Estimated reading time: 5 minutes

This report was published by Documentary Credit World (http://doccreditworld.com/).

Following the latest Q3 2022 edition of its quarterly letter of credit (LC) statistics for US banks, Documentary Credit World (DCW) has released its analysis of LC issuance from banks in the country.

The analysis examines the differences in the volumes of standby letters of credit (SBLCs) and commercial letters of credit (CLCs), as well as profiles of the banks – divided into a set of tiers – that tend to issue the documents.

The dataset determines bank tiers by comparing the “Net Letters of Credit” of each institution, which represents the combined total dollar amount of outstanding SBLCs and CLCs.

DCW’s analysis primarily shows three trends:

- US banks have SBLCs outstanding at a much higher dollar figure than CLCs.

- A small number of the largest banks have the majority of outstanding dollar values for SBLCs.

- Financial SBLCs comprise a much greater proportion of the total amount outstanding than performance SBLCs.

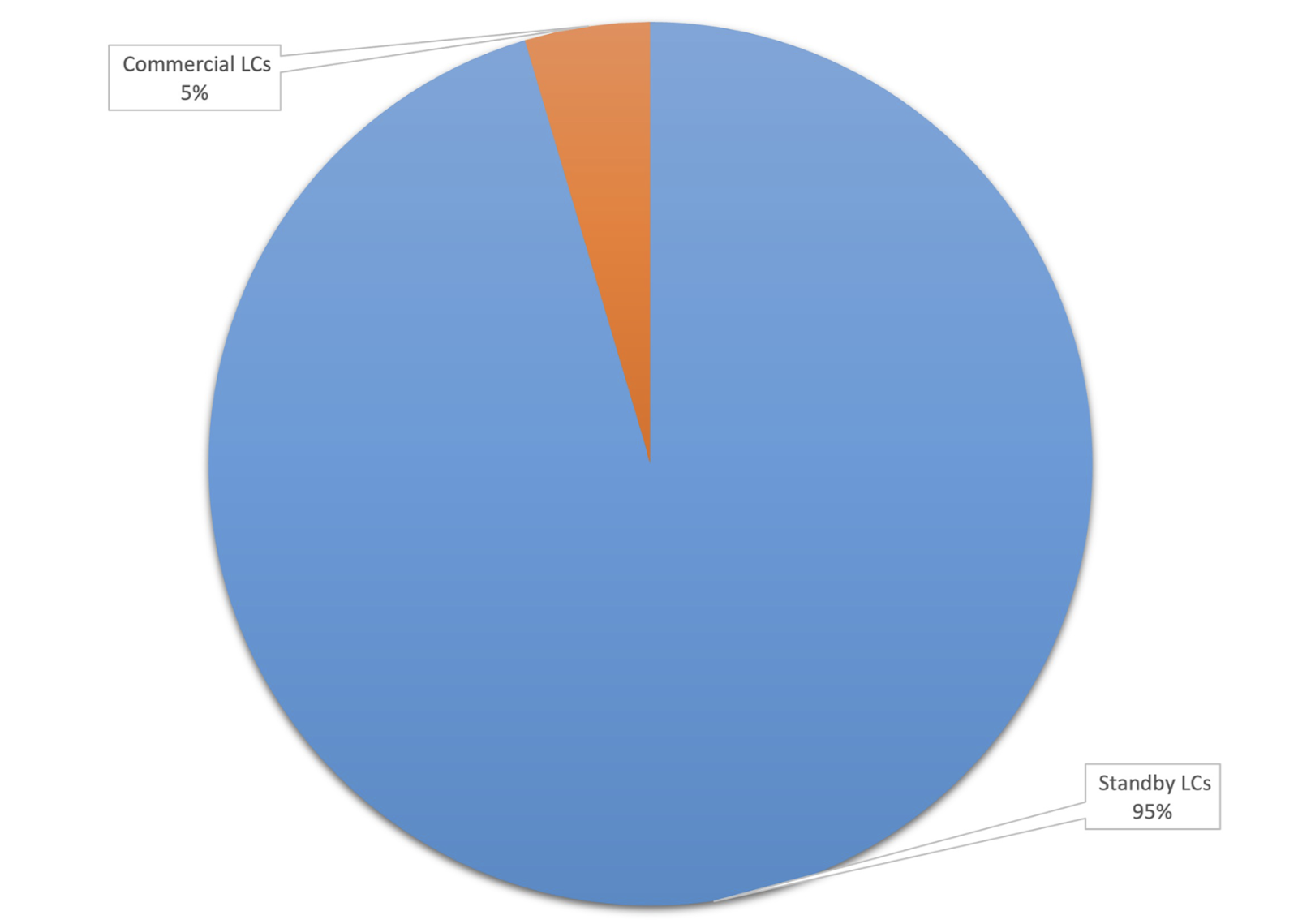

Greater outstanding dollar value for standby letters of credit than commercial letters of credit

According to DCW, there is $354.6 billion worth of outstanding SBLCs (representing about 95% of the total share) versus only $17 billion outstanding for CLCs (5%).

These findings support the intuitive nature of the primary applications of the two documents.

SBLCs are not used as a primary payment method for a transaction, but rather as a secondary method that acts as a guarantee in case a primary mechanism does not work.

Conversely, CLCs are generally the primary payment method to facilitate trade transactions.

This nature as a “backup” payment mechanism employed to instil confidence in a counterpart, coupled with an SBLC’s relative simplicity compared to a CLC means that it is a much more ubiquitous document.

By extension, it should come as little surprise that there is a larger dollar amount of them outstanding on the market than their commercial counterparts.

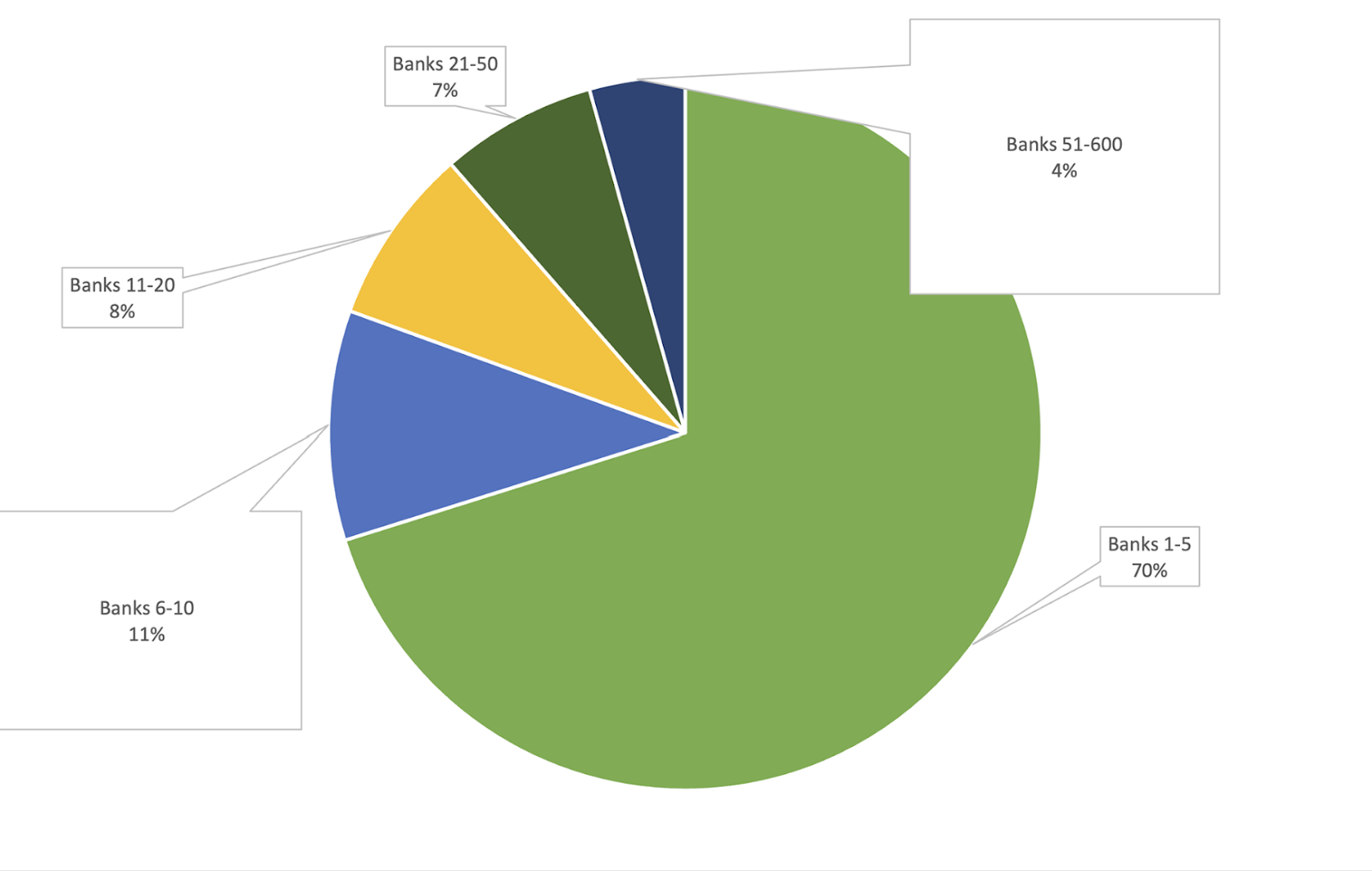

Five banks have more than 70% of outstanding SBLC amounts

To understand the distribution of outstanding LC amounts better, DCW categorised the top 600 US banks into five tiers: banks 1-5, 6-10, 11-20, 21-50, and 51-600.

This breakdown revealed that banks 1-5 have $260.8 billion worth of SBLCs outstanding on the market (more than 70% of the total).

Banks 6-10 have $38.6 billion (11% of the total), banks 11-20 have $29.9 billion (8%), banks 21-50 have $23.6 billion (7%), and the remaining 550 banks combined have only $16.1 billion outstanding (4%)

This large concentration of outstanding SBLC value at the top of the banking sphere is likely due to several factors.

First, the top banks are more likely to have a strong reputation and the financial stability needed to fulfil the terms of an LC if called upon to do so. They also generally have more experience issuing and handling SBLCs than many smaller institutions. This results in these banks being more sought after by companies and increases their attractiveness to all sides of an international commercial transaction.

Another reason is that larger banks already have vast networks of correspondents and relationships with other financial institutions worldwide, allowing them to serve a diverse group of clients.

Given the recent cost-saving trend of cutting correspondent banking relationships, businesses in many regions are likely to have no choice but to interact with one of the larger banks if they wish to complete a particular transaction.

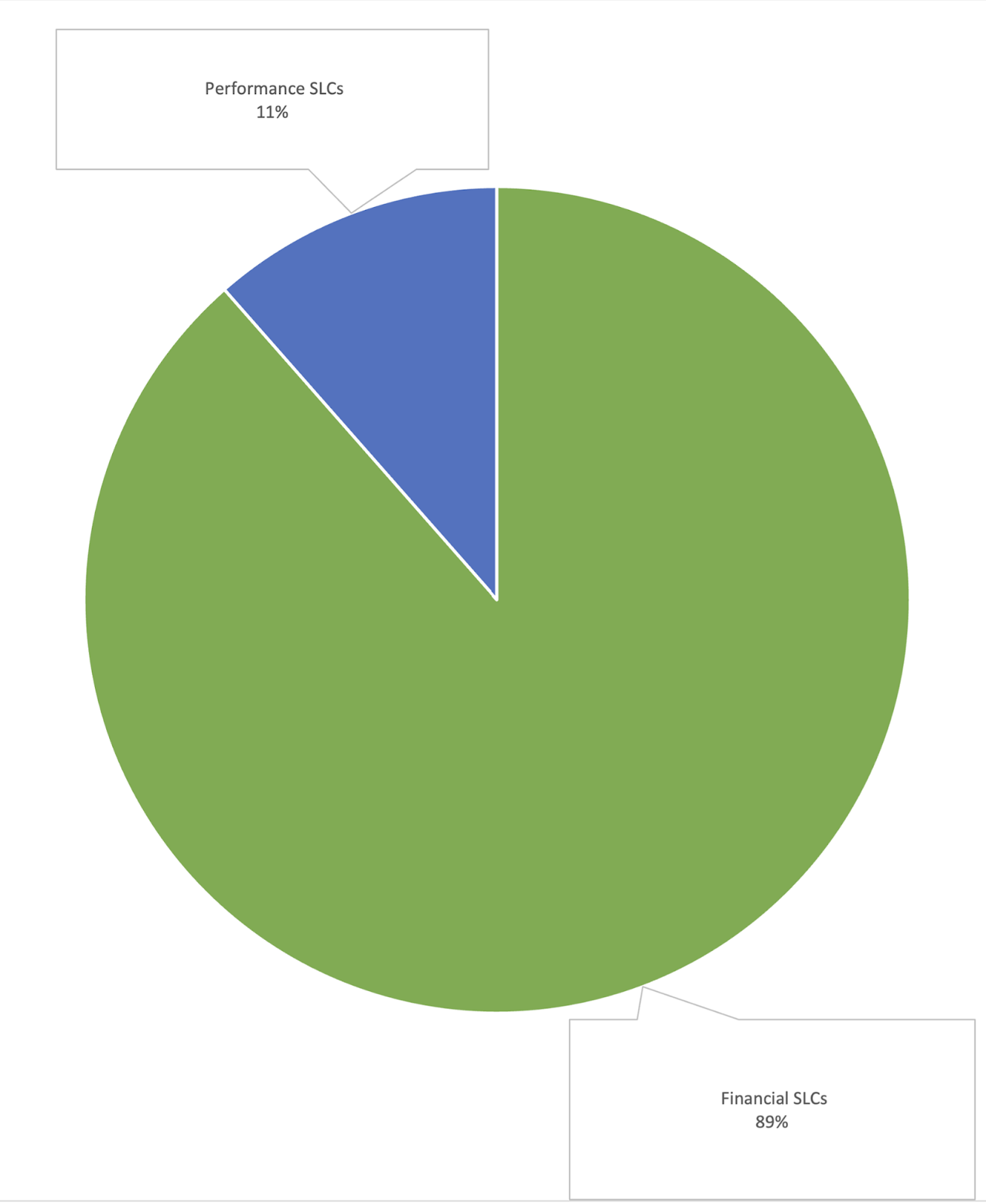

More financial SBLC value outstanding than performance SBLC

The DCW report also examined the composition of the type of SBLCs that are outstanding on the market.

There are two main types of SBLCs: financial and performance.

A financial SBLC provides a guarantee to the seller that they will receive payment for goods or services specified by a contract, with the buyer’s bank agreeing to reimburse the seller if the buyer fails to pay.

A performance SBLC, on the other hand, guarantees the buyer that the seller will complete the project outlined in a contract, with the seller’s bank agreeing to reimburse the buyer if the seller fails to complete the project.

Financial SBLCs are generally more common than performance SBLCs, and they are generally issued for much larger amounts.

The DCW report, which indicates the value outstanding for financial SBLCs (89% of the total at $313.8 billion) is substantially larger than that of performance SBLCs (11% at $40.6 billion), further supports this.

The continuing importance of the letter of credit

LCs continue to be a vital tool for businesses and financial institutions to manage risk and facilitate trade.

The data demonstrates a strong demand for these financial instruments in various industries and transactions and highlights the importance of financial guarantees in today’s economy.

The analysis of LC statistics provides valuable insight into the current state and direction of the market. Understanding these statistics is crucial for businesses and financial institutions to make informed decisions and manage risk effectively.

To read more from Documentary Credit World, visit the Institute of International Banking Law & Practice at https://iiblp.org/.