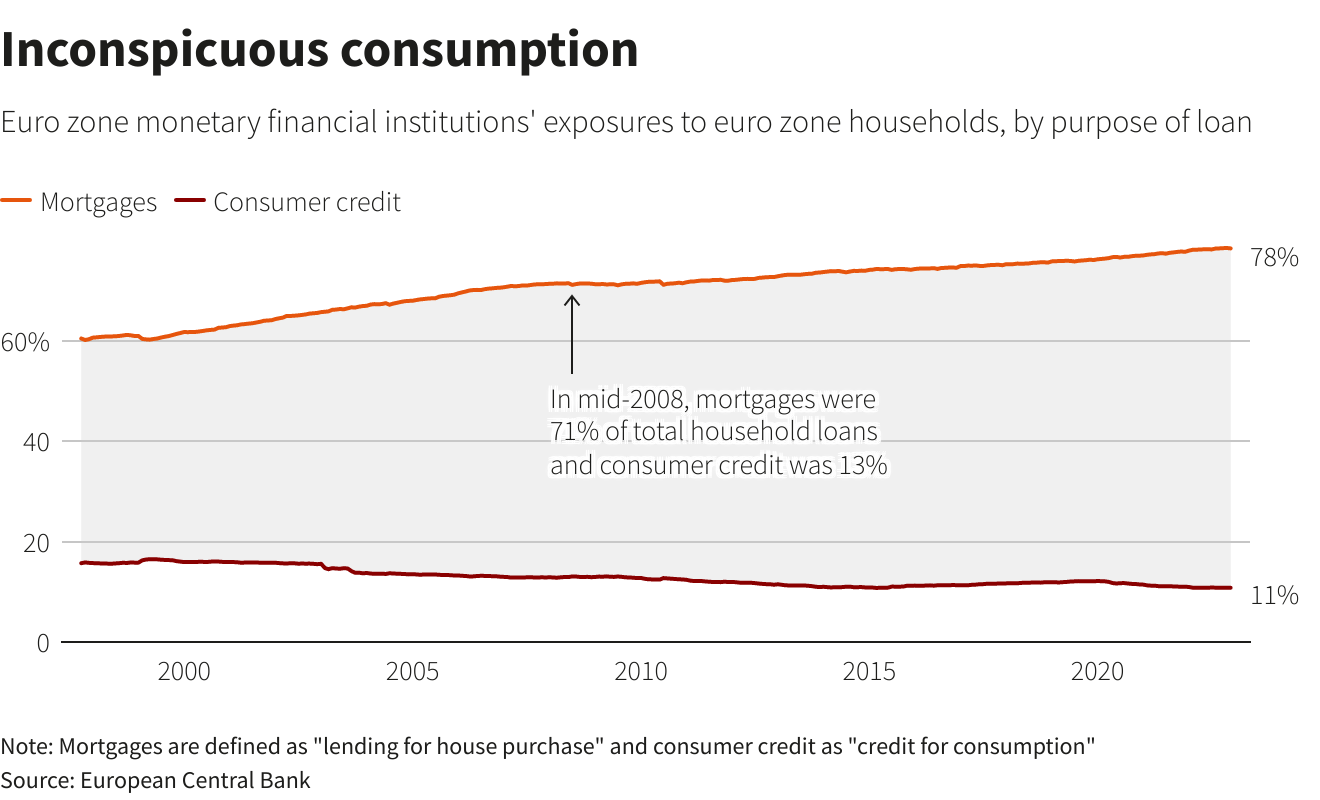

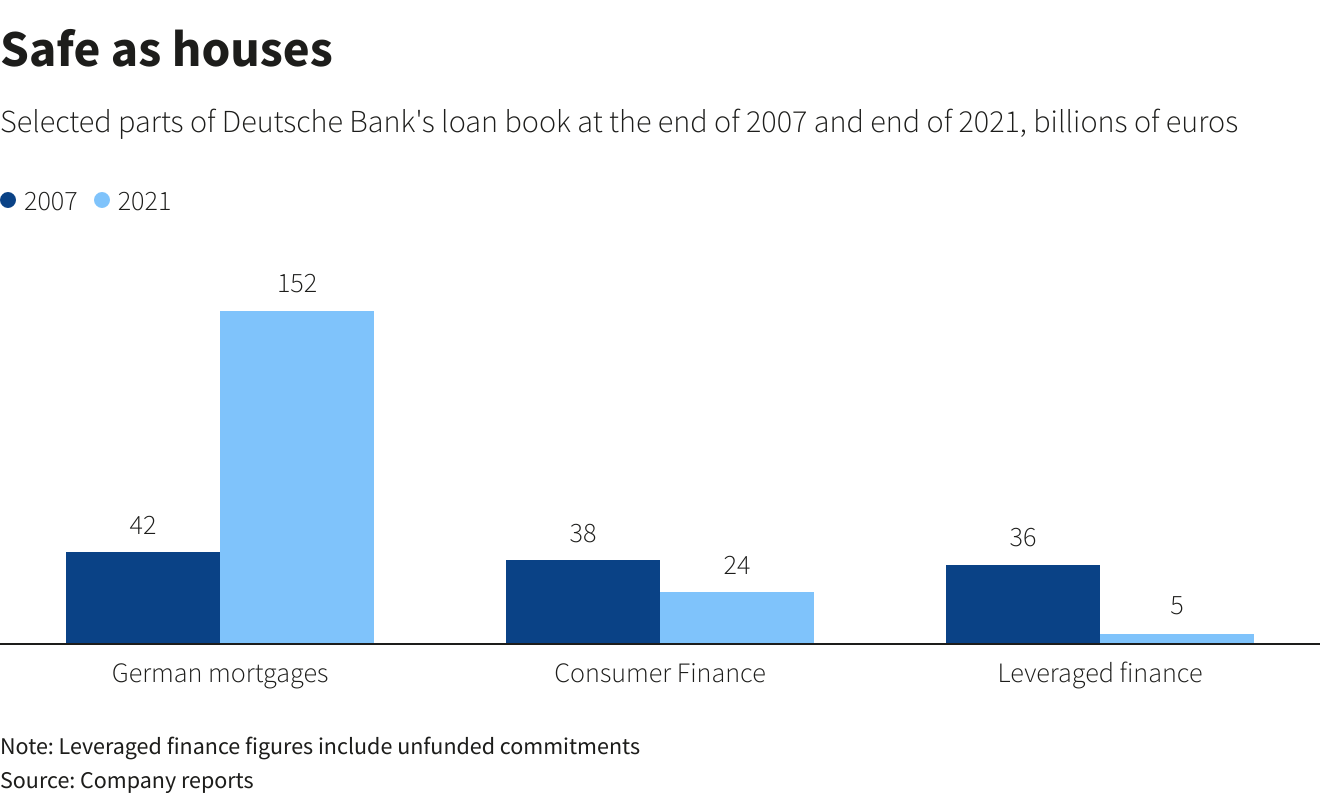

When they do lend, they’re now taking less risk. Start with retail lending. In the euro zone, the sector’s exposure to relatively risky consumer finance has ticked down as a percentage of the total, while the share of mortgages has gone up. That’s helpful for banks because borrowers are much less likely to default on a home loan, which could result in the customer losing their house, than on unsecured debt like credit cards. That contrasts with the United States, where consumer finance has soared.

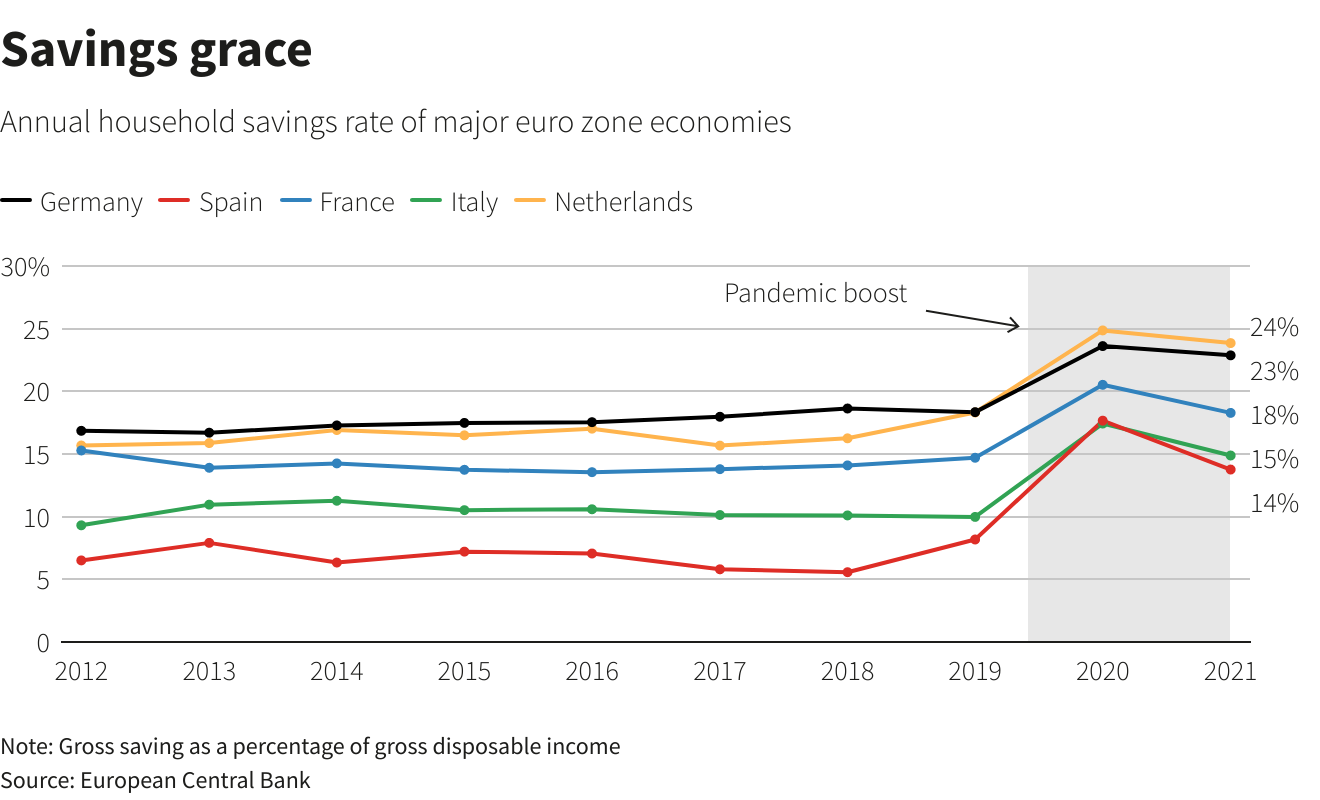

Customers, meanwhile, are in better shape. Lenders across the region have been phasing out variable-rate mortgages in favour of fixed-price deals, helping to insulate borrowers from the immediate cost of higher rates. A combination of pandemic lockdowns and government support programmes also saw the savings rate surge in most major economies. That means households have a much larger cash buffer to help them through a slowdown.

While companies remain risky, it’s now a problem shared. Banks have an issue when small and medium-sized businesses hit hard times, since they’re more likely to fail than larger borrowers. But because politicians underwrote so much lending during the pandemic, much of the risk now sits with the state. Almost one-tenth of loans to non-financial corporates at BNP Paribas (BNPP.PA) and Société Générale (SOGN.PA) carry a government guarantee, according to Jefferies. The same analysts reckon that Intesa Sanpaolo (ISP.MI), Banco Santander (SAN.MC), BBVA (BBVA.MC), CaixaBank (CABK.MC) and UniCredit have taxpayer backstops for between 10% and 22% of their domestic corporate loans.

Lastly, banks have conquered some of their historically diciest habits. In 2008, losses mounted from big trading and investment banking bets on assets like leveraged-buyout debt and mortgage bonds. There are still pockets of risk in those areas: BNP Paribas, for example, backed the buyouts of social network Twitter and UK supermarket Wm Morrison, and could be stuck holding some of that debt.

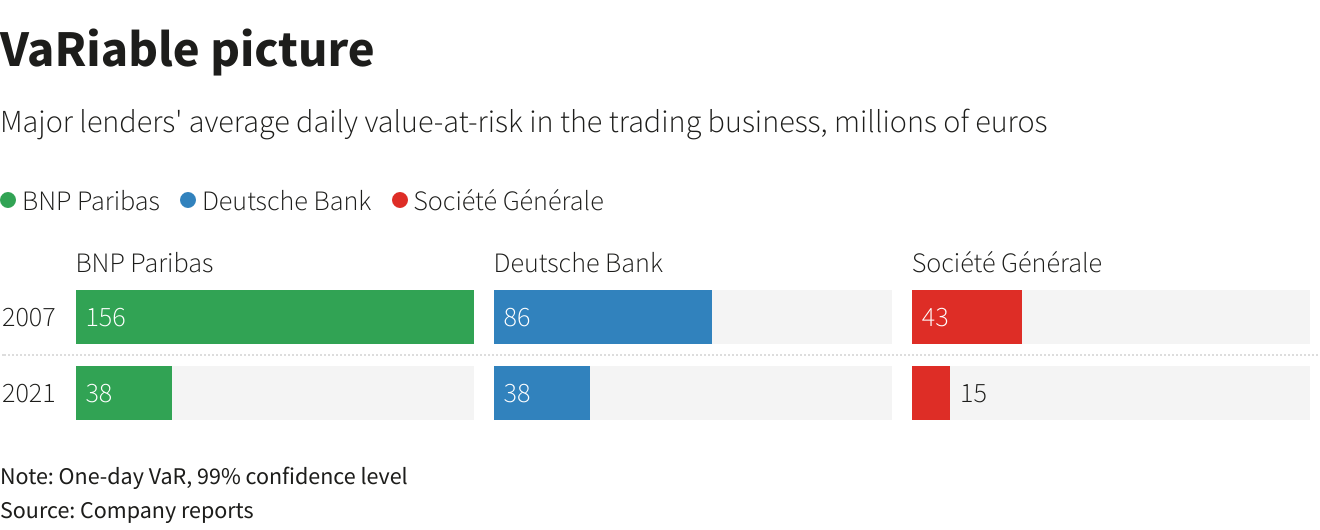

But others have retrenched. In 2007, euro zone and UK banks accounted for nine of the top 20 slots in global leveraged-finance underwriting league tables, according to Refinitiv, while last year just three of them figured in that list. Former basket case Deutsche Bank has massively shrunk its exposure to risky credit. European investment banks have also cut down the proportion of their balance sheets available to traders, which shows up through the amount the banks could potentially lose in a day, known as “value at risk”. That reduces the risk of a 2008-style mortgage blowup.

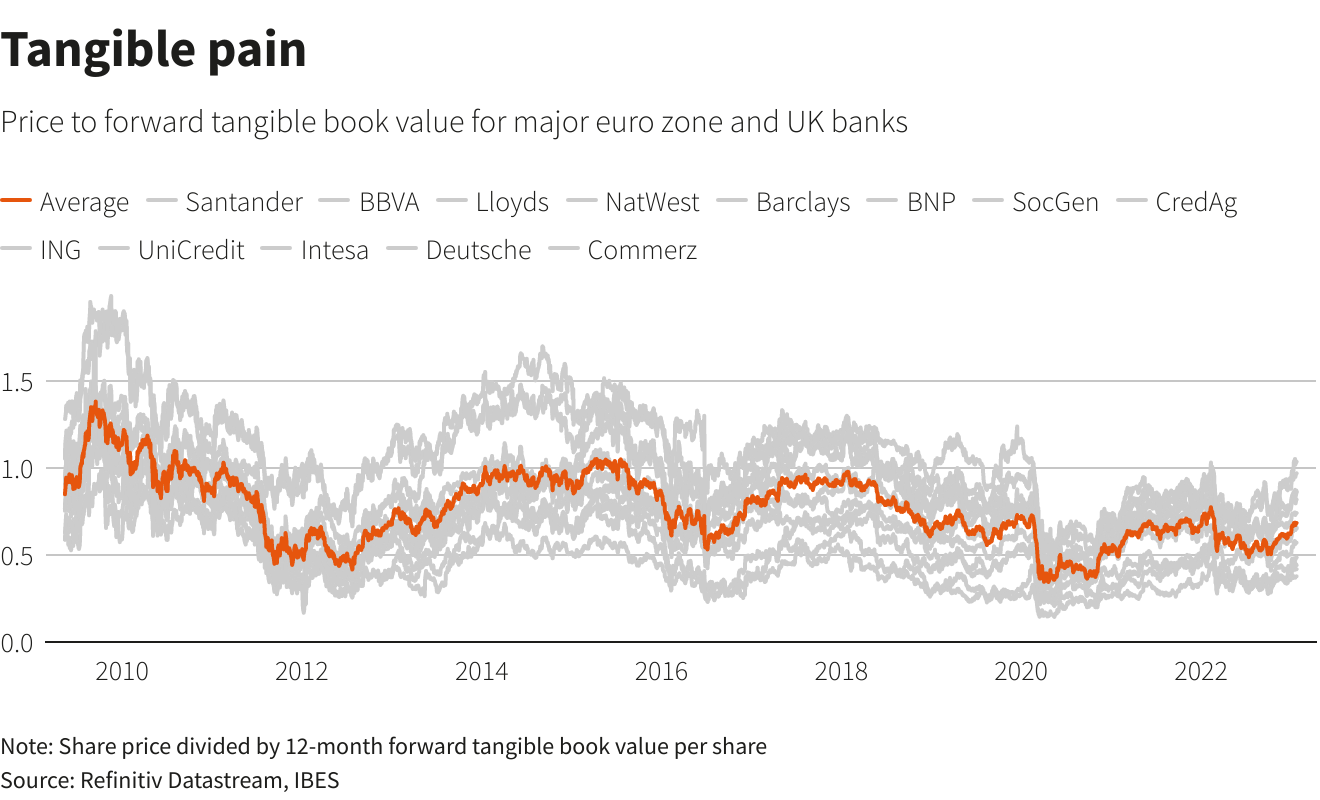

Helped by this cleanup, and thanks also to higher revenue from rising rates, analysts reckon the big euro zone and UK banks will churn out a healthy profit over the coming year, equivalent to over 10% of tangible equity. That’s higher than at any point over the last decade. And since investors typically demand a minimum 10% return for holding bank shares, it ought to be enough to justify valuations in line with the listed lenders’ book value.

That’s still not happening. The region’s banks trade at just two-thirds of their tangible book value, even though they’ve lately outperformed the wider European benchmark. It may be that investors want to see that lenders’ virtuous new habits will stick, and that they can make it through a potential recession without too many scrapes. But given the banks’ efforts at good behaviour, their recidivist-style valuations look unjust.

Follow @liamwardproud on Twitter

CONTEXT NEWS

Earnings season for major European banks starts with UniCredit on Jan. 30, followed by Banco Bilbao Vizcaya Argentaria on Feb. 1.

Deutsche Bank, ING and Banco Santander report their full-year and quarterly earnings on Feb. 2.

Editing by Neil Unmack, John Foley and Oliver Taslic

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.

{kind=link}