Internet users

For the ICT survey of households and individuals, an internet user is defined as a person aged 16–74 who makes use of the internet in whatever way: whether at home, at work, or anywhere else; whether for private or professional purposes; regardless of the device (desktop computer, laptop, netbook or tablet, smartphone, games console or e-book reader) or type of connection being used.

Across the EU, some 84.0 % of people made use of the internet on a daily basis

In 2022, more than four fifths (84.0 %) of the EU’s population aged 16–74 reported having used the internet on a daily basis during the three months preceding the survey. This figure was 3.6 percentage points higher than a year before and 27.7 points higher than a decade before (note there is a break in series). Internet use was particularly high among younger generations: some 96.4 % of young people in the EU – defined here as those aged 16–29 – made use of the internet on a daily basis in 2022. By contrast, the share for older people –defined here as those aged 65–74 – was considerably lower, at 55.0 %.

With a growing share of day-to-day tasks being carried out online, the ability to use modern technologies becomes increasingly important to ensure everyone can participate in the digital society. As noted above, one such ‘digital divide’ is in terms of age, with some older generations not having the necessary digital skills or interest to take full advantage of the expanding array of internet services or internet-enabled devices that are on offer. In a similar vein, people aged 16–74 living in rural areas of the EU were less likely to make use of the internet on a daily basis (78.4 % during the three months preceding the survey in 2022) than those living in towns and suburbs (84.1 %) or in cities (87.4 %). Many rural area have a higher proportion of older people which partly explains this ‘digital divide’ by degree of urbanisation. However, a lack of infrastructure investment may also be a factor, as people living in rural areas may be less likely to use the internet if they are hampered by slower internet speeds, less technological choice, or higher prices. This divide is likely to be further challenged in the coming years, as 5G internet services (the fifth generation of cellular network technology) continue to be rolled out.

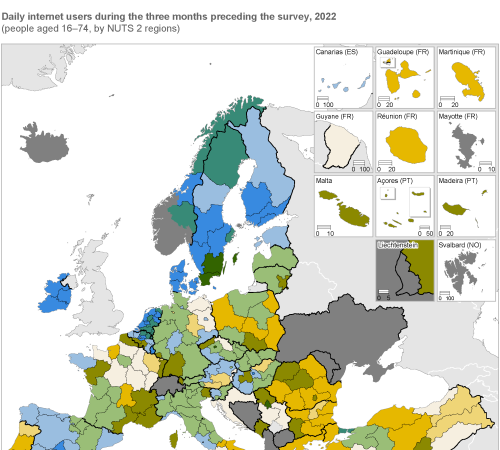

In every region of the EU, more than two thirds of the population made use of the internet on a daily basis

Map 1 shows the regional distribution of daily internet use across NUTS level 2 regions; note that data for Germany, Greece, Poland and Türkiye relate to level 1 regions. There were clear disparities between EU regions in terms of daily use of the internet along broad geographical lines: northern and western regions generally recorded higher levels of use than southern or eastern regions.

In 2022, the highest share of people aged 16–74 making daily use of the internet was recorded in the Swedish region of Sydsverige (96.7 %). There were six other regions within the EU where more than 95.0 % of people used the internet on a daily basis:

- the capital regions of the three Nordic Member States – Stockholm, Helsinki-Uusimaa, and Hovedstaden;

- Småland med öarna (which is also in Sweden), Zeeland (in the Netherlands) and Eastern and Midland (in Ireland).

There were only two NUTS level 2 regions within the EU where fewer than 7 out of 10 people aged 16–74 made daily use of the internet in 2022: the Bulgarian region of Yuzhen tsentralen (68.5 %) and the southern Italian region of Calabria (68.0 %).

_RYB2023.png)

(people aged 16–74, by NUTS 2 regions)

Source: Eurostat (isoc_r_iuse_i) and (isoc_ci_ifp_fu)

Figure 1 provides information on the overall change in the share of daily internet users between 2019 and 2022:

- there were 65 regions (out of 196 for which data are available) in the EU where the share of daily internet users rose by more than 10.0 percentage points during the period under consideration;

- by contrast, there were 18 regions where the share of daily internet users fell.

In the French outermost region of La Réunion, the proportion of daily internet users rose 25.0 percentage points between 2019 and 2022. The highest increases were otherwise observed for several regions located across Romania and Bulgaria, as well as Alentejo in Portugal. At the other end of the range, among the 18 regions that recorded a fall, it was already common to observe relatively high shares of daily internet users in 2019; most of these regions saw their share of daily internet users decline by a modest amount. However, there were a number of regions – principally across Germany, but also in Sweden, the Netherlands and Belgium – where a more substantial fall was observed. The largest declines were observed in Bremen and in Sachsen-Anhalt (both Germany), as well as Mellersta Norrland (Sweden).

_RYB2023.png)

(percentage points difference compared with 2019, people aged 16–74, by NUTS 2 regions)

Source: Eurostat (isoc_r_iuse_i) and (isoc_ci_ifp_fu)

Internet activities

With the prolific use in modern society of mobile devices such as smartphones and tablets, the frequency with which people use the internet has grown exponentially. Although it was initially used as a means to exchange information (often in a working environment), the range of activities conducted over the internet has rapidly changed. For example, it is no more than 15 years since commercially successful app stores and streaming services were launched.

Participation in social networks

Today, one of the most popular activities on the internet is participation in social networks, for example, using Facebook, Instagram, Snapchat, TikTok or Twitter. As with many internet activities, the propensity to make use of such services is closely linked to age. A much higher proportion of younger people use social networks on a regular basis, and young people are also more likely to be early adopters of new apps/services as they seek alternative ways of exchanging text, sound, images, video and other information. Looking generally across the EU population aged 16–74, it was more common for people living in cities (rather than those living in rural areas) to participate in social networks, while people with a high level of educational attainment were more likely to participate in social networks than those with lower levels of attainment.

Close to three fifths of the EU’s population participated in social networks

In 2022, close to three fifths (58.2 %) of the EU’s population aged 16–74 participated in social networks during the three months preceding the survey. At 83.6 %, the participation rate for younger people (aged 16–29) was more than three times as high as the corresponding rate for older people (aged 65–74; 24.2 %). In recent years, there has been little change in the proportion of younger people who participate in social networks; their share was already higher than 80.0 % in 2014 (note there is a break in series; it is also important to bear in mind that the statistics presented here do not provide a measure of the average time spent by each individual interacting with social networks). By contrast, there was relatively rapid growth – from an initially low level – in the proportion of older people participating in social networks: their share more than trebled from 7.2 % in 2013 to 24.2 % by 2022 (note there is a break in series).

In all five Danish regions, more than four fifths of the population participated in social networks

There were eight NUTS level 2 regions across the EU where more than four fifths of the population aged 16–74 participated in social networks during the three months preceding the 2022 survey; note again that data for Germany, Greece and Poland relate to level 1 regions, as do the data for Türkiye. These eight regions were concentrated in Denmark (all five regions) and also included the capital regions of Budapest (Hungary) and Helsinki-Uusimaa (Finland), as well as Drenthe in the Netherlands. The highest share was recorded in Hovedstaden – the Danish capital region – at 86.3 %.

Although many would argue that social networks are ubiquitous, there were 42 regions within the EU where less than half of the population participated in social networks. Among these, there were seven – exclusively located in France (four regions) and Germany (three regions; NUTS level 1) – that had shares of less than 40.0 %. The lowest proportion of people participating in social networks was recorded in the northern German region of Bremen (34.1 %; low reliability due to small case unit), while the other two German regions were the eastern regions of Brandenburg and Mecklenburg-Vorpommern. The lowest proportion of people participating in social networks in France was recorded in the outermost region of Guadeloupe (36.0 %), while three rural regions – Franche-Comté, Limousin, and Centre – Val de Loire also recorded relatively low shares.

The wide differences in participation rates for social networks may, at least in part, be linked to whether (or not) people are connected to the internet. Relatively low rates of internet access will, by definition, limit the potential use of social networks. However, internet access was generally widespread in much of France and Germany. As such, other factors may be relevant, for example, an ageing population structure in certain regions, or issues linked to privacy and the willingness of individuals to share their data online. By contrast, despite relatively low overall levels of internet access, many eastern regions of the EU recorded relatively high shares of people participating in social networks.

_RYB2023.png)

(people aged 16–74, by NUTS 2 regions)

Source: Eurostat (isoc_r_iuse_i) and (isoc_ci_ac_i)

Figure 2 provides information about those EU regions with the largest changes in their share of people participating in social networks between 2019 and 2022. In 155 regions out of 196 for which data are available in the EU, the share of people participating in social networks rose during the period under consideration. There were 41 regions that recorded increases of at least 10.0 percentage points, with the largest increases in Northern and Western (Ireland; up 16.3 percentage points) and the capital region of Attiki (Greece; NUTS level 1; up 16.0 points). There were three other regions where the share of people participating in social networks increased by more than 15.0 points: Severozapaden (Bulgaria), Corse (France; low reliability) and Molise (Italy).

At the other end of the range, there were 40 regions across the EU where the proportion of people participating in social networks fell between 2019 and 2022. Among these, there were six regions that recorded a fall of at least 10.0 percentage points:

- the biggest decline was observed in Prov. Liège (Belgium; down 16.7 points), while another Belgian region, Prov. Luxembourg, also recorded a double-digit reduction;

- there were also relatively large falls in two German regions (NUTS level 1) – Bremen (down 13.4 points; low reliability due to small case unit) and Sachsen-Anhalt (down 10.5 points);

- the other two regions with falls of at least 10.0 points were geographically remote, located at opposite ends of the EU – the Swedish region of Övre Norrland (down 12.3 points) and the Spanish region of Ciudad de Ceuta (down 10.8 points).

_RYB2023.png)

(percentage points difference compared with 2019, people aged 16–74, by NUTS 2 regions)

Source: Eurostat (isoc_r_iuse_i) and (isoc_ci_ac_i)

Internet banking

In recent years, one of the main developments within the EU’s banking sector has been an expansion of online services. The frequency with which consumers visit their local branch has fallen rapidly, the number of branches has contracted, and online transfers and e-payments have become the norm. Some markets have seen the emergence of internet (or ‘virtual’) banks that do not have any physical branches. These internet banks eliminate the overheads associated with running local branches and are often in a better position to offer more competitive services than ‘bricks and mortar’ banks. In response, some traditional banks have expanded their products and diversified their distribution channels (‘click and mortar’ banks), integrating online banking into their group either though organic growth or the acquisition of internet-based competitors.

Almost three fifths of the EU population made use of internet banking

Almost three fifths (59.7 %) of the EU’s population aged 16–74 used the internet for banking during the three months preceding the 2022 survey. As with most internet activities, there were some quite large differences between age groups concerning the use of internet banking. Some young people do not (yet) have a bank account, and therefore by definition, they have no need for internet banking. However, the share of the EU’s adult population making use of the internet for banking rises quickly, with around three quarters (75.1 %) of people aged 25–29 making use of these online services. By contrast, just over one third (36.1 %) of persons aged 65–74 used internet banking.

Map 3 shows the proportion of people aged 16–74 using internet banking during the three months preceding the 2022 survey for NUTS level 2 regions; note again that data for Germany, Greece, Poland and Türkiye relate to level 1 regions. The use of internet banking across EU regions reflects, to some degree, the availability of broadband internet connections and the nature of internet banking services that are on offer. Nevertheless, an individual’s choice as to whether or not they use the internet for banking often comes down to a matter of trust, which may reflect, among other factors, national characteristics. For example in 2022, more than 90.0 % of the population made use of internet banking in every region of Denmark and Finland (no data available for Åland), and in 9 out of the 12 regions in the Netherlands. At the other end of the range, those regions where the use of internet banking was considerably below the EU average were predominantly located in eastern and southern regions of the EU. For example, less than one quarter of the population used the internet for banking in all but one region each of Bulgaria and Romania; the exceptions were their respective capital regions of Yugozapaden and Bucureşti-Ilfov, where the share of people using internet banking was close to one third. Issues around access to financial services may explain, at least to some degree, these very low figures, as a relatively high proportion of people in Bulgaria and Romania do not possess a bank account.

The highest shares of internet banking were recorded in the Finnish and Danish capital regions

A more detailed analysis of the latest information from Map 3 reveals the highest proportions of people making use of internet banking were recorded in the Finnish and Danish capital regions of Helsinki-Uusimaa (95.9 %) and Hovedstaden (95.4 %). By contrast, the lowest proportions were recorded in Romania, where four regions had shares below 15.0 %; the lowest proportion was observed in Sud-Est (12.9 %).

People living in rural regions are more likely to face limited access to a physical branch of their bank; however, the use of internet banking was generally lower in rural and remote regions (than it was in urban regions). Outside of Bulgaria and Romania, some of the lowest penetration rates for online banking were recorded in regions characterised by a low level of internet connectivity and/or an older population age structure. For example, less than one third of people aged 16–74 from the southern Italian regions of Calabria, Campania, Basilicata, Puglia and Sicilia made use of internet banking in 2022.

_RYB2023.png)

(people aged 16–74, by NUTS 2 regions)

Source: Eurostat (isoc_r_iuse_i) and (isoc_ci_ac_i)

Figure 3 provides information for those regions with the largest changes in their share of people making use of internet banking between 2019 and 2022. For the EU as a whole, there was an increase in the use of internet banking, up 5.1 percentage points to 59.7 %. A regional analysis reveals that the proportion of people making use of internet banking rose in more than four fifths of the 196 regions for which data are available across the EU. There were 84 regions that recorded double-digit increases, with the biggest gain, by far, observed for the Spanish region of Ciudad de Melilla (up 39.6 percentage points). This was followed by eight regions that recorded increases within the range of 20.5–23.4 points:

- two more regions in Spain – Región de Murcia and Illes Balears (Spain);

- the capital regions of Attiki (Greece; NUTS level 1), Yugozapaden (Bulgaria) and Bucureşti-Ilfov (Romania);

- Cyprus, Guadeloupe (France) and Northern and Western (Ireland).

There were 35 regions across the EU where the penetration of online banking declined between 2019 and 2022. Among these, there were 12 regions where the proportion of people aged 16–74 making use of internet banking fell by at least 10.0 percentage points. The vast majority of this group – 10 regions – were located across Germany (NUTS level 1), with the share of people making use of internet banking falling at a particularly fast pace in Bremen (down 27.6 percentage points) and Sachsen-Anhalt (down 25.7 points). Övre Norrland (Sweden) and Ciudad de Ceuta (Spain) were the other two regions across the EU where double-digit falls in the use of internet banking were observed.

_RYB2023.png)

(percentage points difference compared with 2019, people aged 16–74, by NUTS 2 regions)

Source: Eurostat (isoc_r_iuse_i) and (isoc_ci_ac_i)

E-commerce

E-commerce has the potential to make it easier for consumers to compare different retail offers. It can reconfigure the geography of consumption, for example, extending consumer choice and influencing price competition in remote regions of the EU. At the same time, it may transfer the time and cost burden of travelling to shops from consumers to distributors. The ability to shop 24 hours a day, coupled with the ease of making electronic payments, is gradually leading to a digital transformation of the EU’s retail space, disrupting many aspects of shopping behaviour; this development was reinforced during the COVID-19 crisis. Nevertheless, the vast majority of retail sales within the EU continue to take place in shops.

For statistical purposes, e-commerce is defined as ‘buying goods or services through electronic transactions, including the placing of orders for goods or services over the internet (payment and the ultimate delivery of the goods or service may be conducted either online or offline); orders via manually typed e-mails are excluded’.

Across the EU, more than two thirds of the population used e-commerce

In 2022, more than two thirds (68.0 %) of the EU’s population aged 16–74 reported that they had bought/ordered goods or services over the internet in the 12 months preceding the survey. As with many other internet activities, the propensity to make use of e-commerce is closely linked to age. For example, a particularly high proportion (85.3 %) of people aged 25–34 made use of the internet to buy/order goods or services; this was 2.4 times as high as the corresponding share (35.7 %) recorded for older people aged 65–74. The share of people reporting that they had bought/ordered goods or services over the internet was higher among those people living in cities (71.6 %) than it was for people living in rural areas (64.1 %).

More than 90.0 % of people made use of e-commerce in the capital regions of Czechia, Denmark and the Netherlands; this was also the case in another region from the Netherlands, namely Limburg

There were 41 regions across the EU where at least four fifths of people aged 16–74 had bought/ordered goods or services over the internet in the 12 months preceding the 2022 survey. Map 4 shows these regions were largely concentrated across Denmark, Ireland, France, the Netherlands and Sweden; note again that data for Germany, Greece and Poland relate to NUTS level 1 regions (as do the data for Türkiye). The highest propensities to make use of e-commerce were recorded in three capital regions – Hovedstaden (Denmark; 91.3 %), Noord-Holland (the Netherlands; 90.3 %) and Praha (Czechia; 90.1 %) – as well as a further region in the Netherlands, Limburg (90.9 %).

At the other end of the range, there were 56 regions where less than three fifths of the population made use of e-commerce. The lowest proportions of people using e-commerce were concentrated in eastern and southern regions of the EU, particularly across Bulgaria, Romania, Italy and Portugal; this may reflect, at least in part, relatively low levels of internet access/use and relatively high numbers of people not possessing bank accounts and/or a credit card (thereby making it more difficult to pay online). There was also a relatively low propensity to make use of e-commerce in several of the French, Portuguese and Spanish outermost regions; these low shares may, at least in part, be linked to relatively high shipping costs for goods purchased online. Looking in more detail, there were three regions in the EU where less than one third of all people made an online purchase during the 12 months preceding the 2022 survey. Two of these regions were located in Bulgaria – Yugoiztochen (31.9 %) and Severen tsentralen (29.9 %) – while the third was Calabria in southern Italy (also 31.9 %).

_RYB2023.png)

(people aged 16–74, by NUTS 2 regions)

Source: Eurostat (isoc_r_blt12_i) and (isoc_ec_ib20)

Just over one sixth of the EU population reported that they had never made an online purchase

In contrast to the information presented above, Map 5 provides a more detailed analysis of e-commerce insofar as it shows how recently people ordered goods or services over the internet; note that all of the data are presented for NUTS level 1 regions. When surveyed in 2022, some 56.1 % of people aged 16–74 in the EU confirmed that they had made an online purchase during the previous three months. Relatively few people made irregular use of e-commerce:

- 11.9 % had made their last online purchase some 3–12 months prior to the survey (bringing to 68.0 % the share of people having made their last online purchase anytime during the 12 months before the survey);

- 5.8 % had made their last online purchase more than a year before the survey;

- whereas 17.2 % of people reported that they had never made an online purchase.

The overall pattern for the EU was repeated in the vast majority of regions (no data for Åland, Finland): in 2022, there were 82 out of 91 NUTS level 1 regions where the most common response when asked about their latest online purchase was for people aged 16–74 to say that they had made a purchase during the three months preceding the 2022 survey. More than three quarters of all people reported that they had made an online purchase in Denmark and Ireland, as well as all four regions of the Netherlands, and two out of the three regions in Sweden (the exception being Norra Sverige).

By contrast, there were nine NUTS level 1 regions where the most common response when asked about their latest online purchase was for people to say that they had never made an online purchase: two regions in each of Bulgaria, Italy and Romania, as well as island regions in France, Cyprus and Portugal. Looking in more detail, there were five regions where more than one third of all people reported that they had never made an online purchase: Cyprus had the highest share at 36.7 %, closely followed by Região Autónoma da Madeira (Portugal; 36.1 %), Sud (Italy; 34.9 %), Macroregiunea Patru (Romania; also 34.9 %) and Isole (Italy; 34.2 %).

_RYB2023.png)

(%, people aged 16–74, by NUTS 1 regions)

Source: Eurostat (isoc_r_blt12_i) and (isoc_ec_ib20)

Just over one sixth of the EU population reported that they had made an online purchase from a seller in another EU Member State

The final map in this chapter provides more detailed information in relation to one specific aspect of e-commerce developments. Across the EU, some 17.2 % of people aged 16–74 made online purchases over the internet from sellers in other EU Member States during the three months preceding the 2022 survey; this figure was 1.0 percentage point lower than a year before, when the impact of the COVID-19 crisis may have led to more people making online purchases from other Member States as a range of restrictions prevented/deterred them from in-store shopping, whether locally or in another country.

There were 23 NUTS level 2 regions where at least 35.0 % of people ordered goods or services over the internet from sellers in other EU Member States during the three months preceding the 2022 survey (as shown by the darkest shade in the map); note again that data for Germany, Greece and Poland relate to level 1 regions (as do the data for Türkiye). These 23 regions were concentrated across Ireland (all three regions), Austria (all nine regions) and Belgium (8 out of 11 regions, the exceptions being in the southern Région wallonne). Relatively high shares were also recorded in Luxembourg and Malta, as well as Hovedstaden (the capital region of Denmark). Note that many of these regions are in Member States which have larger neighbouring Member States that use the same or a similar language, thereby reducing the impact of language barriers for cross-border shopping.

At the other end of the range, there were 11 regions in the EU where the share of people making online purchases from sellers in other EU Member States was less than 5.0 % (as shown by the lightest shade in the map). These regions were, unsurprisingly, characterised by a relatively low propensity to use e-commerce in general and were principally located across Bulgaria and Romania, but also included the northern German region of Mecklenburg-Vorpommern (NUTS level 1), the French outermost region of La Réunion, and the eastern Polish region of Makroregion wschodni (also NUTS level 1).

Luxembourg was the only region in the EU where a majority of the population made online purchases from sellers in other EU Member States

In 2022, Luxembourg had the highest share of people aged 16–74 who made online purchases from sellers in other EU Member States during the three months preceding the survey, some 51.2 %. Almost half (49.9 %) of the population living in the Irish capital region of Eastern and Midland used e-commerce to purchase goods and/or services from sellers in other EU Member States, while relatively high shares – more than 45.0 % – were also observed in three Belgian regions, Prov. Limburg, Prov. Oost-Vlaanderen and Prov. Brabant Wallon. By contrast, there were four regions within the EU where less than 3.0 % of the population made online purchases from sellers in other EU Member States: Severen tsentralen (Bulgaria), Nord-Est, Sud-Muntenia, and Vest (all in Romania). Vest had the lowest regional share in the EU, at 2.4 %.

_RYB2023.png)

(%, people aged 16–74, by NUTS 2 regions)

Source: Eurostat (isoc_r_blt12_i) and (isoc_ec_ibos)

Source data for figures and maps

Data sources

European ICT surveys aim to provide timely statistics on individuals, households and enterprises relating to their use of ICTs. Many of these statistics are used in the benchmarking framework associated with one of the European Commission’s six priorities for the period 2019–2024: A Europe fit for the digital age. This strategy is built on three pillars: i) technology that works for people; ii) a fair and competitive digital economy; iii) an open, democratic and sustainable society.

The data in this chapter are based on an annual survey on ICT usage in households and by individuals. The legal basis for the 2022 survey is Regulation (EU) 2019/1700 of the European Parliament and of the Council establishing a common framework for European statistics relating to persons and households, based on data at individual level collected from samples. In this fast-changing environment, this framework is implemented through a series of annual regulations that specify the detailed information to be collected, making it possible for the survey to be tailored to emerging technological developments, so that policymakers can have access to data that measure the impact of new technologies and services. For 2022, the survey was implemented by Regulation (EU) 2021/1223 and supplemented by Regulation (EU) 2021/1898.

The statistical units for regional data on ICTs are the household or the individual. The population of households consists of all households having at least one member in the age group 16–74. The population of individuals consists of all persons aged 16–74. Questions on access to ICTs are addressed to households, while questions on the use of ICTs are answered by individuals within the household. The information presented (and the underlying database) are organised according to survey years; the results presented refer to individuals’ experiences during the 3 or 12 months prior to a survey.

Regional statistics on ICT are generally available for NUTS level 2 regions. However, the latest data for Germany, Greece and Poland are only provided for NUTS level 1 regions; a similar situation exists for Türkiye. For reference year 2021, the implementation of a new legal basis for the collection of statistics on the digital society (the framework regulation for the production of European statistics on persons and households (Integrated European Social Statistics – IESS)) resulted in a considerable level shift from one year to the next in relation to the data provided by several EU Member States (principally Belgium, Germany and Ireland). Note that while this may impact analyses over time, the bulk of the information presented in this chapter concerns reference years 2021 and 2022 (and therefore is not affected by any breaks in series).

Indicator definitions

Internet users

An internet user, in the context of information society statistics in the EU, is defined as a person aged 16–74 making use of the internet in whatever way:

- whether at home, at work or from anywhere else;

- whether for private or professional purposes;

- regardless of the device or type of connection used.

Internet activities

People participating in social networks refers to people creating user profiles, posting messages or other contributions to websites and applications such as Facebook, Instagram, Snapchat, TikTok or Twitter.

People using internet banking refers to the use of online banking services either through a website or an app (application).

E-commerce

E-commerce can be defined generally as the sale or purchase of goods or services, whether between businesses, households, individuals or private organisations, through electronic transactions conducted via the internet or other computer-mediated (online communication) networks. The term covers the ordering over computer networks of goods and services, but the payment and the ultimate delivery of the good(s) or service(s) may be conducted either online or offline.

E-commerce by individuals or households via the internet is defined more specifically as the placing of orders for goods or services via the internet; orders via manually typed e-mails are excluded. Also included in the definition are:

- buying financial investments – such as shares;

- making reservations for accommodation and travel;

- participating in lotteries and betting;

- paying for information services from the internet;

- buying via online auctions.

Context

European Commission priorities

In 2019, the European Commission President, Ursula von der Leyen, described how she wanted the EU to grasp the opportunities presented by the digital age. Indeed, A Europe fit for the digital age is one of six Commission priorities for the period 2019–2024. Such a digital transformation is based on the premise that digital technologies and solutions should: open up new opportunities for businesses; boost the development of trustworthy technology; foster an open and democratic society; enable a vibrant and sustainable economy; help fight climate change.

With this in mind, during February 2020 the European Commission adopted an overarching presentation of ideas and actions for Shaping Europe’s Digital Future, as well as specific proposals in relation to:

Digital society and digital technologies bring with them new ways to learn, entertain, work, explore, and fulfil ambitions. They also bring new freedoms and rights, and give people living in the EU the opportunity to reach out beyond physical communities, geographical locations, and social positions. However, there are also challenges associated with this digital transformation that need to be addressed. For example, the EU seeks to increase its strategic autonomy in technology and develop new rules and technologies to protect citizens from, among other threats, counterfeit products, cybertheft, and disinformation.

The European data strategy aims to make the EU a leader for data-driven societies. Creating a single market for data should allow information to flow freely within the EU and across sectors for the benefit of businesses, researchers and public administrations. All of these actors should be empowered to make better decisions based on insights from non-personal data, which should be available to all, while ensuring that EU rules, in particular privacy and data protection, are fully respected.

In March 2021, a European Commission communication Digital Compass: the European way for the Digital Decade ((COM) 2021 118 final) set out the EU’s digital ambitions for the next decade in the form of clear, specific targets. The digital compass identifies a number of goals to be reached over the remainder of the decade:

- a digitally skilled population and highly skilled digital professionals;

- secure and sustainable digital infrastructures;

- the digital transformation of businesses;

- the digitisation of public services.

In January 2022, the European Commission made a proposal Establishing a European declaration on digital rights and principles for the digital decade (COM(2022) 27 final). It is shaped around six key areas:

- putting people and their rights at the centre of the digital transformation;

- supporting solidarity and inclusion;

- ensuring the freedom of choice online;

- fostering participation in digital public spaces;

- increasing the safety, security and empowerment of individuals;

- promoting the sustainability of a digital future.

In July 2022, a new ‘Roaming regulation’ entered into force. Regulation (EU) 2022/612 of the European Parliament and of the Council on roaming on public mobile communications networks within the Union extends ‘Roam-like-at-home’ until 2032 – this revised scheme:

- allows travellers in the EU to call, text and surf abroad without extra charges, whilst enjoying the same quality of mobile service as they have at home;

- improves access to emergency communications across the EU;

- guarantees clear information about services that may be subject to extra charges.

In November 2022, the Digital Markets Act (Regulation (EU) 2022/1925) and the Digital Services Act (Regulation (EU) 2022/2065) entered into force. The Digital Markets Act establishes a set of objective criteria for qualifying large online platforms as ‘gatekeepers’ (characterised by their strong economic or intermediation position). The act aims to ensure that these platforms behave in a fair way:

- promoting a fairer business environment;

- providing new opportunities for innovators and start-ups to compete;

- giving consumers more and better services and the opportunity to switch provider;

- preventing unfair practices.

The “Digital Services Act” sets out new standards for the accountability of online platforms across the EU. It is designed to ensure better protection for internet users and their fundamental rights. It creates new obligations for online platforms to reduce harm and counter risks, while placing them under a new transparency and accountability framework. Designed as a single, uniform set of rules for the EU, the act, among other points:

- creates stronger public oversight of online platforms (in particular, those that reach more than 10 % of the EU’s population);

- is designed to increase the mechanisms for the removal of illegal content and for the effective protection of users’ fundamental rights;

- provides measures to counter illegal goods, services or content online;

- introduces new obligations on the traceability of business users in online market places;

- provides safeguards for users, including the possibility to challenge platforms’ content moderation decisions;

- bans certain type of targeted adverts;

- increases obligations for very large platforms and search engines to prevent the misuse of their systems.

The recovery plan for Europe

The centrepiece of the EU’s recovery plan from the COVID-19 crisis is the Recovery and Resilience Facility that has a budget of €723.8 billion. The emergency European Recovery Instrument (also known as Next Generation EU), which complements the regular 2021–2027 multiannual financial framework, is the basis of funding for the Recovery and Resilience Facility. Among other aims, the facility will support digital transitions.

The European Commission’s proposal for the recovery plan noted that ‘investing in digital infrastructure and skills will help boost competitiveness and technological sovereignty’. Subsequently the 2021–2027 multiannual financial framework, which was adopted in December 2020, specifically included commitments of €7.6 billion for the Digital Europe Programme. This budget aims to strengthen investments in supercomputing (€2.2 billion), artificial intelligence (€2.1 billion), cybersecurity (€1.7 billion), and advanced digital skills (€580 million). An additional €1.1 billion is reserved for ensuring a wide use of digital technologies across the economy and society.

{kind=link}