** Please note that these remarks relate to the ECB’s activities in 2019 and were finalised before the global coronavirus (COVID-19) pandemic. The economic situation and the ECB’s policy actions have evolved substantially since that point. The ECB will do everything necessary within its mandate to help the euro area through this crisis. **

2019 marked the 20th anniversary of the introduction of the euro, and support for the single currency among euro area citizens reached an all-time high of 76% in the November Eurobarometer poll.

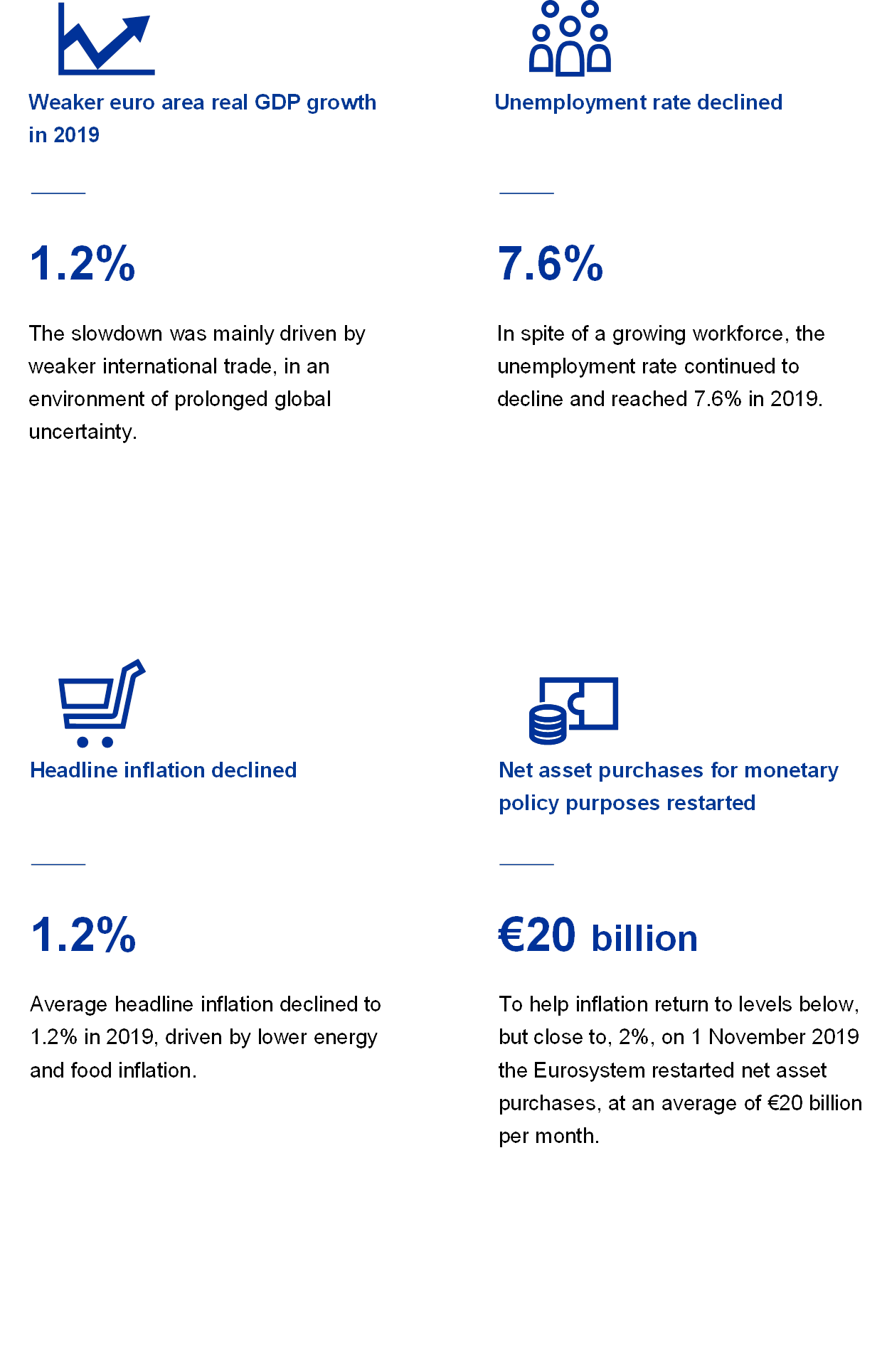

Euro area economic growth moderated further in 2019, to 1.2% from 1.9% in the previous year. The continued expansion was supported by favourable financing conditions, further employment gains and the mildly expansionary fiscal stance, although global trade-related uncertainty weighed most notably on manufacturing and investment.

Euro area labour markets continued to improve in 2019. The unemployment rate declined further to 7.6%, and wage growth remained robust, around its long-run average.

Headline inflation in the euro area stood at 1.2% on average in 2019, down from 1.8% in 2018. This decline reflected lower contributions from the two more volatile components, energy and food. Excluding these two components, inflation averaged 1.0% in 2019, the same as in the two previous years.

Against that background, the ECB’s Governing Council undertook further monetary accommodation in 2019 over three successive rounds. This included a new series of targeted longer-term refinancing operations, an extension of our forward guidance, a reduction in our deposit facility rate and the resumption of our asset purchase programme. By the end of 2019 there were some initial signs of a stabilisation of growth dynamics and a mild increase in underlying inflation.

As part of our policy assessment process, the Governing Council takes into consideration the impact of any potential side effects of our policy. In that vein, a two-tier system for reserve remuneration was introduced, which exempts a fraction of banks’ excess cash reserves from the negative deposit facility rate, in order to safeguard the bank-based transmission of monetary policy.

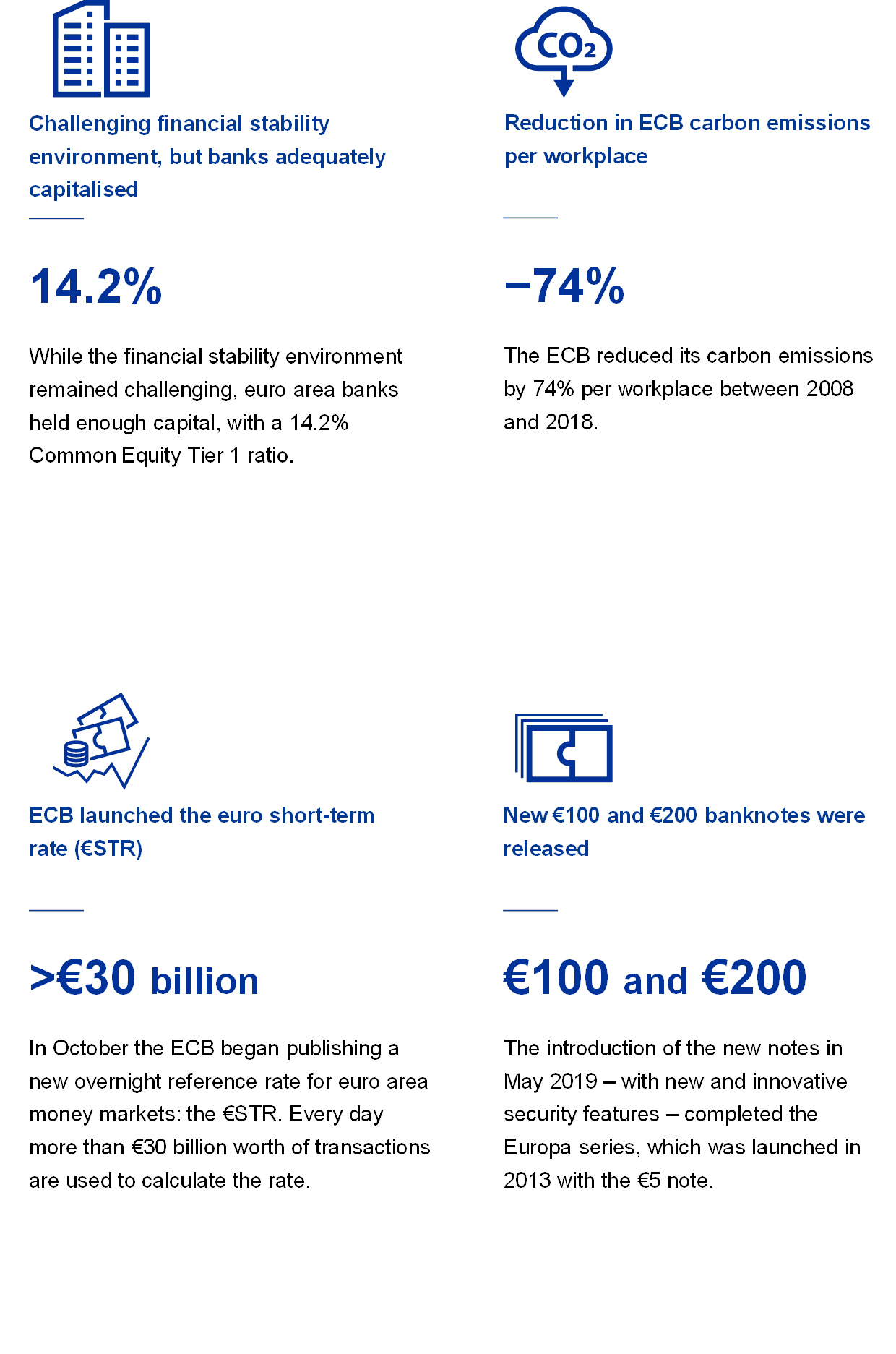

Structurally low profitability remains a challenge for euro area banks, although the sector is adequately capitalised, with a 14.2% Common Equity Tier 1 ratio. During 2019 strong risk-taking in financial and real estate markets continued to fuel the build-up of asset price vulnerabilities, while risks continued to increase in the growing non-bank financial sector. Euro area countries, in consultation with the ECB, implemented a number of macroprudential measures to mitigate and build up resilience to systemic risks.

The Eurosystem continued its efforts to ensure the smooth operation of payment systems. This included preparations for the replacement of TARGET2 with a new, state-of-the-art real-time gross settlement system and the adoption of a new retail payments strategy. The strategy supports the development of a market-led pan-European solution for point-of-interaction payments, to complement the successful Single European Payments Area.

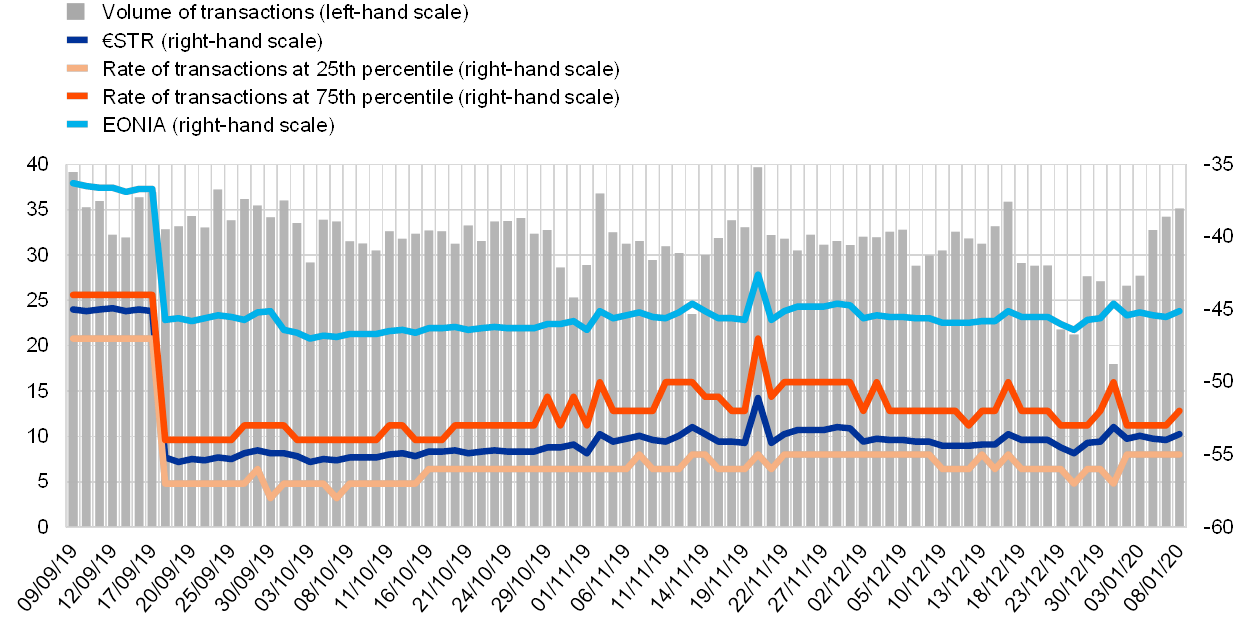

Publication of a new overnight reference rate, the €STR (euro short-term rate), began on 2 October, with the aim of replacing the current reference rate, EONIA, by January 2022. The daily production of the €STR has worked well and the methodology has proved reliable.

The ECB continues to study carefully the impact of climate change on the outlook for price stability and the financial system. This includes understanding the carbon intensity of bank lending portfolios and developing an analytical framework for carrying out a pilot climate risk stress-test analysis for the euro area banking sector. The ECB contributes to the efforts against climate change through its own investment decisions and environmental activities. We reduced carbon emissions and energy consumption per workplace by 74% and 54% respectively between 2008 and 2018.

2019 brought a renewed focus on engaging with a broader audience than financial markets and experts, and on listening more attentively to people’s concerns. Initiatives included the #EUROat20 competition, a new “ECB explains” video series and a monthly podcast.

Frankfurt am Main, May 2020

Christine Lagarde

President

After peaking in mid-2018, the global economy slowed down considerably in 2019 amid a sharp rise in trade-related uncertainty. The slowdown was broad-based and synchronised across countries. In this context, euro area economic growth moderated further, to 1.2% from 1.9% in the previous year. The growth moderation in 2019 was primarily driven by weaker international trade, in an environment of prolonged global uncertainty. At the same time, the slowdown was cushioned by favourable financing conditions, further employment gains and rising wages, the mildly expansionary euro area fiscal stance and the continued – albeit slower – growth in global activity. Euro area labour markets improved further, while productivity growth decelerated substantially. Inflationary pressures remained muted overall. Headline inflation declined to 1.2%, driven by lower energy and food inflation, while underlying inflation remained subdued. Favourable financing conditions continued to support credit and money growth. Euro area government bond yields declined significantly, whereas euro area equity prices increased mainly on account of lower discount rates. Household wealth was supported by increased valuations of real and financial assets.

1.1 The global economy slowed down considerably

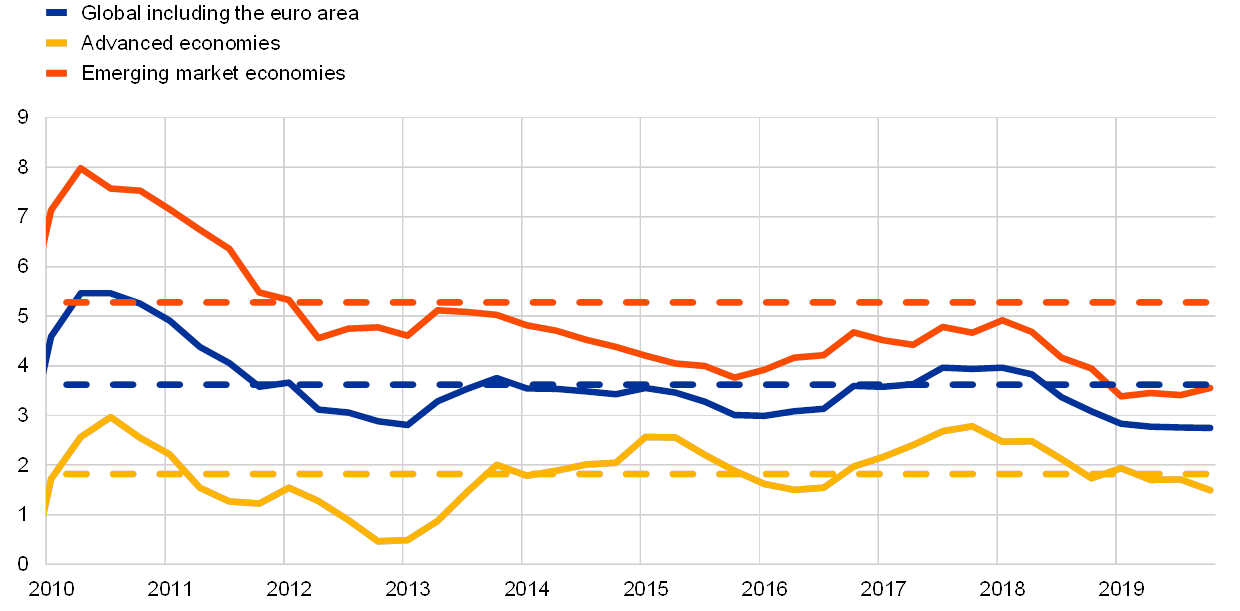

The global economy slowed down considerably in 2019 and the slowdown was broad-based and synchronised across countries

Over the course of 2019 global economic growth declined sharply. After peaking in mid-2018, the global economy slowed down considerably and grew at a rate that was well below the historical average and the weakest since the global financial crisis (see Chart 1). This global slowdown was broad-based and synchronised across countries. In large advanced economies such as the United States, the United Kingdom and Japan, this reflected a decrease from above average rates of growth. In China, growth declined to the lowest rate since 1990 and was around its currently estimated potential rate. Across other large emerging market economies, growth was generally lacklustre, partly reflecting a slow recovery from recent recessions.

Chart 1

Global GDP growth

(annual percentage changes; quarterly data)

Sources: Haver Analytics, national sources and ECB calculations.

Notes: Regional aggregates are computed using GDP adjusted with purchasing power parity weights. The solid lines indicate data and go up to the fourth quarter of 2019. The dashed lines indicate the long-term averages (between the first quarter of 1999 and the fourth quarter of 2019). The latest observations are for 10 March 2020.

The global economic slowdown was driven by a decline in manufacturing sector output and considerably weaker trade and investment growth. By contrast, services sector output growth moderated to a lesser extent, supported by relatively robust consumption growth and a continued improvement in labour markets.

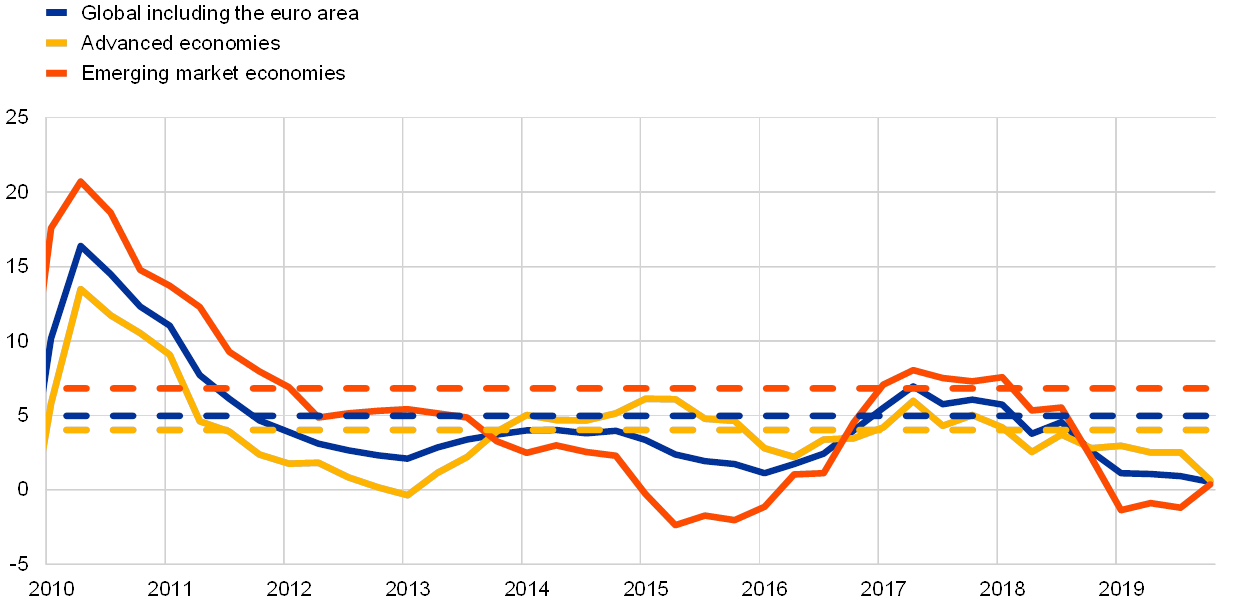

Trade and investment growth weakened considerably in 2019, driven by a sharp rise in trade-related uncertainty

Trade-related uncertainty rose sharply and remained elevated, weakening the global economy. Trade tensions between the United States and China escalated, as suggested by a range of different indicators.[1] Both countries raised tariffs on their bilateral trade. By the end of 2019 most US-China bilateral trade had been subject to higher tariffs. Trade uncertainty eased somewhat as a “phase one” trade agreement was announced in December following additional negotiations between the two countries since mid-October. The agreement was signed on 15 January 2020. Amid elevated trade tensions, the increase in tariffs drove the sharp decline in trade, while increased uncertainty and deteriorating economic sentiment held back investment growth in 2019 (see Chart 2).

Chart 2

Global trade growth

(annual percentage changes; quarterly data)

Sources: Haver Analytics, national sources and ECB calculations.

Notes: Global trade growth is defined as growth in global imports including the euro area. The solid lines indicate data and go up to the fourth quarter of 2019. The dashed lines indicate the long-term averages (between the fourth quarter of 1999 and the fourth quarter of 2019). The latest observations are for 10 March 2020.

Headline inflation fell, but core inflation remained broadly stable

Global inflation remained subdued in 2019, reflecting weak global growth momentum (see Chart 3). In the OECD area, headline annual consumer price inflation fell from around 3% in the second half of 2018 to 2.1% in December 2019 on account of falling energy prices and slowing food price inflation. However, underlying inflation (excluding energy and food) remained relatively steady at around 2% over the year.

Chart 3

OECD inflation rates

(annual percentage changes; monthly data)

Source: Organisation for Economic Co-operation and Development.

Note: The latest observations are for December 2019.

Oil prices fluctuated, driven by oil supply dynamics and expectations about global demand

Oil prices fluctuated over the year, reflecting oil supply dynamics in the first half of the year and expectations about global demand in the second half. The oil price fluctuated between USD 53 per barrel and USD 74 per barrel in 2019. In the first half of the year higher than expected cuts to production by OPEC+ (a group of major oil producers), as well as geopolitical tensions, supported an upward trend in oil prices. In the second half oil prices fell amid concerns about trade tensions and the possible impact on the global economy. The effects of the supply outage in Saudi Arabia following a drone attack on 14 September were short-lived as large inventories and the quick restoration of production capacity helped cushion the shock.

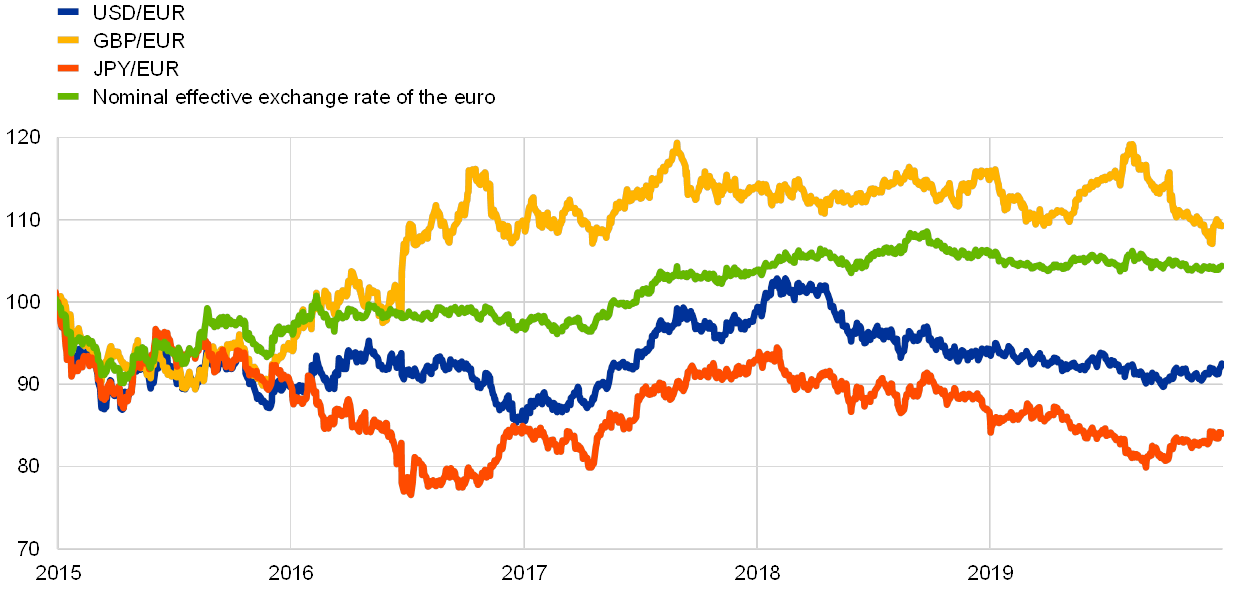

The euro depreciated against currencies of euro area trading partners

The euro depreciated by 1.6% in nominal effective terms over the course of 2019 (see Chart 4). In bilateral terms, this was driven by a depreciation of the euro against the US dollar and the Japanese yen. The euro-pound sterling exchange rate also declined, but exhibited significant volatility throughout 2019 mainly on account of changing Brexit developments.

Chart 4

The euro exchange rate

(daily data; 1 January 2015 = 100)

Sources: Bloomberg, Hamburg Institute of International Economics (HWWI), ECB and ECB calculations.

Notes: Nominal effective exchange rate against 38 major trading partners. The latest observations are for 31 December 2019.

The risks to the outlook for global growth were on the downside

At the end of 2019 the outlook for global growth entailed a moderation of growth as the economic cycle matured in advanced economies and as China gradually transitioned to a lower growth path, while the recovery in other emerging market economies remained fragile. This outlook was uncertain and, on balance, the risks to global activity were on the downside.[2] To the extent that the weakness in the manufacturing sector spread to the services sector, global activity could decelerate more quickly. In China, a sharper slowdown could have a larger effect on the global economy, while an escalation of the trade dispute would exacerbate the negative impact on global trade flows. In Europe, in particular, there was a risk that the United States might impose trade tariffs on some goods in several countries. In general, heightened geopolitical tensions could adversely affect global growth and trade. In addition, despite the United Kingdom’s orderly withdrawal from the European Union, there was uncertainty about the future EU-UK relationship and the outcome of the negotiations remained a downside risk. Moreover, a sharp repricing in global financial markets could dent risk appetite globally and affect real economic activity.

1.2 Euro area economic growth moderated, while labour markets continued to improve

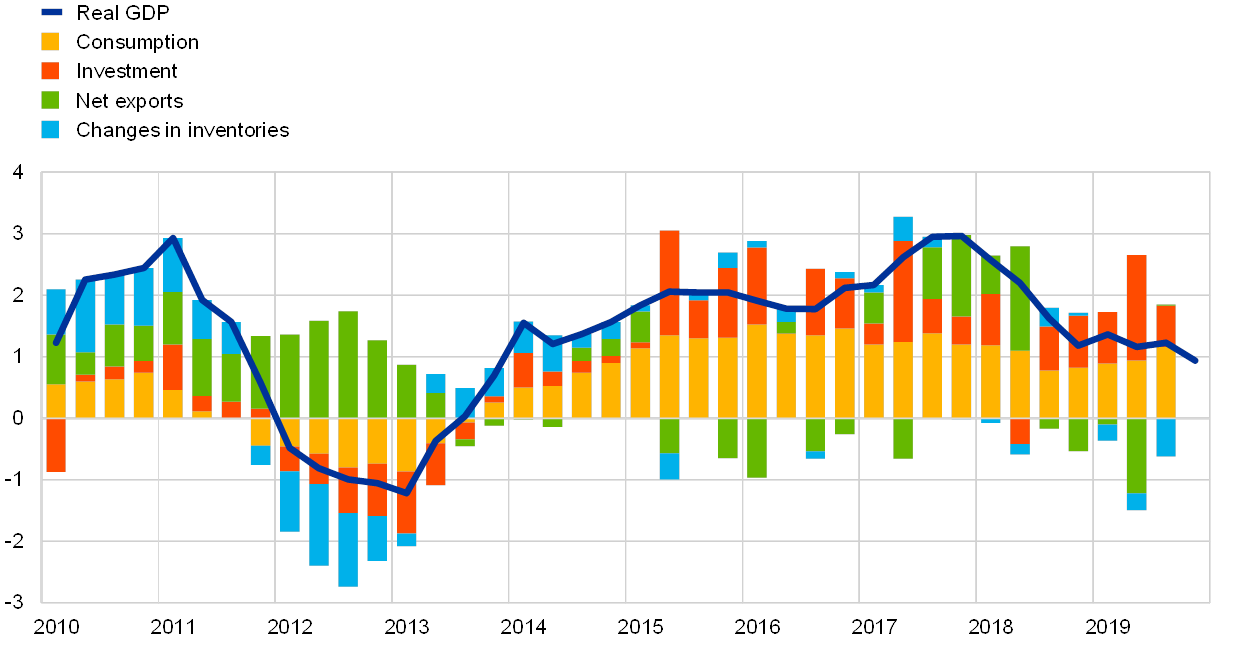

Euro area annual real GDP growth moderated further in 2019, reaching 1.2%, following growth of 1.9% in the previous year (see Chart 5). In contrast to the growth slowdown that took place in 2018, which was driven by weaker growth in both external and domestic demand, the growth moderation in 2019 was primarily driven by a marked weakening in international trade, in an environment of prolonged global uncertainty. At the same time, the euro area expansion continued to be supported by favourable financing conditions, further employment gains and rising wages, the mildly expansionary euro area fiscal stance and the continued – albeit slower – growth in global activity.

Chart 5

Euro area real GDP

(annual percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

Note: Annual GDP growth for the fourth quarter of 2019 refers to the preliminary flash estimate, while the latest observations for the components are for the third quarter of 2019.

Domestically oriented sectors showed more resilience in 2019

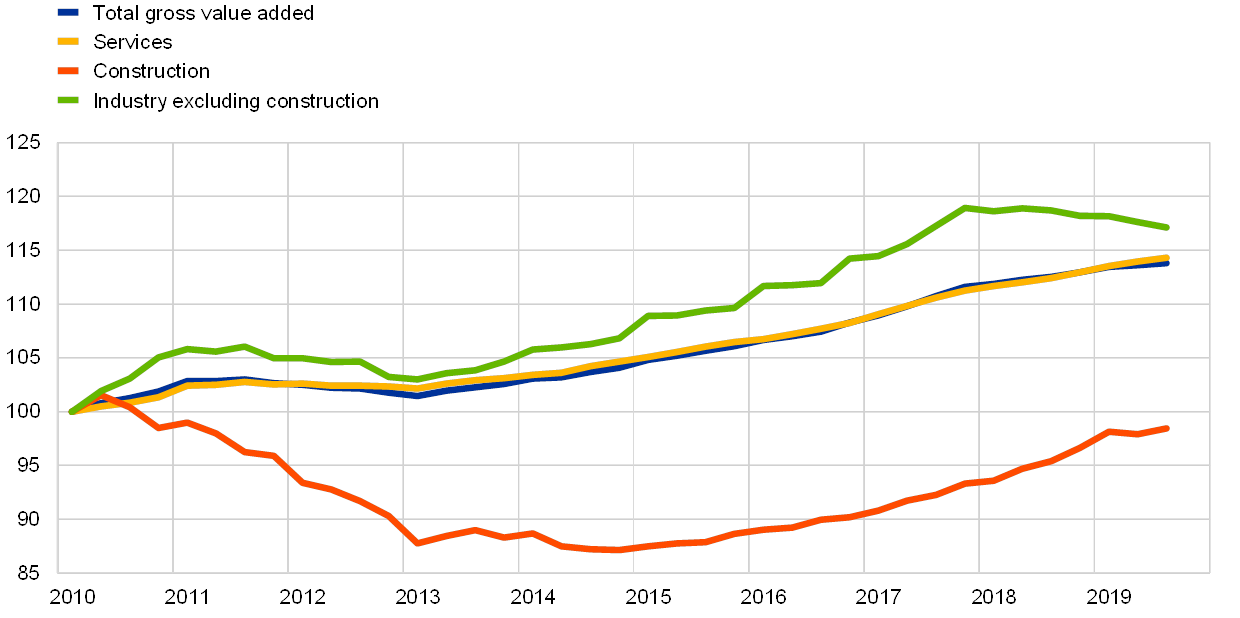

Output growth in 2019 was driven by the services and construction sectors, which showed continued resilience on the back of robust euro area domestic demand. Activity in the euro area industrial sector weakened further (see Chart 6). This reflected negative repercussions from the weakness in foreign demand. There were by contrast only limited signs that weaker external demand affected services in 2019.[3]

Chart 6

Euro area real gross value added by economic activity

(index: Q1 2010 = 100)

Sources: Eurostat and ECB calculations.

Note: The latest observations are for the third quarter of 2019.

In 2019 domestic demand continued to contribute positively to euro area growth, amid favourable financing conditions and improving labour markets. Private consumption, alongside consumer sentiment, remained resilient in 2019 (see Box 1). Household spending was supported by rising employment and wages, which resulted in growing aggregate labour income. Following the gradual slowdown starting in 2018, business investment remained moderate in 2019. A much less dynamic external environment and heightened global uncertainty weighed on firms’ investment decisions. In spite of this and the modest developments in corporate profitability and declining capacity utilisation, business investment continued to contribute positively to economic growth, supported by favourable financing conditions. Growth in investment in intellectual property products, which tends to be volatile, was particularly strong.[4] At the same time, there was a slowdown in housing investment after its strong and prolonged recovery of previous years, alongside a moderation of the momentum in euro area housing markets. This deceleration mainly reflected increasingly binding constraints on housing supply – especially in terms of labour shortages, regulatory bottlenecks and the debt-reduction process – which limited growth in the construction sector in the course of 2019.

Box 1

Consumption and household sentiment remained resilient

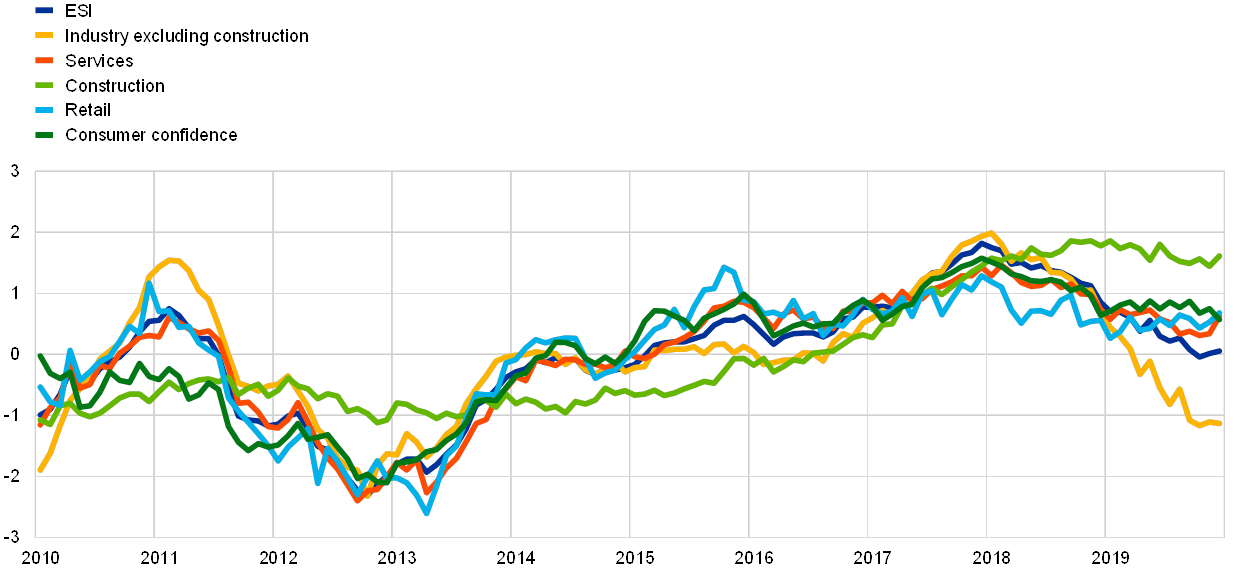

In 2019 the services and retail sectors remained resilient overall as the euro area economy slowed, despite some moderation in growth in these sectors. Private consumption represents an important part of demand in the services and retail sectors. With this in mind, this box looks more closely at consumer confidence in the euro area, considering the reasons for the relative resilience of consumer spending.

Sentiment among consumers stabilised and held up better than in other sectors

The economic slowdown in 2019 predominantly reflected weaker international trade alongside elevated levels of global uncertainty, which in turn mostly weighed on the euro area industrial sector. Meanwhile, the services and retail sectors remained resilient, despite some moderation. This is evident in Chart A, which displays sentiment in various sectors of the euro area economy. The European Commission’s Economic Sentiment Indicator (ESI) is a weighted average of confidence in industry excluding construction (with a weight of 40%), services (30%), construction (5%), the retail sector (5%) and households (20%). As can be seen, the slowdown in the more domestically oriented sectors (i.e. construction, services, retail and households) has been much less pronounced than in industry.

Chart A

Euro area confidence – sectoral breakdown

(standardised percentage balances)

Sources: European Commission and ECB calculations.

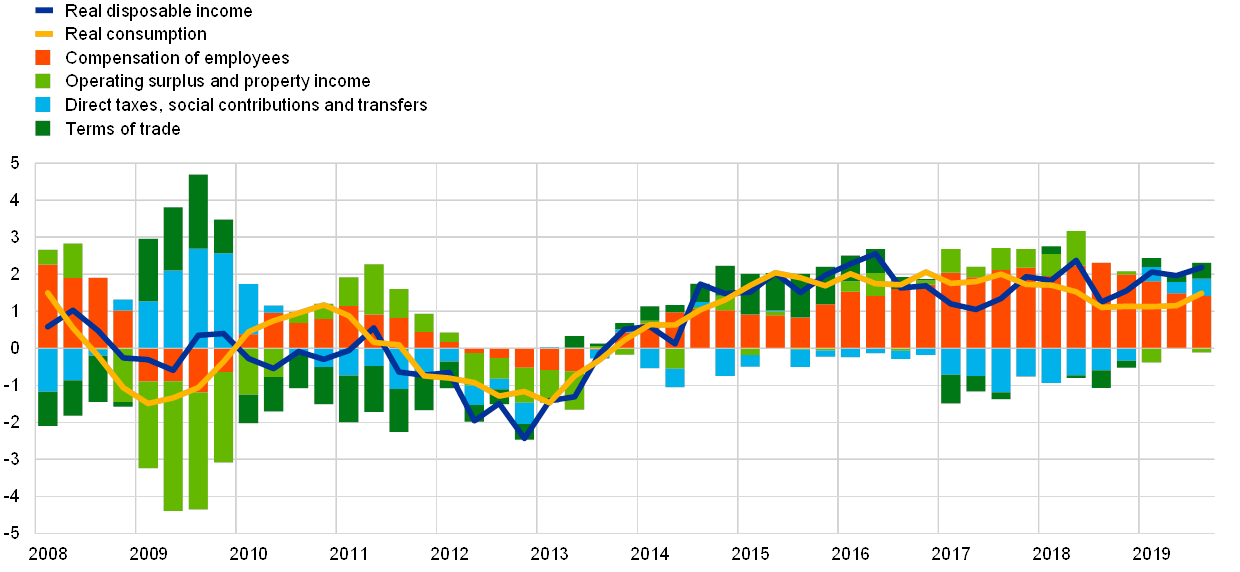

Private consumption remained resilient overall in 2019

Private consumption growth in 2019 was held up by continued growth in real disposable income, which in turn was supported by a resilient labour market. Labour income benefited both from continued increases in wages and further, although slowing, employment gains. In addition, direct taxes, social contributions and transfers are overall likely to have had a small positive impact on income growth, in contrast with 2018 when they still dampened income growth (see Chart B). However, the contribution from the operating surplus and property income, which tend to be closely linked to economic activity, turned slightly negative in 2019, having been positive since 2015.

Chart B

Real private consumption and disposable income

(annual percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

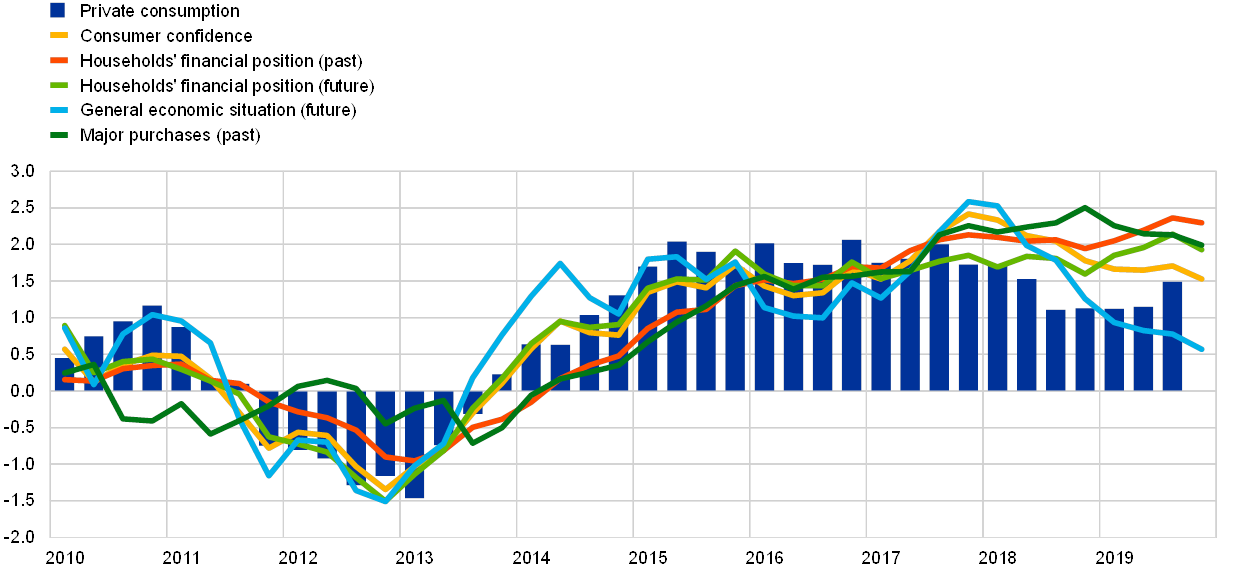

Drivers of consumer confidence

The Commission’s Consumer Confidence Index is the result of averaging four sub-indices relating to perceptions of past financial and economic developments as well as expectations regarding future developments 12 months ahead (see Chart C).[5] While one sub-index relates to the assessment of the overall economic situation in the country, the others deal with households’ financial situation. Looking at the developments in these sub-indices, it can be seen that households had a relatively more benign view of their personal situation, mainly reflecting the ongoing resilience of the labour market, which has largely shielded household income from the economic slowdown.

Chart C

Private consumption and consumer confidence

(annual percentage changes; standardised percentage balances)

Sources: Eurostat, European Commission and ECB calculations.

Note: The survey data have been standardised with the average and standard deviation of annual growth in private consumption since 2010.

Robust labour market developments, in conjunction with rising wages, combined with favourable financing conditions and households’ improving financial position, largely explain why euro area consumer confidence remained elevated in 2019, supporting private consumption. In the context of resilient domestic demand alongside weak foreign demand, the ECB continues to closely monitor incoming data in order to assess the risk of negative spillovers from the external sector to the domestic sector.

The external sector contributed negatively in net terms to euro area output in 2019. With the exception of exports to the United States, which expanded at a slower pace, the decline was broad-based, owing mainly to the bleak performance of exports of capital goods and cars. Intra-euro area trade declined as well, with the slump concentrated in trade in intermediate goods, reflecting the impairment of euro area production chains.

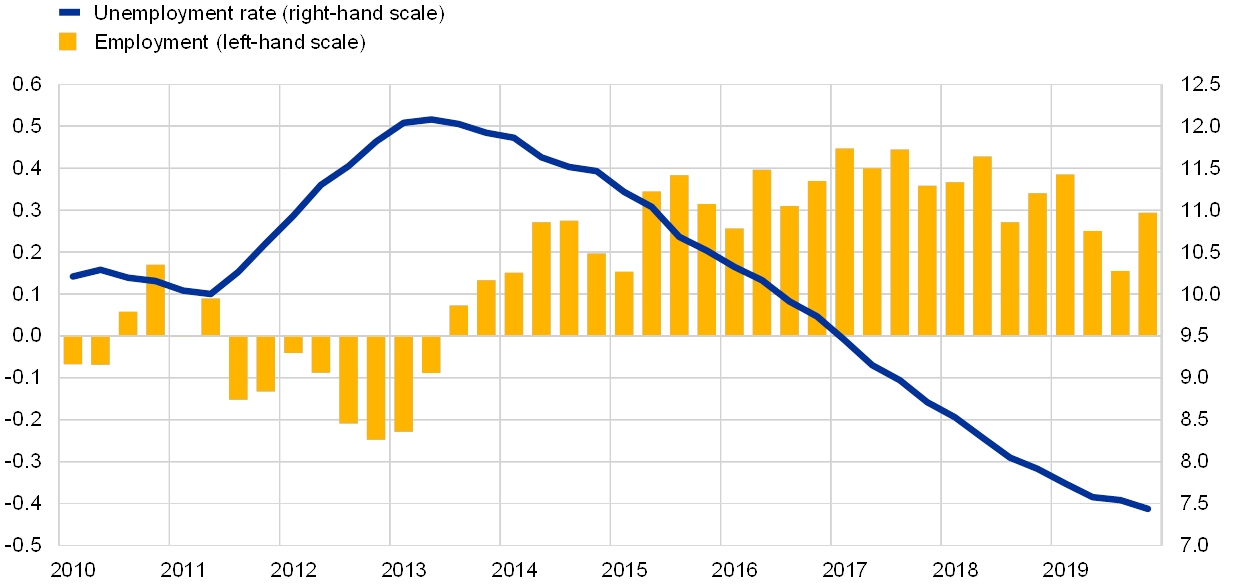

Euro area labour markets continued to improve, while productivity growth decelerated substantially

Euro area labour markets continued to improve in 2019

Euro area labour markets continued to improve in 2019 (see Chart 7). This improvement was a key element supporting economic activity in 2019.

According to an analysis based on synthetic labour market indicators, the level of labour market activity was close to its precrisis peak in the second quarter of 2019. In addition, labour market momentum remained above its long-term average, although it has recently moderated somewhat.[6] The good labour market performance occurred against the background of continued increases in labour supply, which in part reflected the higher participation of older workers resulting from previous reforms that increased the statutory pension age.[7]

Chart 7

Labour market indicators

(percentage of the labour force; quarter-on-quarter growth rate; seasonally adjusted)

Source: Eurostat.

Note: The latest observations are for the fourth quarter of 2019.

Employment increased by 1.2% in 2019, which is a robust rate when comparing with GDP growth developments. The growth of labour productivity per person employed was 0.0% in 2019, following 0.4% in 2018.[8] In spite of the increases in labour supply, the unemployment rate continued to decline and reached 7.6% in 2019, close to the rate observed in 2007. However, the dispersion of unemployment rates across euro area countries remained high.

The digital economy requires monitoring

Digitalisation is having an effect on variables which are relevant for monetary policy

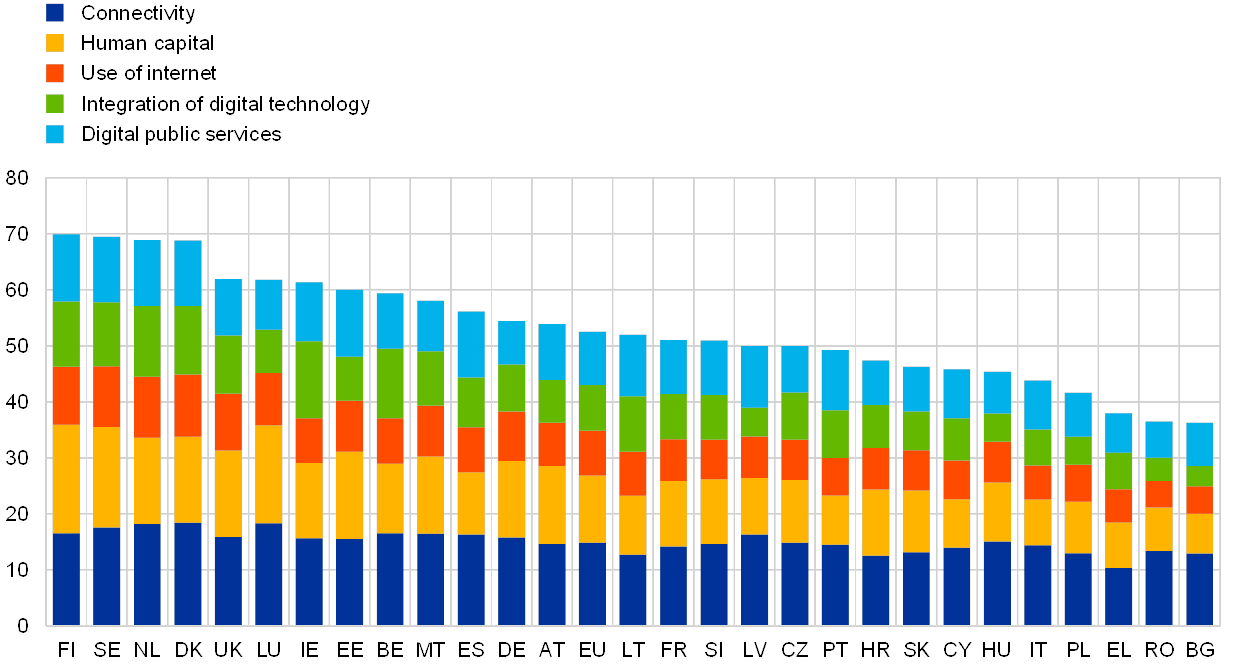

According to the literature, digitalisation is having an impact on a number of key economic variables which are relevant for monetary policy. The empirical evidence on the effects of digitalisation suggests that they may be pushing up activity and productivity, while its overall effect on inflation is not clear yet.[9] In 2019 the degree of digitalisation of the EU economies ranged from around 40 for the least digital to around 70 for the most digital economies, according to the European Commission’s Digital Economy and Society Index (DESI) (see Chart 8). While the EU economies scored broadly similarly in terms of connectivity, they displayed less homogeneity in terms of human capital, use of the internet, integration of digital technology and digital public services.

Chart 8

Digital Economy and Society Index for 2019

Source: European Commission.

Structural policies should help to address key challenges

The implementation of policy recommendations remained lacklustre in 2019

The implementation of structural policies in euro area countries needs to be substantially stepped up to boost euro area productivity and growth potential, reduce structural unemployment and increase the resilience of the economy. This includes structural policies to improve the functioning of labour markets, increase competition in product and factor markets and enhance the business environment.[10] Furthermore, structural policies are needed to help address the current and future challenges posed, for example, by population ageing, digitalisation and climate change. The country-specific recommendations (CSRs) provide policy recommendations tailored to an individual country on how to enhance economic growth and resilience. The CSRs are endorsed by Member States in the European Council. In February 2019 the European Commission concluded that 95% of the policy recommendations had either not been implemented or, at best, had been implemented to “some” extent.[11]

A mildly expansionary fiscal stance provided some support to economic activity

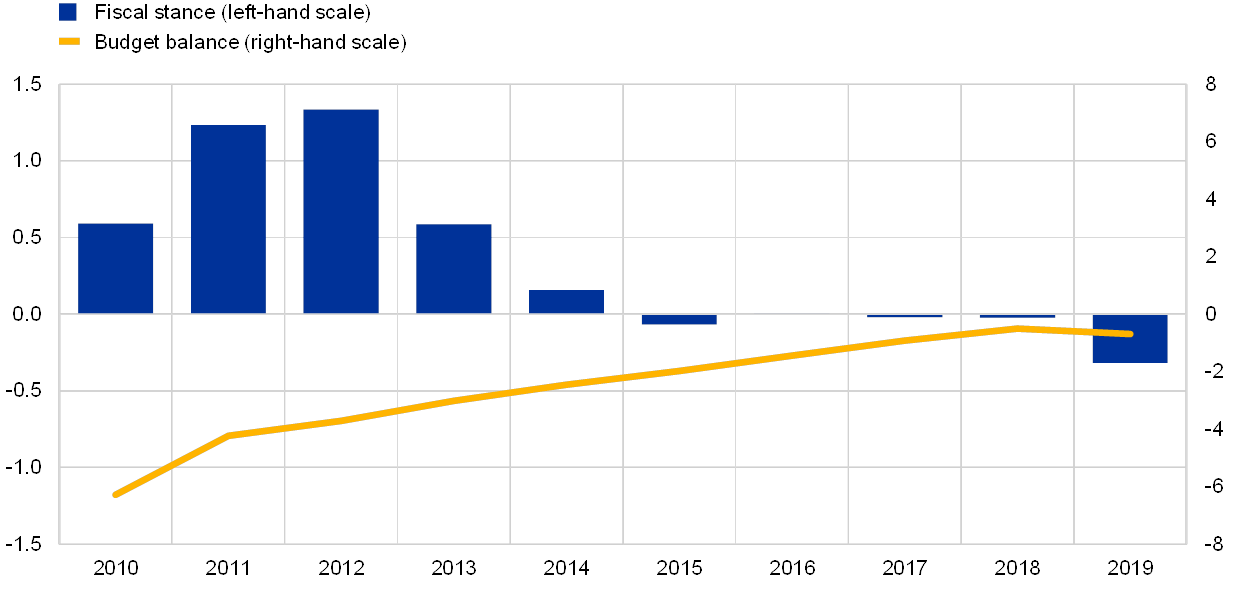

The euro area general government deficit ratio increased slightly on account of a mildly expansionary fiscal stance

After having been broadly neutral for five years, the euro area fiscal stance[12] turned expansionary, albeit mildly, in 2019 (see Chart 9). The loosening of the stance provided support to economic activity in the euro area. It reflected expansionary policy measures which were implemented in some large member countries, mostly cuts to direct taxes as well as public expenditure increases. Based on the December 2019 Eurosystem staff macroeconomic projections, the euro area general government deficit ratio increased slightly in 2019 to 0.7% of GDP. The decline in the budget balance reflected the more expansionary fiscal stance, which was partly offset by savings in interest payments, while the contribution from the cyclical position remained broadly unchanged.

Chart 9

General government balance and fiscal stance

(percentage of GDP)

Sources: Eurostat and ECB calculations.

The aggregate general government debt-to-GDP ratio in the euro area continued to decline in 2019 and reached 84.5% of GDP at the end of the year. However, debt-to-GDP ratios remained high in a number of countries. The reduction in the aggregate debt ratio was supported by favourable interest rate-growth differentials and positive, but declining primary balances. While there were no euro area countries under the corrective arm of the Stability and Growth Pact (SGP) at the end of 2019, the European Commission assessed that the 2020 draft budgetary plans of eight euro area countries, many of which had debt ratios of close to or above 100% of GDP, posed a risk of non-compliance with the requirements under the SGP.[13]

1.3 Inflationary pressures remained muted

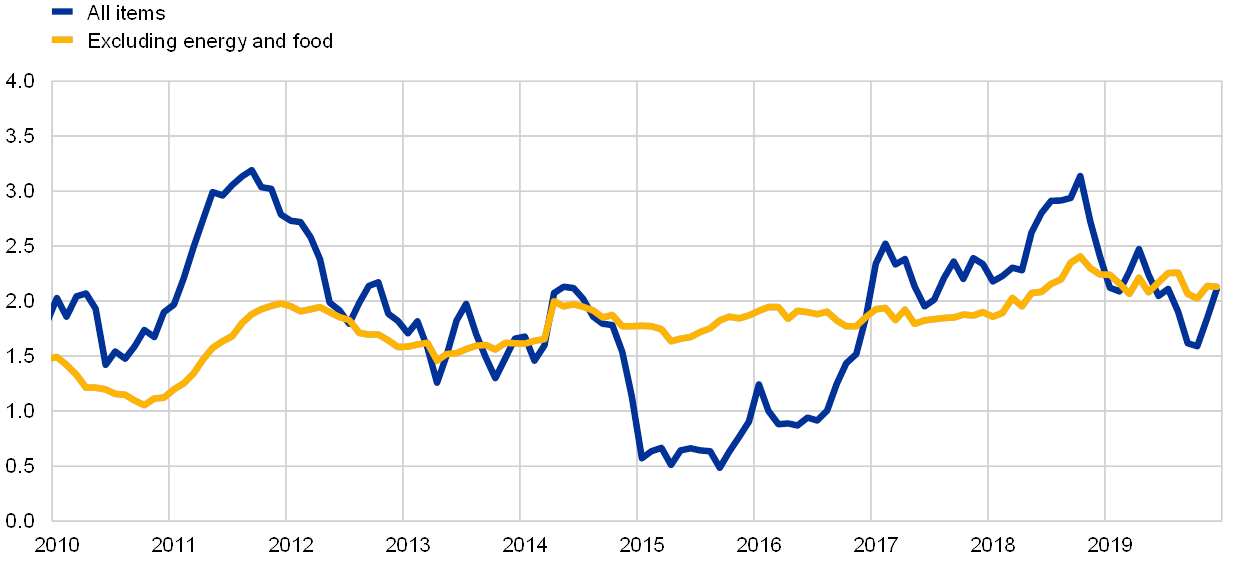

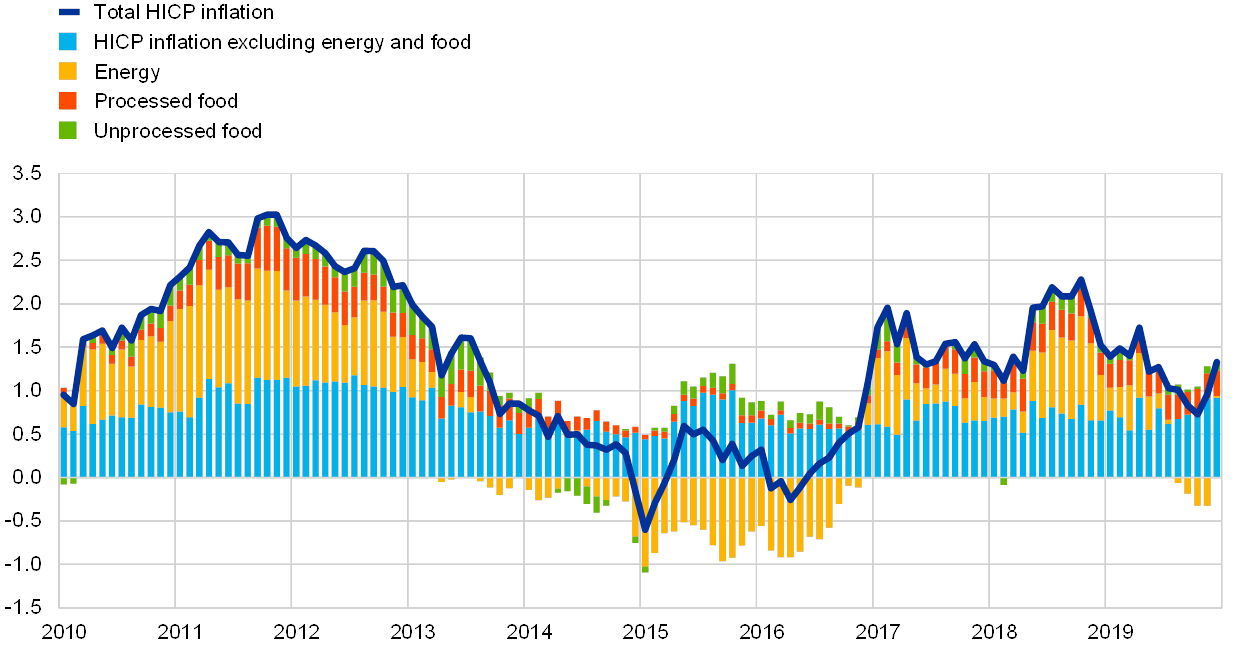

Headline inflation in the euro area stood at 1.2% on average in 2019, down from 1.8% in 2018.[14] This decline essentially reflected lower contributions from the two more volatile inflation components, energy and food. HICP inflation excluding energy and food, one measure of underlying inflation, remained at subdued rates, averaging 1.0% in 2019 as in 2018 and 2017, despite an increase towards the end of the year (see Chart 10).

Chart 10

HICP inflation and contributions by components

(annual percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

The decline in headline inflation was driven by lower energy and food inflation, while underlying inflation remained subdued

Developments in energy inflation were largely responsible for the decline in average headline inflation in 2019 compared with 2018. The contribution of total food inflation to headline HICP inflation declined to 0.3 percentage points in 2019, from 0.4 percentage points in 2018. Developments in total food inflation within the year were largely determined by those in the volatile unprocessed food component. Processed food inflation hovered around 1.9% in 2019, which was slightly below the 2018 average. Increases in producer prices for consumer food and in food commodity prices (as captured by EU farm-gate prices), two drivers of processed food prices, suggest that such cost increases were not fully passed through to food prices at the consumer level in a context of high competition.

HICP inflation excluding energy and food, like other measures of underlying inflation, moved broadly sideways during most of the year and remained below its historical average, despite the mild increase at the end of 2019. Box 2 below discusses the relationship between underlying inflation and economic activity, as well as broader economic developments since the global financial crisis. Weak developments in both non-energy industrial goods and services inflation contributed to subdued HICP inflation excluding energy and food. Non-energy industrial goods inflation averaged 0.3% in 2019, unchanged from 2018 and the average since 2015. Indicators of price pressures at different stages of the pricing chain show that the annual rate of change of producer prices for non-food consumer goods remained broadly stable through the year, but was substantially higher than its average since 2015. This suggests that some of the cost increases have been absorbed at the retailer stage. In addition, unlike in 2018, the average annual rate of change of import prices for non-food consumer goods was positive in 2019, reflecting, among other factors, the depreciation of the euro. Services inflation displayed some volatility linked to price developments in travel-related services that resulted from a statistical effect.[15] Looking through this monthly volatility, services inflation moved sideways and, on average, stood at 1.5% in 2019, unchanged from 2018 and only marginally higher than the average since 2015. Overall, the increases in services prices, which mostly include a large labour cost content, continued to lag behind wage growth.

Box 2

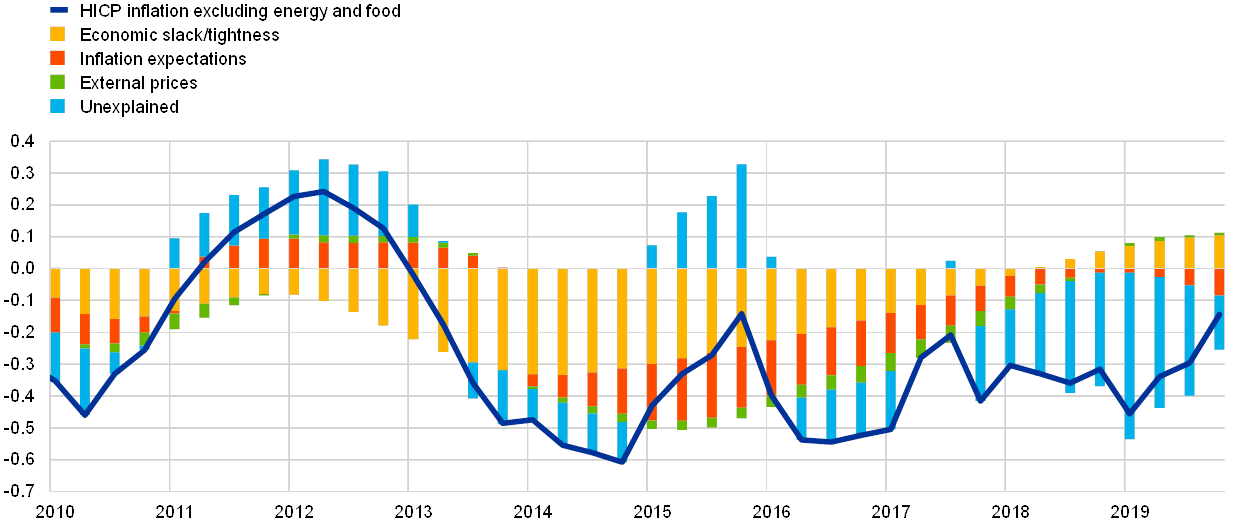

The euro area Phillips curve and its interpretation of recent inflation developments

Since 2013 HICP inflation excluding energy and food has consistently remained below its historical average. While this could initially be explained by large amounts of economic slack and other factors dampening inflationary pressures, the more recent weakness is difficult to account for within a standard Phillips curve framework, as visible from the unexplained component of the decomposition of inflation developments in Chart A. This has prompted renewed scrutiny of this fundamental economic relationship.[16]

Chart A

Phillips curve-based decomposition of underlying inflation

(annual percentage changes and percentage point contributions; all values in terms of deviations from their averages since 1999)

Source: ECB calculations.

Notes: The bars show average contributions across a large number of model specifications (see Bobeica, E. and Sokol, A., “Drivers of underlying inflation in the euro area over time: a Phillips curve perspective”, Economic Bulletin, Issue 4, ECB, 2019). Contributions are derived as in Yellen, J. L., “Inflation Dynamics and Monetary Policy”, speech at the Philip Gamble Memorial Lecture, University of Massachusetts, Amherst, 24 September 2015.

Inflation determinants within the Phillips curve framework

In essence, the Phillips curve captures the notion that economic activity and the associated degree of tightness in goods and labour markets should influence inflation. High levels of economic slack weighed on inflation in the aftermath of the global financial crisis. The euro area also experienced a second recession between 2011 and 2013, and the weakness in underlying inflation starting in early 2013 is well explained by this factor. However, even if by 2018 many measures of economic activity and slack had returned to average levels, and some measures even started to show signs of excess demand, underlying inflation has remained below its average since 1999 (1.3%).

Besides economic activity, other factors, such as inflation expectations and external prices, are also crucial to understand inflation developments. Many factors can influence economic agents’ inflation expectations: recent inflation developments (and in particular energy price movements) typically influence expectations at short horizons, while genuine concerns about the credibility and attainability of a central bank’s inflation objective can weigh on longer-term expectations, although these factors are difficult to disentangle empirically.[17] Both market and survey-based measures of inflation expectations weakened over the period 2014-17, which is reflected in their negative contributions to underlying inflation over the same period.[18] More recently, survey measures of longer-term inflation expectations for the euro area, notably those from the ECB Survey of Professional Forecasters, have shown signs of a softening. However, the drag on inflation attributable to these recent developments is smaller.

Finally, measures of external prices, such as oil and broader import price indices, can be an important factor explaining firms’ pricing decisions, and thus developments in inflation, over and above what might already be captured by slack and inflation expectations. While external prices, and especially energy prices, are typically quickly reflected in headline inflation, their indirect effects on underlying inflation appear to have been limited in recent years.[19] Overall, developments in underlying inflation appear to be explained reasonably well by standard factors up to 2017, but the more recent weakness is difficult to account for within this framework.

One possible explanation could be that standard measures of economic slack do not capture all developments in economic activity relevant for inflation. In that spirit, Jarociński and Lenza (2018)[20] derive a measure of economic slack designed explicitly to forecast inflation. Such a measure would imply a much larger amount of economic slack than a more standard measure of the output gap.

Overall, the Phillips curve remains a central element for the interpretation and communication of inflation developments, but it needs to be complemented with information from other tools and approaches, especially in the light of recent developments in underlying inflation.

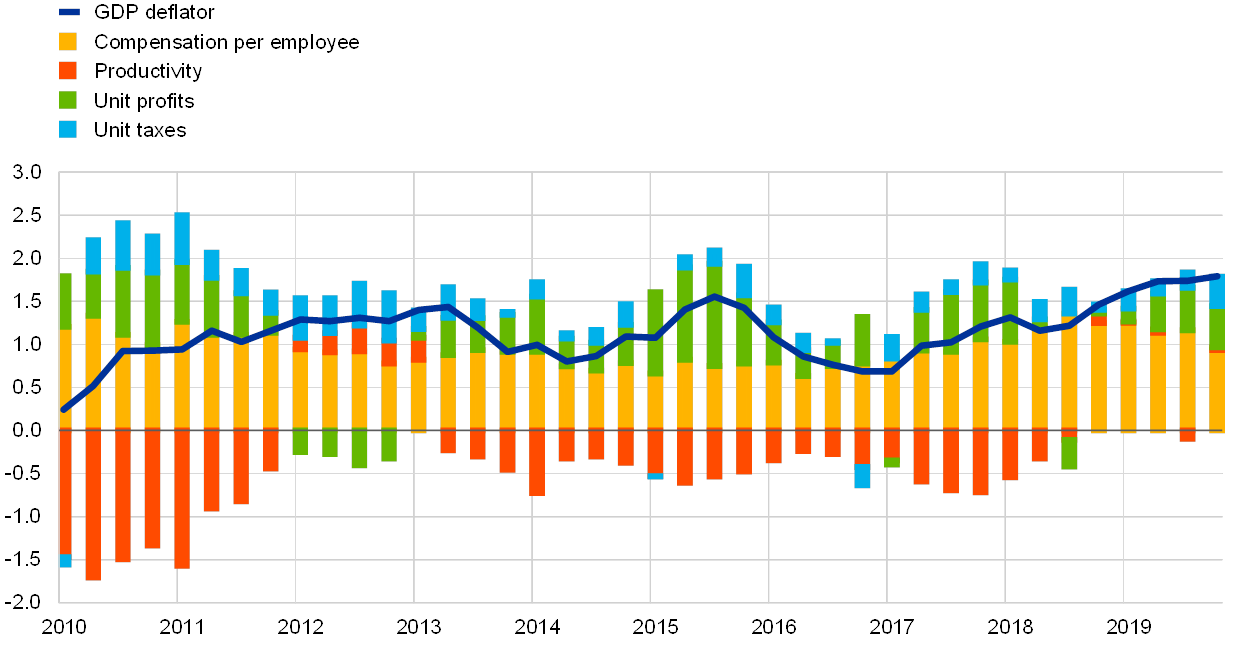

Domestic cost pressures, as measured by the growth in the GDP deflator, increased on average in 2019, at a rate above the average level of 2018 and the average since 2015 (see Chart 11). The annual growth in compensation per employee maintained its robust pace in 2019, standing at 2.0% on average, slightly below the 2018 average, but above its average since 2015. Compensation per employee growth was tempered by developments in social security contributions,[21] while growth in wages and salaries increased in 2019 compared with 2018, in line with the further reduction in the unemployment rate and despite the moderation in economic growth in the euro area (see Section 1.2 above). The robust average growth in compensation per employee implied, however, an increase in unit labour cost growth as productivity stagnated in 2019. In addition to the higher unit labour cost growth, the increase in the GDP deflator growth also reflected a rebound in profit developments (measured in terms of the gross operating surplus), which had weakened noticeably in the course of 2018. Given that productivity moved sideways in 2019, the profit rebound in 2019 most likely reflected improvements in the terms of trade and developments in economic sectors that were less affected by the global activity and trade slowdown.[22] These were for instance the construction and real estate sectors, which also displayed a high rate of growth in their value added deflators, going up to 4.6% on average in 2019 in the case of construction.

Chart 11

Breakdown of the GDP deflator

(annual percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

Longer-term inflation expectations declined in the course of 2019. Expectations for inflation five years ahead from the ECB Survey of Professional Forecasters eased to 1.7% in the fourth quarter of 2019 from 1.9% in the fourth quarter of 2018. Market-based measures of longer-term inflation expectations, such as the five-year inflation-linked swap rate five years ahead, also declined. However, they stabilised – albeit at still low levels – towards the end of the year.

1.4 Favourable financing conditions continued to support credit and money growth

In 2019 euro area financial markets were driven primarily by the effects of slowing economic activity amid persistently low inflation, uncertainty related to political factors inducing risk-off sentiment in some periods of the year, and further monetary policy easing. Both money market rates and longer-term bond yields declined significantly, while equity prices increased overall, supported by lower discount rates. The external financing flows of non-financial corporations (NFCs) broadly stabilised in 2019 at a level significantly below their latest peak in 2017, but borrowing from banks and the issuance of debt securities remained solid, supported by favourable financing conditions, and net issuance of unlisted shares was robust, underpinned by an increased number of mergers and acquisitions. The ongoing expansion of bank credit to the private sector, coupled with the low opportunity costs of holding M3, helped to sustain the growth rates of broad money. Favourable financing conditions reflected the ECB’s accommodative monetary policy stance and the capacity of the banking system to pass this accommodation on to the lending rates faced by firms and households. Increasing valuations of financial asset and real estate holdings supported household wealth, which in turn underpinned private consumption growth.

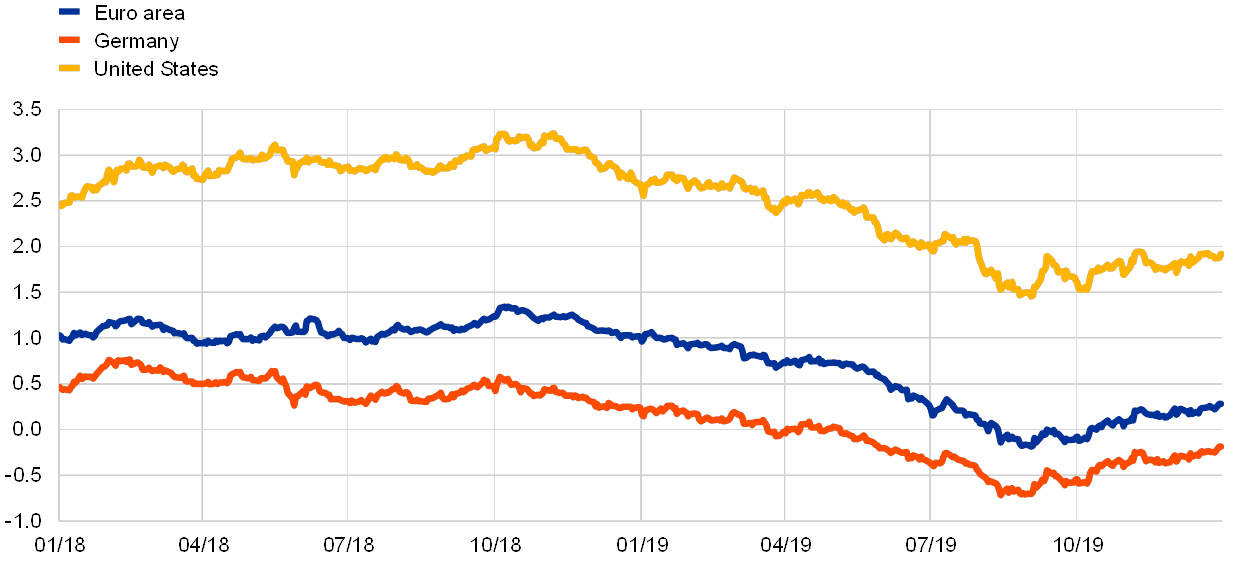

Euro area government bond yields declined significantly in 2019, albeit recovering since September

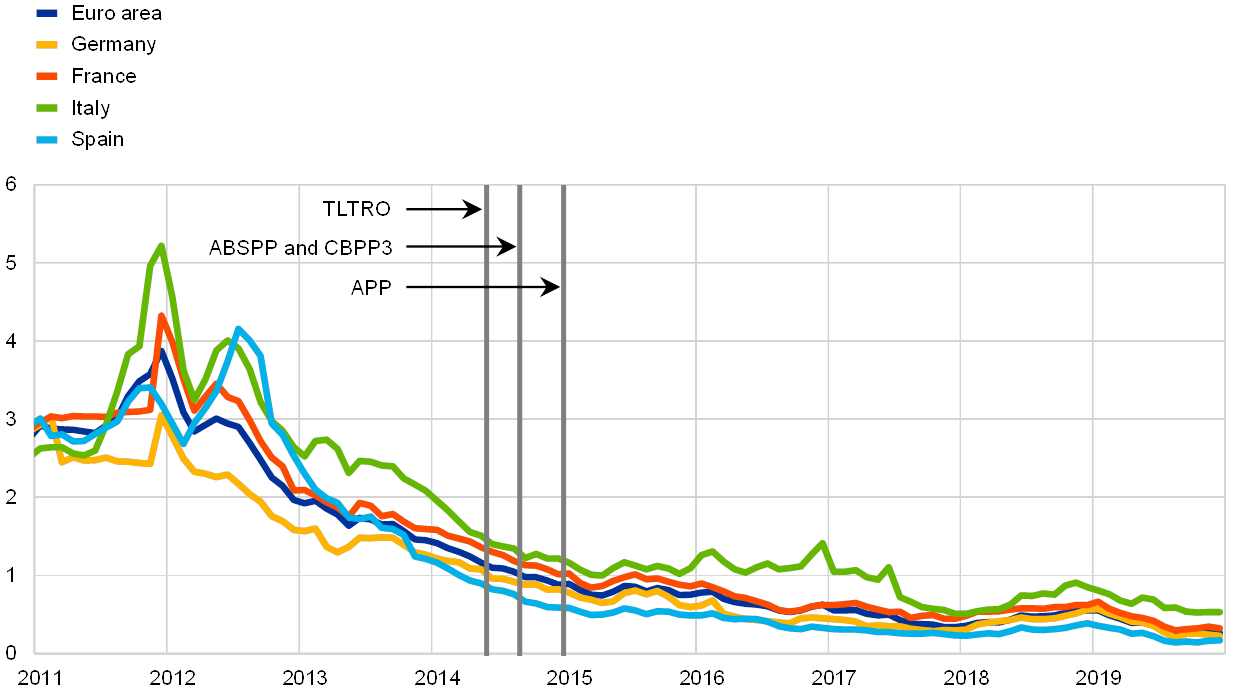

Euro area government bond yields declined significantly in 2019, with long-term yields reaching negative levels during the summer. This decline reflected growing concerns about the extent and duration of the slowdown in euro area economic activity and its impact on inflation developments. Monetary policy accommodation in the United States, heightened global risk sentiment connected to the US-China trade tensions and Brexit, and growing expectations in financial markets about a further easing of monetary policy by the ECB also contributed to lower risk-free rates in the euro area. After the ECB’s monetary policy easing package was announced in September, somewhat more positive euro area macroeconomic data releases and some stabilisation in global risk sentiment contributed to a gradual recovery of euro area government bond yields. This notwithstanding, the euro area GDP-weighted average of ten-year sovereign bond yields stood at 0.28% on 31 December 2019, which was 74 basis points lower than its level on 1 January 2019. The spread of euro area countries’ ten-year sovereign bond yields against the German ten-year Bund yield declined, significantly so for some countries, owing to lower fiscal policy uncertainty.

Chart 12

Ten-year sovereign bond yields in the euro area, the United States and Germany

(percentages per annum; daily data)

Sources: Bloomberg, Thomson Reuters Datastream and ECB calculations.

Notes: The euro area data refer to the ten-year GDP-weighted average of sovereign bond yields. The latest observations are for 31 December 2019.

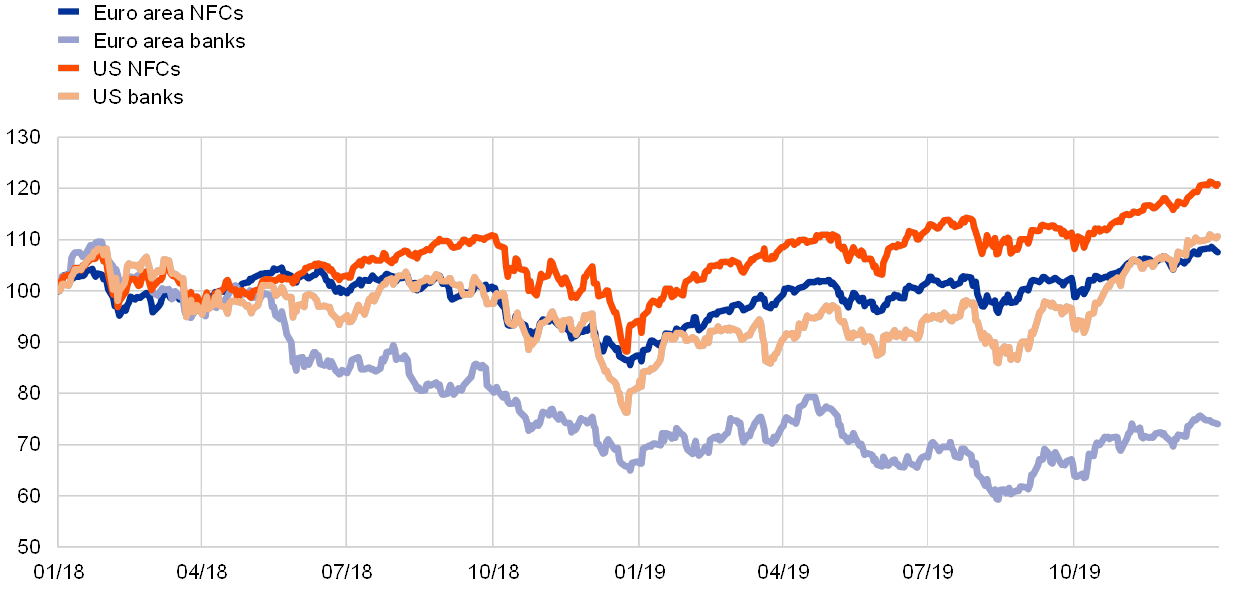

Euro area equity prices increased on account of lower discount rates

In 2019 euro area equity prices increased significantly. The broad index for euro area NFC equity prices increased by 20.7% over the course of 2019, while an index of euro area bank equity prices rose by 9.7% (see Chart 13). Lower discount rates were the main supporting factor behind the equity price developments, while earnings expectations remained weak and movements in risk premia – primarily related to evolving developments in the US-China trade dispute and Brexit negotiations – weighed on equities.

Chart 13

Equity market indices in the euro area and the United States

(index: 1 January 2018 = 100)

Source: Thomson Reuters Datastream.

Notes: The EURO STOXX banks index and the Datastream market index for NFCs are shown for the euro area; the S&P banks index and the Datastream market index for NFCs are shown for the United States. The latest observations are for 31 December 2019.

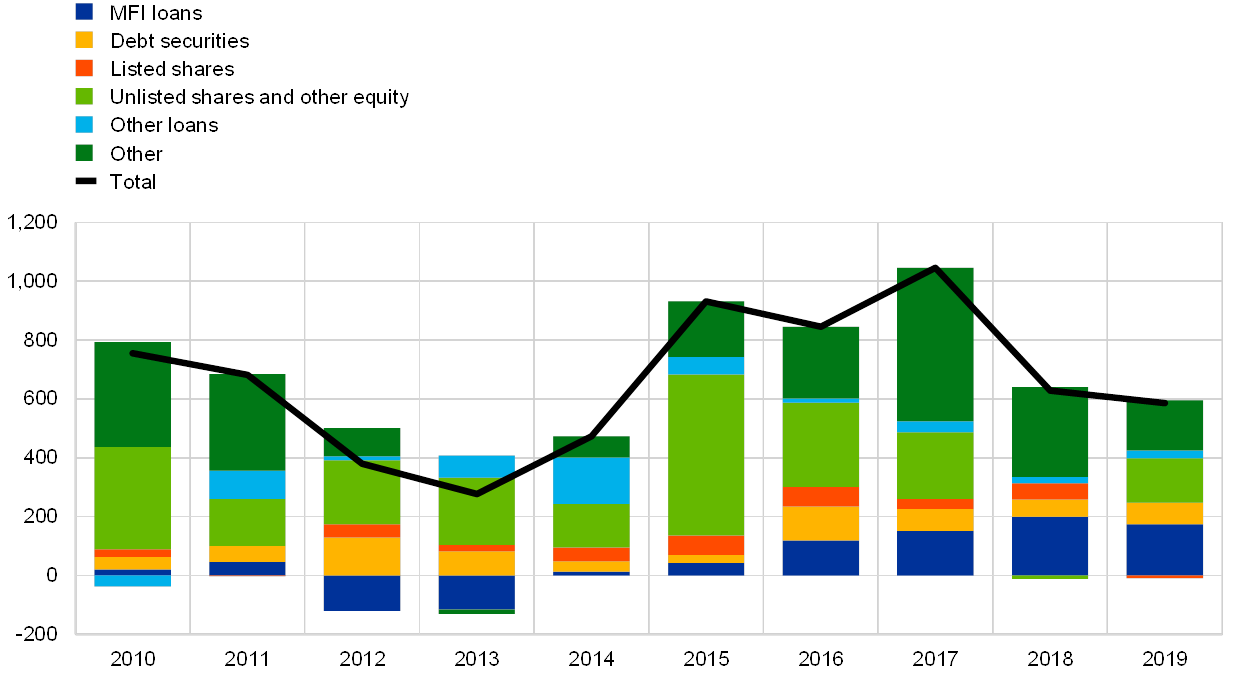

NFCs’ borrowing from banks and issuance of debt securities were solid

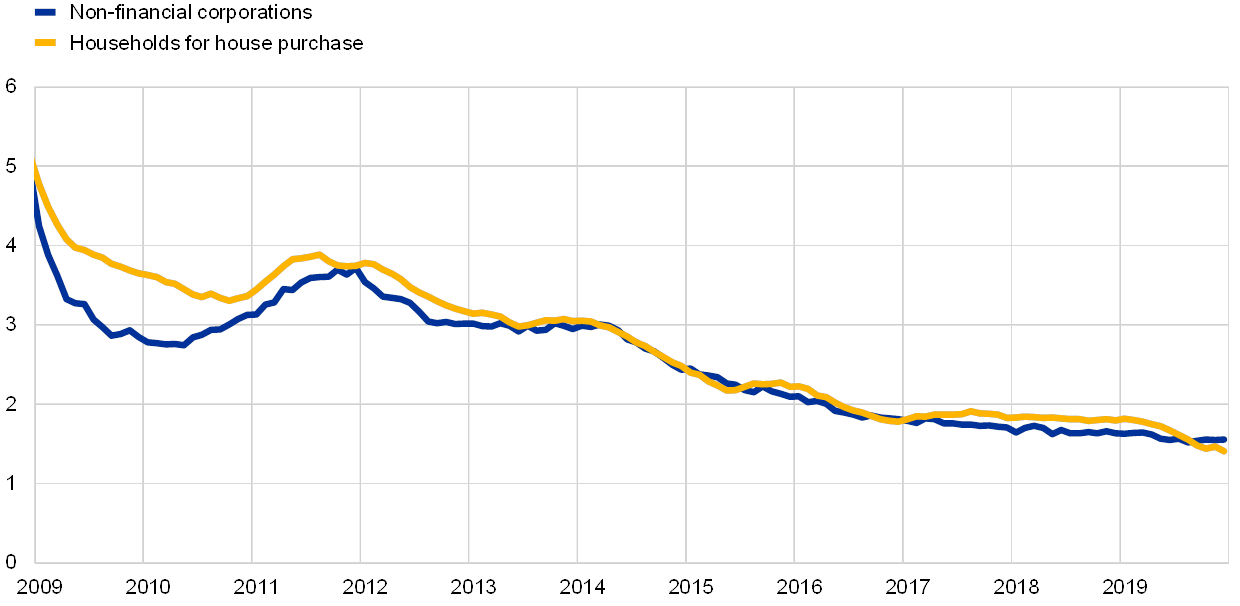

The external financing flows of NFCs broadly stabilised in 2019, significantly below their latest peak in 2017 (see Chart 14). This said, the growth of borrowing from banks and the issuance of debt securities remained solid, supported by favourable financing conditions, and net issuance of unlisted shares was robust, underpinned by an increase in the number of mergers and acquisitions. By contrast, there was moderation in the other sources of financing (including inter-company loans and trade credit) and a decline in the net issuance of listed shares (which reflected the elevated cost of equity compared with other sources of funding). Bank lending rates declined further – broadly in line with the evolution of market rates – to new historical lows during 2019.

Further monetary policy easing by the ECB during 2019 was transmitted to financing conditions, which became more favourable. This was partly due to the fact that some of the measures introduced in 2019 – such as the third series of targeted longer-term refinancing operations (TLTRO III) and the two-tier system for reserve remuneration – were geared towards supporting bank intermediation capacity (see Section 2.1). At the same time, the banking system made further progress in balance sheet repair, in terms of boosting capital positions and improving asset quality.

Chart 14

Net flows of external financing to non-financial corporations in the euro area

(annual flows; EUR billions)

Sources: Eurostat and ECB.

Notes: “Other loans” include loans from non-MFIs (other financial institutions, insurance corporations and pension funds) and from the rest of the world. MFI (monetary financial institution) and non-MFI loans are adjusted for loan sales and securitisation. “Other” is the difference between the total and the instruments listed in the chart. It includes inter-company loans and trade credit. The latest observations are for the third quarter of 2019.

Household wealth was supported by increased valuations of real and financial assets

Households’ net wealth increased strongly in the first three quarters of 2019, thereby underpinning private consumption. Despite a moderating momentum in housing markets, net wealth benefited from further house price increases, which resulted in significant valuation gains on households’ real estate holdings. In addition, households also registered notable valuation gains on their financial asset holdings. Furthermore, rising house prices and favourable financing conditions contributed to the continued gradual upward trend in the annual growth rate of bank loans to households for house purchase. Household gross indebtedness – measured as a percentage of household nominal gross disposable income – remained at levels well above its average pre-crisis level.

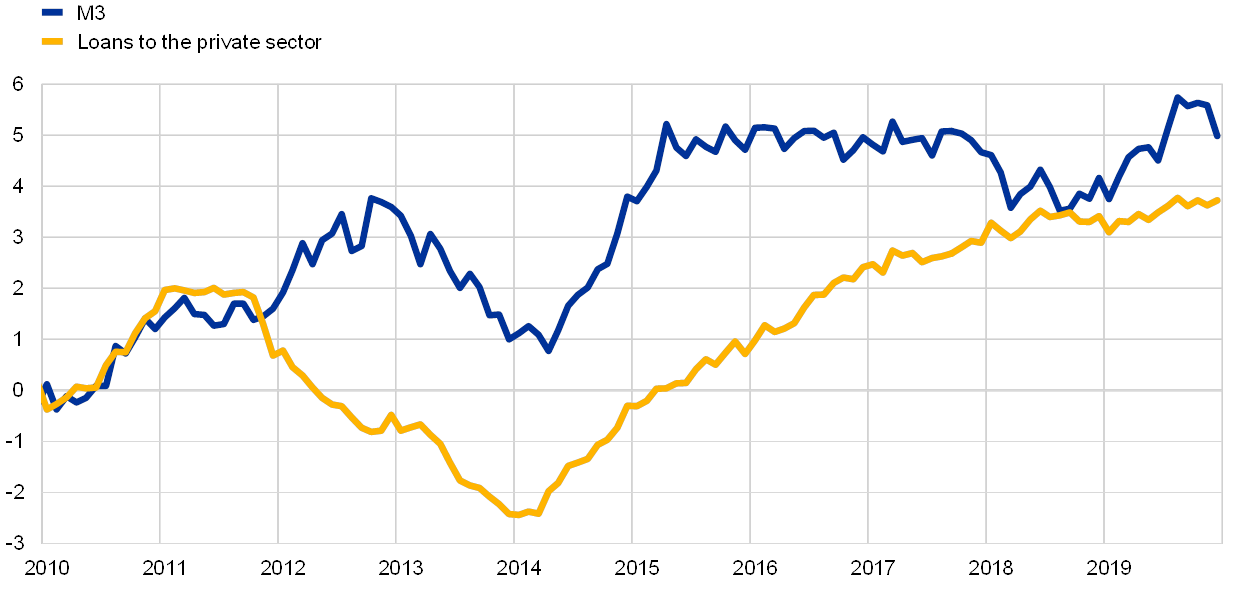

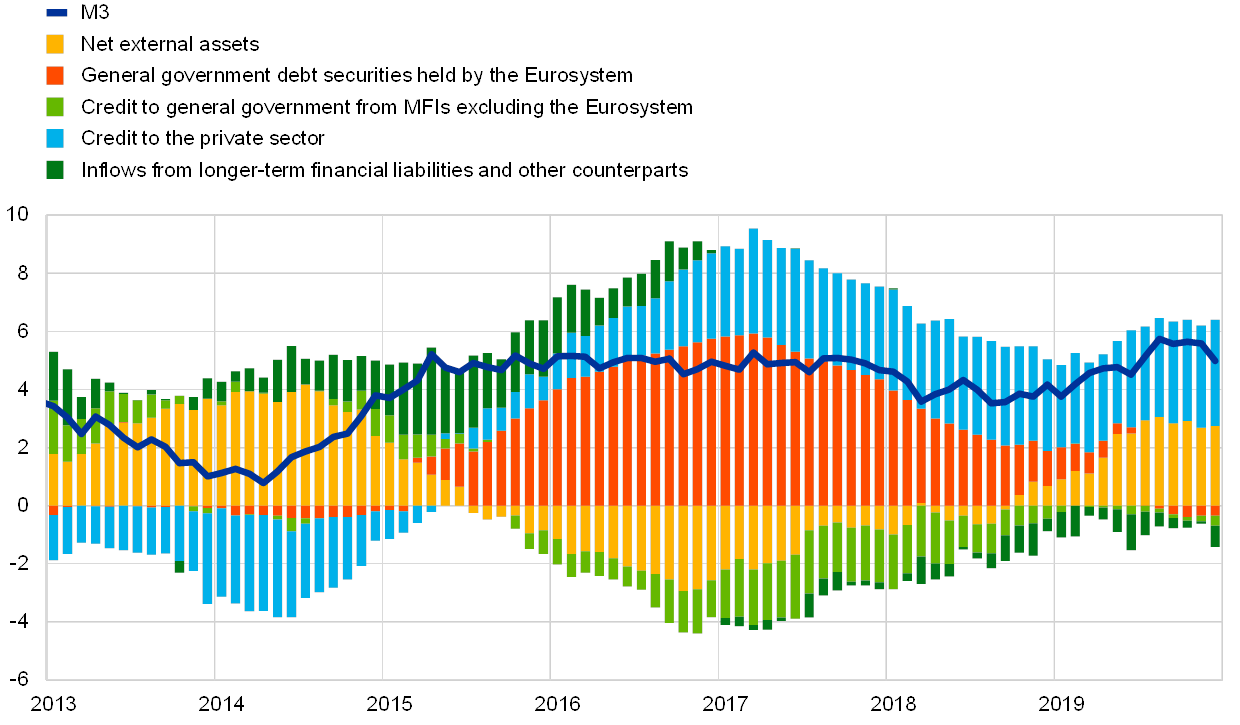

M3 and credit growth recovered in 2019

Overall, bank lending to the private sector was solid, with its annual growth rate (adjusted for loan sales, securitisation and notional cash pooling) increasing to 3.7% in December 2019, from 3.4% in December 2018. Credit growth remained the largest driver of broad money growth (see the blue parts of the bars in Chart 16). At the same time, external monetary flows made an increasing contribution to M3 dynamics (see the yellow parts of the bars in Chart 16). Annual M3 growth thus recovered in 2019 (see Chart 15). While the termination of net purchases under the asset purchase programme at the end of 2018 had a dampening impact on M3 growth (see the red parts of the bars in Chart 16), their resumption in November 2019 only had a limited influence on broad money growth in 2019.

Chart 15

M3 and loans to the private sector

(annual percentage changes)

Source: ECB.

Notes: Loans are adjusted for loan sales, securitisation and notional cash pooling. The latest observations are for December 2019.

Chart 16

M3 and its counterparts

(annual percentage changes; contributions in percentage points; adjusted for seasonal and calendar effects)

Source: ECB.

Notes: Credit to the private sector includes MFI loans to the private sector and MFI holdings of securities issued by the euro area non-MFI private sector. As such, it also covers the Eurosystem’s purchases of non-MFI debt securities under the corporate sector purchase programme. The latest observations are for December 2019.

Most of M3 growth reflected increased holdings of overnight deposits

From an instrument perspective, overnight deposits continued to be the main driver of M3 growth, given the low opportunity cost of holding liquid deposits in an environment characterised by very low interest rates and a flat yield curve. Growth in overnight deposits reflected the strong expansion of overnight deposits held by both households and NFCs. As a result, the narrow monetary aggregate M1, which comprises currency in circulation and overnight deposits, continued to grow at a robust pace.

Against the background of a weakening of the euro area economy, more persistent downside risks and an inflation outlook that continued to fall short of the medium-term inflation aim of the Governing Council of the ECB, the Governing Council provided three successive rounds of additional monetary accommodation over the course of 2019. These successive interventions underlined the Governing Council’s determination to act as appropriate to support the return of inflation to a sustained convergence path towards its medium-term aim. In view of the time needed for all of the measures to exert their full impact on the euro area economy, the Governing Council continued to closely monitor inflation developments and the pass-through of the unfolding monetary policy measures, while it remained ready to adjust all of its instruments, as appropriate, to ensure that inflation moved towards its aim in a sustained manner, in line with its commitment to symmetry. At the end of 2019 monetary policy-related assets accounted for 70% of the total assets on the Eurosystem’s balance sheet. The size of the balance sheet stabilised at €4.7 trillion in 2019, in line with the level reached at the end of the previous year. Risks related to the large balance sheet continued to be mitigated by the ECB’s risk management framework.

2.1 A first round of monetary policy measures to keep policy accommodation ample amid rising external headwinds

Following the deterioration in the economic outlook at the end of 2018, incoming information in early 2019 continued to be weaker than expected owing to softer external demand and some country and sector-specific factors, pointing to less buoyant near-term growth momentum than previously anticipated. At the same time, there was considerable uncertainty as to whether the factors slowing down euro area growth would be transitory or longer lasting, and hence to what extent slower growth in the short term would affect the medium-term growth outlook. Against this background, the Governing Council recognised that the risks surrounding the euro area growth outlook had moved to the downside on account of the persistence of uncertainties related to geopolitical factors and the threat of protectionism, vulnerabilities in emerging markets and financial market volatility. The Governing Council highlighted that monetary policy needed to remain patient, prudent and persistent. While supportive financing conditions, favourable labour market dynamics and rising wage growth would continue to underpin the euro area expansion and gradually rising inflationary pressures, the Governing Council reiterated the need for significant monetary policy stimulus to ensure a continued sustained convergence of inflation to levels below, but close to, 2% over the medium term.

The more sluggish economic momentum slowed the adjustment of inflation towards the medium-term aim, prompting the introduction of a first policy package

Incoming economic data during the spring continued to be weak, pointing to a sizeable moderation in the pace of the economic expansion that would extend into 2019. In particular, activity in the manufacturing sector had decelerated markedly, mainly on account of external headwinds, as global growth and trade dynamics remained weak. The more sluggish economic momentum was slowing the adjustment of inflation towards the Governing Council’s medium-term aim.

In response to a material downgrade of the growth and inflation outlook, the Governing Council therefore decided at its March meeting on a package of policy measures to provide additional monetary accommodation. This would support the further build-up of domestic price pressures and headline inflation developments over the medium term and increase the resilience of the euro area economy in an environment of global uncertainties. In particular, the Governing Council decided on the following measures. First, it decided to shift out the calendar-based leg of its forward guidance on policy rates. More specifically, the Governing Council expected to keep the key ECB interest rates at their present levels at least through the end of 2019, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels in line with its medium-term aim. Second, it reiterated the intention to continue reinvesting, in full, the principal payments from maturing securities purchased under the asset purchase programme (APP) for an extended period of time past the date when it started raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation. Given the link between the forward guidance on policy rates and reinvestments, the expected reinvestment horizon was automatically shifted out, reinforcing the guidance on policy rates while underlining the Governing Council’s determination to act as appropriate. Third, in addition to the change in policy rate guidance, a new series of quarterly targeted longer-term refinancing operations (TLTRO III) was announced. These operations would start in September 2019 and end in March 2021, and each operation would have a maturity of two years. The new series of TLTROs aimed to preserve favourable bank lending conditions to keep bank credit flowing to customers on affordable terms. In turn, a healthy credit flow to the private sector underpinned the consumption and investment plans of households and businesses, helping the economy to grow and supporting the adjustment of inflation towards the Governing Council’s medium-term aim. Fourth, the Governing Council decided to continue to conduct the Eurosystem’s lending operations as fixed rate tender procedures with full allotment for as long as necessary, and at least until the end of the reserve maintenance period starting in March 2021.

Following the announcement of the new series of TLTROs, at its next monetary policy meeting, the Governing Council communicated that the precise terms of the TLTRO III series would be announced at one of the forthcoming meetings. In particular, the pricing of the TLTRO III operations would take into account a thorough assessment of the bank-based transmission channel of monetary policy, as well as further developments in the economic outlook. In addition, the Governing Council, bearing in mind that the negative interest rate environment would prevail for longer than previously anticipated, noted that in the context of its regular assessment, it would consider whether the preservation of the favourable implications of negative interest rates for the economy would require the mitigation of their possible side effects, if any, on bank intermediation.

A second round of additional monetary policy accommodation and deteriorating confidence in the inflation outlook

By mid-year, the incoming information indicated that global headwinds continued to weigh on the euro area outlook

By mid-year, the incoming information indicated that global headwinds, relating in particular to the ongoing weakness in global trade and more pervasive and prolonged uncertainties in the external environment, continued to weigh on the euro area outlook. These factors were weighing in particular on the euro area manufacturing sector. Furthermore, HICP inflation decreased further, mainly on account of temporary factors, and measures of underlying inflation continued to move sideways.

In the light of the prolongation of uncertainties and their implications for the inflation outlook, the Governing Council recognised the need to adjust the monetary policy stance for the second time in 2019 and provide additional monetary accommodation for inflation to remain on a sustained path towards its medium-term aim. Therefore, the Governing Council decided at its June meeting to strengthen its forward guidance on policy rates by shifting out further the calendar-based element of the forward guidance. More specifically, the Governing Council stated that it expected the key ECB interest rates to remain at their present levels at least through the first half of 2020, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to its medium-term aim. In addition, it reiterated its forward guidance on reinvestments. Finally, the Governing Council also decided on the pricing of the TLTRO III series. The interest rate in each operation would be set at a level that was 10 basis points above the average rate applied in the Eurosystem’s main refinancing operations. For banks whose eligible net lending exceeded a benchmark, the rate applied in TLTRO III would be lower, and could be as low as the average interest rate on the deposit facility plus 10 basis points. It was noted that this pricing struck a reasonable balance between acknowledging the sound developments in bank lending, on the one hand, and the importance of preserving the accommodative stance, on the other hand.

Over the course of the summer, softening global growth dynamics and weak international trade continued to weigh on the euro area outlook. In addition, the prolonged presence of uncertainties continued to dampen business sentiment, especially in the manufacturing sector. Price developments, in turn, remained muted, while measures of underlying inflation continued to move sideways. Market-based measures of longer-term inflation expectations had stagnated at the historical lows reached after the June meeting, while surveys signalled a marked fall in longer-term expectations.

The Governing Council noted that realised and projected inflation rates had been persistently below levels that were in line with its aim

Against this background, the Governing Council, at its July meeting, noted that inflation rates (both realised and projected) had been persistently below levels that were in line with its aim. Moreover, the Governing Council viewed the symmetry of its medium-term inflation aim as an important element to bolster the achievement of a sustained adjustment in inflation to its aim. It was hence seen as important for the Governing Council to demonstrate its determination and capacity to act and to be prepared to ease the policy stance further by adjusting all of its instruments, as appropriate, to achieve its inflation aim. At the same time, the Governing Council stated that if the medium-term inflation outlook continued to fall short of its aim, it was determined to act, in line with its commitment to symmetry in the inflation aim. Hence, in this context, the Governing Council decided to reintroduce a so-called easing bias in its forward guidance on policy rates by stating that it expected to keep the key ECB interest rates at present or lower levels. In addition, it tasked the relevant Eurosystem Committees with examining options, including ways to reinforce the forward guidance on policy rates, mitigating measures (e.g. the design of a tiered system for reserve remuneration) and possibilities for the size and composition of potential new net asset purchases. These announcements paved the way for the potential implementation of a comprehensive policy package at the Governing Council’s next monetary policy meeting if the inflation outlook failed to improve in line with its aim.

A third round of policy accommodation with a comprehensive package of measures in response to persistently low inflation rates

The September 2019 ECB staff macroeconomic projections showed a further downgrade of the inflation outlook. Overall, the Governing Council was confronted with a protracted slowdown in the euro area economy, persistent downside risks and an inflation outlook that continued to fall short of its medium-term inflation aim. In particular, successive and significant downward revisions to the inflation outlook had brought projected inflation in 2021 down from 1.8% in the December 2018 projections to 1.5% in the September 2019 projections. The further downgrade of the inflation outlook – despite the fact that the financial conditions embedded in the projections already reflected substantial expectations of additional policy easing – meant that inflation was projected to move further away from levels that the Governing Council considered to be consistent with its inflation aim. Measures of underlying inflation remained muted and indicators of inflation expectations remained at low levels. Against this background, the Governing Council agreed that a third round of easing of the monetary policy stance was warranted to support the return of inflation to a sustained convergence path towards its inflation aim. The Governing Council therefore took the following decisions in September:

A comprehensive policy response was deemed necessary to support the return of inflation to a sustained convergence path towards the medium-term aim

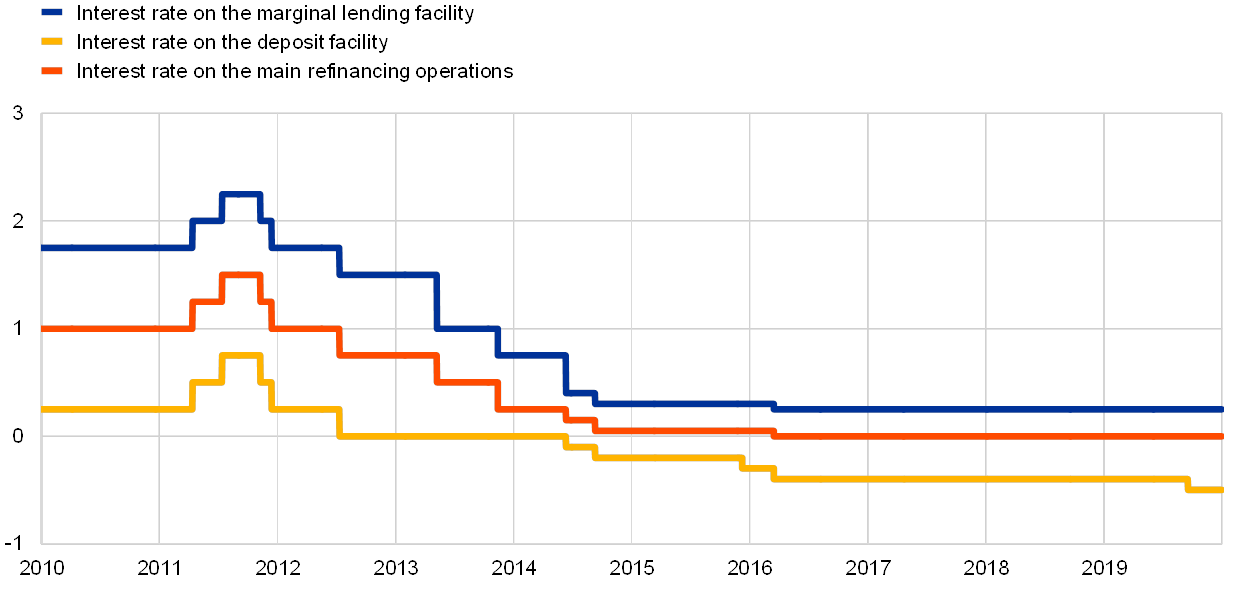

First, it decided to reduce the deposit facility rate, by 10 basis points, to -0.50% (see Chart 17). The reduction in the deposit facility rate was accompanied by a reformulation of the Governing Council’s forward guidance on the expected path of policy rates. It now expected that the key ECB interest rates would remain at their present or lower levels until the inflation outlook was seen to robustly converge to a level sufficiently close to, but below, 2% within the projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

Chart 17

Key ECB interest rates

(percentages per annum)

Source: ECB.

Note: The latest observations are for 31 December 2019.

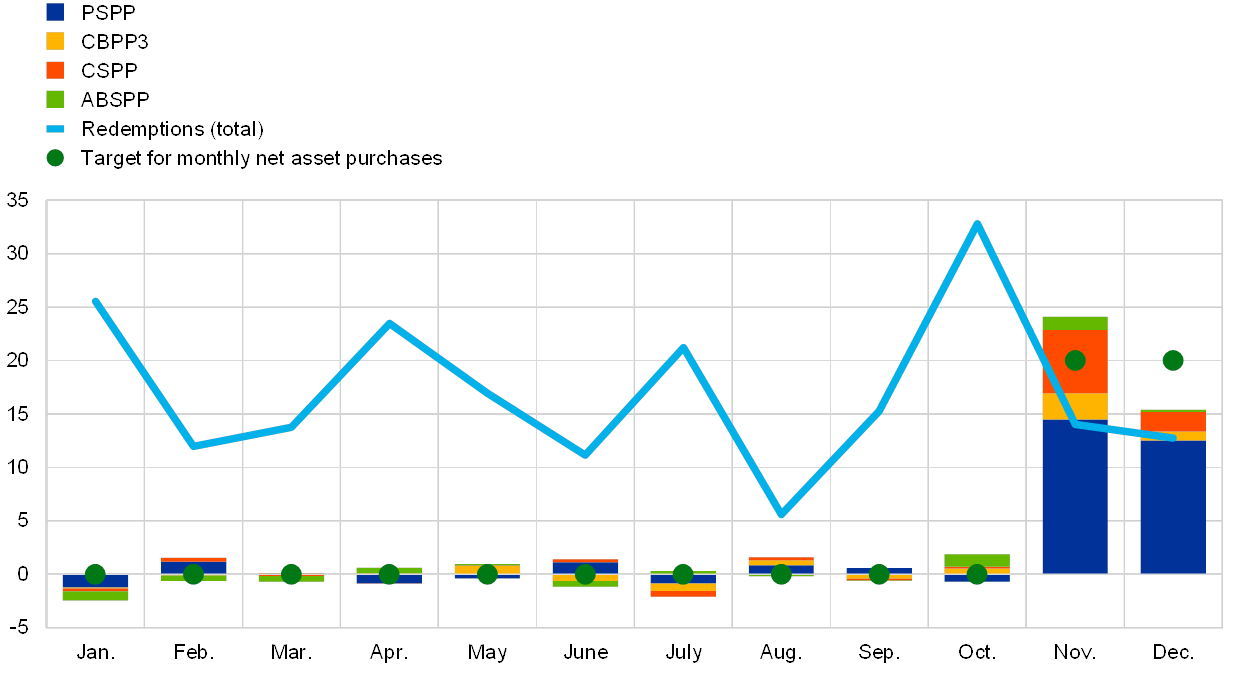

Second, it decided to restart net purchases of bonds under the APP at a monthly pace of €20 billion as from 1 November (see Chart 18) with the expectation to terminate net purchases shortly before the Governing Council started to raise the key ECB interest rates. The Governing Council also reiterated that it would continue to reinvest, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when it started to raise the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Chart 18

Monthly net asset purchases and total redemptions under the APP in 2019

(EUR billions)

Source: ECB.

Notes: Monthly net purchases at book value and monthly redemption amounts. During the reinvestment phase, the Eurosystem adheres to the principle of market neutrality via smooth and flexible implementation. To this end, the reinvestments of principal redemptions are distributed over the year to allow for a regular and balanced market presence. Furthermore, additional net asset purchases can also be distributed to neighbouring months to cater for expected lower market activity in particular months (e.g. December). As a consequence, monthly net purchases are not exactly equal to the monthly target for net asset purchases. The latest observations are for 31 December 2019.

Third, it decided to recalibrate the third series of TLTROs with a more attractive interest rate for participating banks (banks outperforming a minimum lending benchmark could now borrow at a rate that could be as low as the average interest rate on the deposit facility prevailing over the life of the operation) and a longer maturity (three years instead of two years). The more favourable TLTRO conditions sought to preserve favourable bank lending conditions, ensure the smooth transmission of monetary policy and further support the accommodative stance of monetary policy.

Finally, to safeguard the bank-based transmission of monetary policy, a two-tier system for reserve remuneration was introduced which exempts a fraction of banks’ excess cash reserves from the negative deposit facility rate.

All elements of the package of measures decided upon at the Governing Council’s September monetary policy meeting were designed to complement each other in providing monetary stimulus and support the convergence of inflation towards the Governing Council’s aim. The reduction in the deposit facility rate and the strengthened state-contingent forward guidance served to anchor short to medium-term interest rates, which are important for pricing loans to firms in the euro area. The renewed net asset purchases and the expected reinvestment horizon anchored medium to longer-term interest rates, which are important for pricing mortgage loans to households. TLTRO III was recalibrated to preserve favourable bank lending conditions, ensure a smooth transmission of monetary policy and incentivise banks to keep credit flowing to their customers. Finally, the two-tier system for reserve remuneration was designed to alleviate the direct cost of negative interest rates for banks in order to support the bank-based transmission of monetary policy. Consequently, easier market funding conditions continued to be passed through to the lending conditions faced by firms and households.

Monitoring inflation developments in the light of a tentative stabilisation in the growth outlook, while standing ready to act

By year-end, following three rounds of monetary policy easing over the course of 2019, measures of underlying inflation remained generally subdued and euro area growth dynamics continued to be weak, although there were some initial signs of stabilisation in the growth slowdown and of a mild increase in underlying inflation in line with previous projections. In the light of these developments and given that it took time for all of the measures to exert their full impact, the Governing Council announced at its December meeting that it was closely monitoring inflation developments and the pass-through of the unfolding monetary policy measures taken in September to the economy. In any case, it underlined that it continued to stand ready to adjust all of its instruments, as appropriate, to ensure that inflation moved towards its aim in a sustained manner, in line with its commitment to symmetry.

In the light of the persistent uncertainties and downside risks, substantial additional monetary policy accommodation was implemented over the course of 2019. All elements of the measures taken continued to work together and contributed to a further decline in bank funding costs (see Chart 19). Banks’ very favourable financing conditions were passed on to the wider economy, with borrowing conditions for firms and households standing at – or close to – their historical lows (see Chart 20). All decisions taken over the course of 2019 contributed to the ample degree of monetary policy accommodation introduced since 2014 and continued to support the improvement in the economic performance of the euro area.

Chart 19

Composite cost of debt financing for banks

(composite cost of deposit and unsecured market-based debt financing; percentages per annum)

Sources: ECB, Markit iBoxx and ECB calculations.

Notes: The composite cost of deposits is calculated as an average of new business rates on overnight deposits, deposits with an agreed maturity and deposits redeemable at notice, weighted by their corresponding outstanding amounts. The latest observations are for 31 December 2019.

Chart 20

Composite bank lending rates for non-financial corporations and households

(percentages per annum)

Source: ECB.

Notes: Composite bank lending rates are calculated by aggregating short and long-term rates using a 24-month moving average of new business volumes. The latest observations are for 31 December 2019.

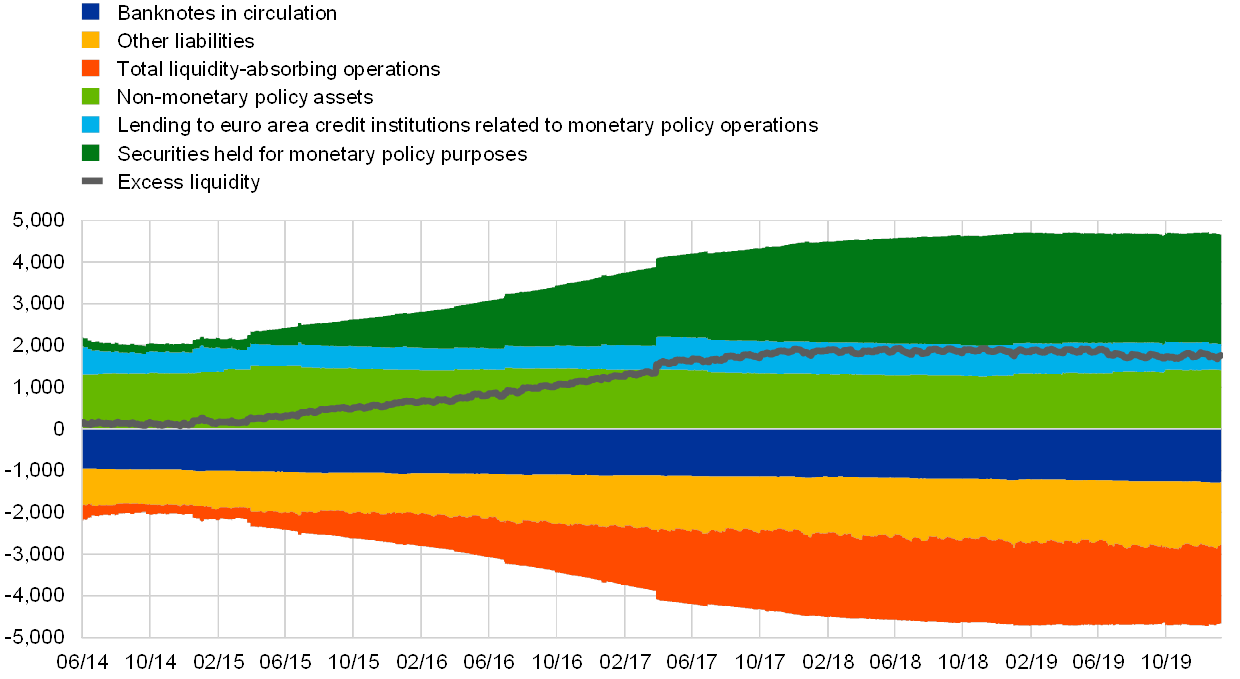

2.2 Eurosystem balance sheet dynamics amid the restart of net asset purchases

The size of the Eurosystem’s balance sheet remained unchanged in 2019

Since the onset of the global financial crisis in 2007-08, the Eurosystem has taken a variety of standard as well as non-standard monetary policy measures, which have had a direct impact on the size and composition of the Eurosystem’s balance sheet over time. The non-standard measures have included refinancing operations to provide funding to counterparties with an initial maturity of up to four years, as well as purchases of assets issued by private and public entities (under the APP). In December 2018 the Eurosystem ended net asset purchases under the APP and, in 2019, it fully reinvested the principal payments from maturing securities. As of 1 November 2019 the Eurosystem restarted net asset purchases at an average monthly pace of €20 billion. At the end of 2019 the size of the Eurosystem’s balance sheet stood at €4.7 trillion, unchanged from the level at the end of 2018.

At the end of 2019 monetary policy-related assets amounted to €3.3 trillion, accounting for 70% of the total assets on the Eurosystem’s balance sheet (down from 72% at the end of 2018). These monetary policy-related assets include loans to euro area credit institutions, which accounted for 13% of total assets (down from 16% at the end of 2018), and assets purchased for monetary policy purposes, which represented around 56% of total assets (unchanged from the end of 2018) (see Chart 21). Other financial assets on the balance sheet mainly consisted of foreign currency and gold held by the Eurosystem and euro-denominated non-monetary policy portfolios.

On the liabilities side, the overall amount of counterparties’ reserve holdings and recourse to the deposit facility remained broadly unchanged at €2 trillion and represented 39% of the liabilities side at the end of 2019, unchanged from the end of 2018. After the announcement of the two-tier system for reserve remuneration, effective from 30 October 2019, counterparties’ cash holdings with the Eurosystem significantly shifted towards reserve holdings at the expense of recourse to the deposit facility. At the end of 2019 the latter represented 15% of counterparties’ overall cash holdings with the Eurosystem, down from 34% at the end of 2018. Banknotes in circulation grew in line with the historical growth trend and accounted for 28% of liabilities at the end of 2019, up from 26% at the end of 2018. Other liabilities, including capital and revaluation accounts, accounted for 34%, unchanged from the end of 2018 (see Chart 21).

Chart 21

Evolution of the Eurosystem’s consolidated balance sheet

(EUR billions)

Source: ECB.

Notes: Positive figures refer to assets and negative figures to liabilities. The line for excess liquidity is presented as a positive figure, although it refers to the sum of the following liability items: current account holdings in excess of reserve requirements and recourse to the deposit facility.

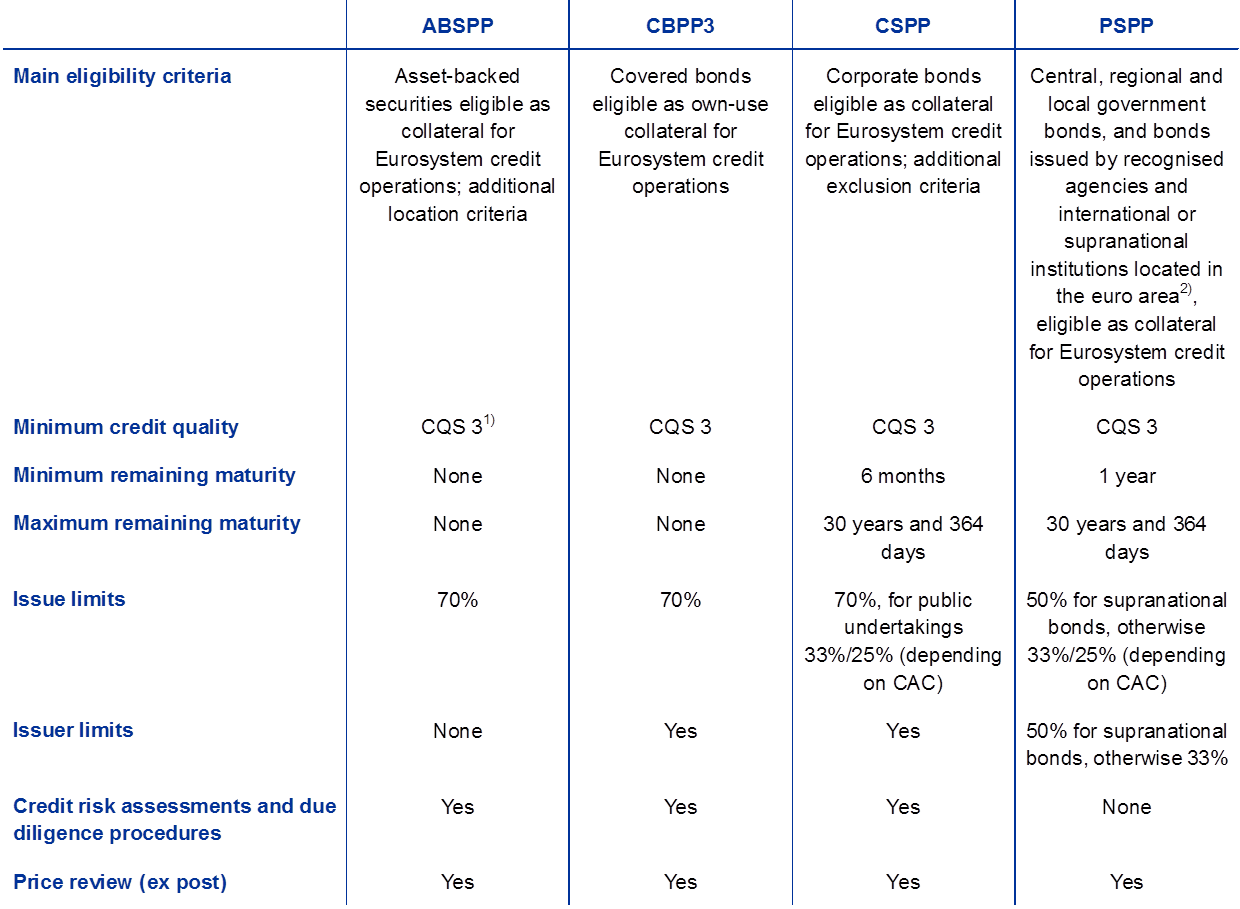

Average APP portfolio maturity and distribution across assets and jurisdictions

The APP comprises four active asset purchase programmes: the third covered bond purchase programme (CBPP3), the asset-backed securities purchase programme (ABSPP), the public sector purchase programme (PSPP) and the corporate sector purchase programme (CSPP). Following the Governing Council decisions, the monthly net purchase targets for the APP have changed over time.

At the end of 2019 APP holdings amounted to €2.6 trillion

At the end of 2019 APP holdings amounted to €2.6 trillion (at amortised cost). The ABSPP accounted for 1% (€28 billion), the CBPP3 for 10% (€264 billion) and the CSPP for 7% (€185 billion) of total APP holdings at the year-end. Out of the private sector purchase programmes, the CSPP contributed the most to the growth in APP holdings in the last two months of 2019, with €7.7 billion of net purchases. CSPP purchases are made based on a benchmark which reflects the market capitalisation of all eligible outstanding bonds.

The PSPP accounted for 82% of total APP holdings

The PSPP accounted for the bulk of the APP holdings, amounting to €2.1 trillion or 82% of total APP holdings at the end of 2019, the same proportion as at the end of 2018. Under the PSPP, the allocation of purchases to jurisdictions was guided by the ECB’s capital key on a stock basis. Within the individual purchase allocations assigned to euro area national central banks (NCBs), NCBs had the flexibility to choose between purchases of central government securities, regional government securities, and securities issued by agencies established in the respective jurisdictions. Some NCBs also purchased securities issued by EU supranational institutions. The ECB did not purchase any debt securities issued by EU supranational institutions or regional government bonds. The weighted average maturity of the PSPP holdings stood at 7.12 years at the end of 2019, somewhat lower than the 7.37 years at the end of 2018, with some variation across jurisdictions.[23]

The Eurosystem reinvested the principal payments from maturing securities held in the APP portfolios. Redemptions under the private sector purchase programmes amounted to €37.2 billion in 2019, while redemptions under the PSPP amounted to €167.3 billion.[24] The assets purchased under the PSPP, the CSPP and the CBPP3 continued to be made available for securities lending[25] in order to support bond and repo market liquidity.[26]

Developments in Eurosystem refinancing operations

The outstanding amount of Eurosystem refinancing operations decreased by €109.3 billion since the end of 2018, standing at €624.1 billion at the end of 2019. This can be largely attributed to the voluntary repayments of €208 billion of the TLTRO II series. The amount of €101.1 billion allotted in the first two operations of the TLTRO III series only partially compensated for the decline in outstanding refinancing operations due to TLTRO II repayments. The weighted average maturity of outstanding Eurosystem refinancing operations decreased from around 1.8 years at the end of 2018 to around 1.2 years at the end of 2019.

2.3 Financial risks associated with the APP are mitigated through appropriate frameworks

Risk efficiency is a key principle of the Eurosystem’s risk management function

The main objective of the renewed net asset purchases under the APP is to support the robust convergence of inflation towards the Governing Council’s medium-term aim. At the same time, asset purchases should be both necessary and proportionate to fulfil the ECB’s mandate and achieve its price stability objective. When there are several options to fulfil the policy objectives, the option selected should be efficient both from an operational as well as from a risk perspective. In that context, the Eurosystem’s risk management function endeavours to attain risk efficiency: achieving the policy objectives with the lowest amount of risk for the Eurosystem.[27]

All monetary policy instruments, including outright asset purchases, inherently involve financial risks, which are managed and controlled by the Eurosystem. The outright asset purchases require specific financial risk control frameworks which depend on the specific policy objectives and on the features and risk profiles of the asset types involved. Each of these frameworks consists of eligibility criteria, credit risk assessments and due diligence procedures, pricing frameworks, benchmarks and limits. The APP risk control frameworks apply to the purchase of additional assets, the reinvestment of principal payments from maturing APP holdings, and APP holdings for as long as they remain on the Eurosystem’s balance sheet.

Outright asset purchases require specific risk control frameworks

The risk control frameworks not only serve the purpose of mitigating financial risks, but also contribute to a successful achievement of the policy objectives by steering asset purchases towards a diversified market-neutral asset allocation. In addition, the design of the risk control frameworks also takes into consideration non-financial risks such as legal, operational and reputational risks.

In the following, the current financial risk control frameworks governing the implementation of the APP are described.[28] Table 1 summarises the key elements of the applicable frameworks.

Table 1

Key elements of the risk control frameworks for the APP

Source: ECB.

Notes: CQS: credit quality step as per the Eurosystem’s harmonised rating scale (see the Eurosystem credit assessment framework); CAC: collective action clause.

1) ABSs rated below credit quality step 2 have to satisfy additional requirements, which include: (i) no non-performing loans backing the ABS at issuance or added during the life of the ABS; (ii) the cash-flow-generating assets backing the ABSs must not be structured, syndicated or leveraged; and (iii) servicing continuity provisions must be in place.

2) See the “Implementation aspects of the public sector purchase programme (PSPP)” page on the ECB’s website.

Eligibility requirements for outright asset purchases

Eligibility criteria apply to all asset classes

Only marketable assets which are accepted as collateral for Eurosystem credit operations are potentially eligible for outright asset purchases. The collateral eligibility criteria for Eurosystem credit operations are stated in the general framework for monetary policy instruments. Among other things, eligible assets are required to meet high credit quality standards by having at least one credit rating[29] provided by an external credit assessment institution (ECAI) accepted within the Eurosystem credit assessment framework (ECAF) qualifying as credit quality step 3 (CQS 3) of the Eurosystem’s harmonised rating scale or higher (CQS 1 and CQS 2). Furthermore, assets must be euro-denominated and issued and settled in the euro area. In the case of asset-backed securities (ABSs), the debtors underlying the respective claims must be predominantly located in the euro area.

In addition to the eligibility criteria above, specific eligibility criteria apply depending on the purchase programme. For instance, for the PSPP and the CSPP, there are minimum and maximum maturity restrictions in place. For the CSPP, assets issued by credit institutions, or by issuers for which the parent undertaking is a credit institution, are not eligible for purchase. Moreover, for the CSPP and the CBPP3, assets issued by wind-down entities and asset management vehicles are excluded from purchases. In the CBPP3, the assets must fulfil the necessary conditions for their acceptance as own-use collateral for Eurosystem credit operations, i.e. they can be used as collateral by the issuing credit institution.[30] Furthermore, conditional pass-through covered bonds ceased to be eligible for purchase from 1 January 2019. In addition, asset purchases must not circumvent the rules prohibiting the monetary financing of public authorities as set out in Article 123(1) of the Treaty on the Functioning of the European Union.

Credit risk assessments and due diligence procedures

Credit risk assessments and due diligence procedures are conducted on an ongoing basis

For the private sector purchase programmes, the Eurosystem conducts appropriate credit risk assessments and due diligence procedures on the purchasable universe on an ongoing basis. Monitoring frameworks are maintained using certain risk indicators. These assessments and procedures follow the principle of proportionality, where riskier assets are subject to more in-depth analysis. If warranted, additional risk management measures may apply, also subject to the principle of proportionality. These include in particular limitations on or the suspension of purchases and, in extraordinary cases, even sales of assets, which require a case-by-case assessment by the Governing Council.

Pricing frameworks

The pricing frameworks ensure that purchases are made at market prices

The pricing frameworks for the APP ensure that purchases are made at market prices in order to minimise market distortions and facilitate the achievement of risk efficiency. These frameworks take into account available market prices, the quality of such prices and fair values. Ex post price checks are also conducted in order to assess whether the transaction prices reflected market prices at the time of the transactions.

Purchases of eligible debt instruments with a negative yield to maturity are permissible in all asset purchase programmes including, to the extent necessary, those with a yield below the deposit facility rate.[31]

Benchmarks

Benchmarks are used to ensure diversification

Benchmarks are used to ensure the build-up of a diversified portfolio and contribute to mitigating risks. The benchmarks for the private sector purchase programmes are guided by the market capitalisation of the purchasable universe, i.e. the nominal outstanding amounts of the eligible assets satisfying risk considerations. In the case of the PSPP, the ECB’s capital key guides the allocation of purchases per jurisdiction on a stock basis.

Limits

Issue and issuer limits are an effective tool to limit risk concentration

Limit frameworks are in place for the APP. The calibration of issue and issuer limits[32] takes into account policy, operational, legal and risk management considerations. The limits are fine-tuned according to the asset class, with a distinction being made between public sector assets and private sector assets.

PSPP issue and issuer limits are applied to safeguard market functioning and price formation, to limit risk concentration and to ensure that the Eurosystem does not become a dominant creditor of euro area governments. The issue limit for PSPP-eligible supranational bonds is 50% of the outstanding amount of the asset issued. For all other PSPP-eligible bonds, the issue limit is set at 33% of the outstanding amount of the issue, subject to a case-by-case verification that it would not lead to the Eurosystem having a blocking minority for the purpose of collective action clauses. Otherwise, the issue limit is 25%. The issuer limit for supranational issuers is set at 50% of the outstanding amount of eligible assets issued by the respective institution; for other eligible issuers, it is 33%.

For the private sector purchase programmes, the issue limit is 70%. In the CSPP, lower issue limits apply in specific cases, for example for assets issued by public undertakings, which are dealt with in a manner consistent with the treatment under the PSPP. In addition to these issue limits, issuer limits are applied for the CBPP3 and the CSPP. For the CSPP, the issuer limits are defined based on a benchmark allocation related to an issuer group’s market capitalisation in order to ensure a diversified allocation of purchases. Moreover, lower limits may apply if warranted based on the outcome of the credit risk assessment and due diligence procedures, as explained above.