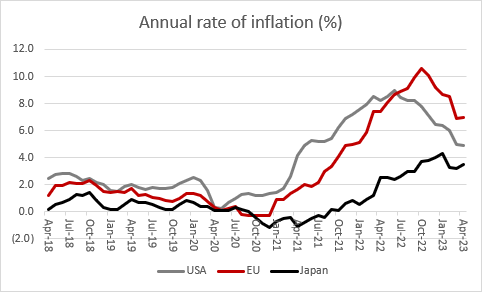

It is one of those weeks when central banks take centre stage, because the US Federal Reserve, the European Central Bank and the Bank of Japan are all scheduled to make their latest policy decisions. The BoJ may be pleased to see inflation, after flirting with deflation for most of the last three decades, and seems in little rush to curb an inflation rate of 3.5% but policymakers may feel they have more work to do in America and Europe, even if the rate of price increases is decelerating.

Source: US Bureau for Labor Statistics, Eurostat, Bank of Japan. USA and Japan based on CPI, EU on HICP

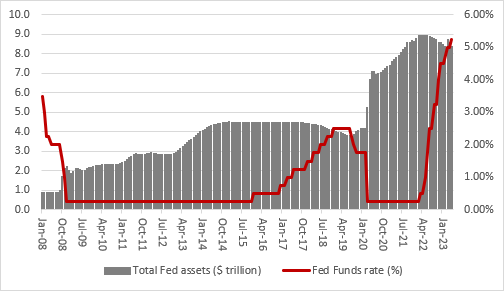

The US Federal Reserve will be first up on Wednesday 14 June. The Fed has taken the Fed Funds rate to 5.25% from 0.25% in just over a year and started to run a Quantitative Tightening (QT) programme to withdraw monetary stimulus and shrink its balance sheet at the rate of $90 billion a month. After a blip when a series of regional banks went under in March, the Fed’s balance sheet has so far shrunk by $550 billion, or some 6%, from its peak to $8.4 trillion worth of assets.

At this meeting, the markets are putting a 77% chance on no change in the Fed funds rate at 5.25% but they then see a 65% chance of a hike in July and a similar chance of one in September to a peak of 5.75% before the first cut in either November or December.

Source: US Federal Reserve, FRED – St. Louis Federal Reserve database, Refinitiv data

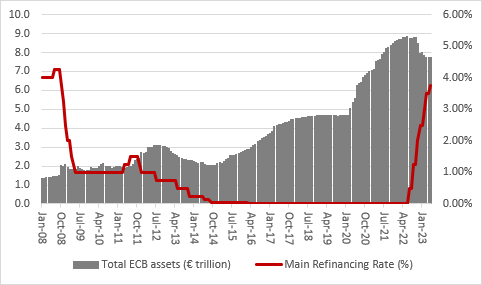

The European Central Bank will be next, on Thursday 15 June. President Christine Lagarde, late to the rate-rising party, has now jacked up the Main Refinancing Rate to 3.75% from its low of zero and also launched QT, at the rate of €15 billion a month. So far, the ECB’s asset holdings have fallen by €1 trillion, or 12%, as the central bank has also called in cheap loans provided to banks (the Targeted Long-Term Refinancing Operations, or TLTROs). The ECB has also said it could reassess the pace of QT at this meeting. EU inflation is down to 6.1% from a peak of 10.6%, but this is still three times the ECB’s target and Mme Lagarde has told markets to expect more rate rises.

Source: European Central Bank, FRED – St. Louis Federal Reserve database, Refinitiv data

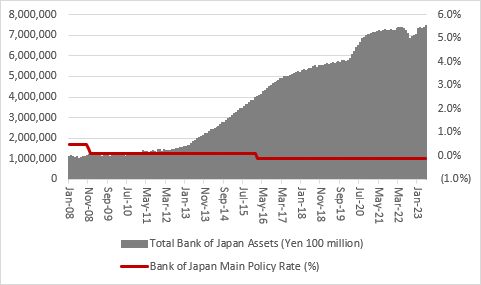

Finally, on Friday 16 June, comes the Bank of Japan. New Governor Kazuo Ueda is a rare creature indeed among central bankers, because he has not raised rates and nor has he abandoned Japan’s Quantitative and Qualitative Easing (QQE) scheme, whereby the Bank of Japan buys government bonds to cap the yield on the ten-year paper at 0.50%. No change is expected this time, either, even if inflation is now 3.5% and ahead of the 2% target, and this ongoing monetary stimulus could be one explanation for why the Nikkei 225 stock index keeps moving higher.

Source: Bank of Japan, FRED – St. Louis Federal Reserve database, Refinitiv data

These articles are for information purposes only and are not a personal recommendation or advice.

{kind=link}