April 9 (Reuters) – As First Republic Bank’s share price fell by double-digits in the aftermath of the collapse of Silicon Valley Bank last month, some people close to the San Francisco-based lender were worried short sellers were exacerbating its travails, according to a source familiar with the situation.

Investors who wager shares in a company will fall were increasing bets on First Republic’s (FRC.N) stock when it was already taking a beating, making it difficult for the bank to recover its value, according to the source.

Short interest in First Republic indeed increased as turmoil in the banking sector intensified, although measures vary. The percent of shares borrowed — the basic mechanism of a short bet — was minimal to start the month but increased to between 7% and 37% by March 31, according to various data provider calculations, versus averages between 3% and 5% across all stocks.

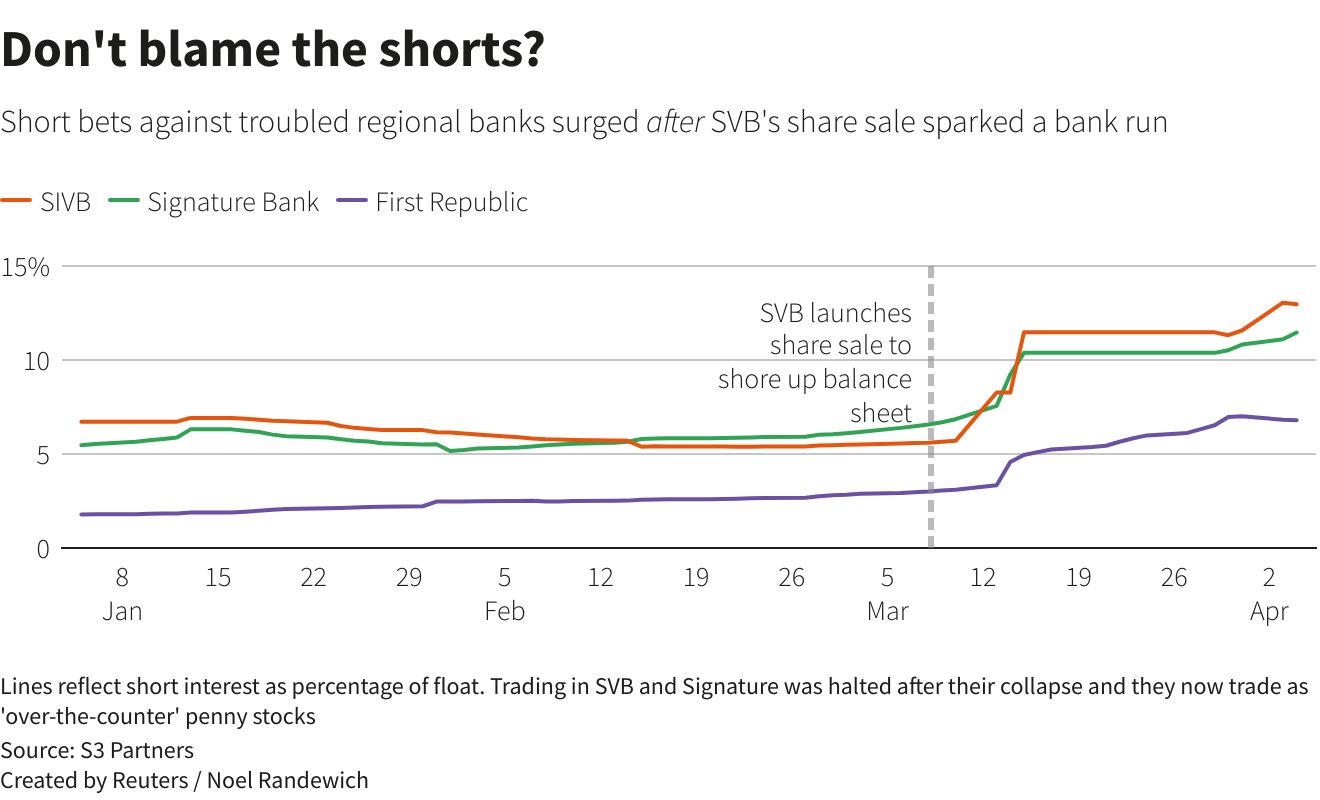

Two of the banks that shut down last month, Silicon Valley Bank (SVB) (SIVBQ.PK) and Signature Bank (SBNY.PK), showed a similar pattern: short interest increased as their stock started to fall, at varying degrees of intensity.

Problems at U.S. regional banks grew last year, as rapidly rising interest rates slashed the value of some banks’ holdings in long-term assets such as home loans and government bonds. Some lenders were also challenged by exposure to cryptocurrency and technology companies. The underlying issues exploded last month when depositor flight spiraled out of control and regional lenders across the board saw their shares hit.

How much short sellers contributed to the downward spiral reprises the debate about whether so-called shorts are market watchdogs or opportunistic investors who profit from others’ misery. In the case of the banking crisis, a review of data and interviews with short sellers and their critics show, the answer may be both.

“The shorts in the months before the collapse were accurately warning the markets…that the bank (SVB) was being dangerously mismanaged,” Dennis Kelleher, President and CEO of Better Markets, a nonprofit industry group in Washington, DC, said in an email. “The problem is once that collapse happened, shorts with various motives started targeting other banks.”

Some short sellers have been public about their negative views on banks but reject suggestions that they are to blame for the problems.

Short-seller Jim Chanos wrote in a March 13 client letter seen by Reuters that investors had known about the underlying balance sheet problems that brought down SVB since last summer. But it was only when the bank, which his fund was short, “abruptly tried, and failed, to raise capital … that anyone cared.”

First Republic and Chanos declined to comment. Signature and SVB did not respond to requests for comment.

CONTROVERSIAL PRACTICE

Short selling is a controversial practice, blamed in the financial crisis of 2008 for adding to the pain; it was temporarily banned, albeit with little impact. Some high profile short sellers were later celebrated as making prophetic calls about the U.S. housing market.

The crisis of confidence in U.S. regional banks started when shares of SVB plunged and depositors fled after it announced plans on March 8 to raise capital to fill a nearly $2 billion hole from the sale of securities.

The Santa Clara, California-based lender was taken over by regulators on March 10, in turn dragging down the shares of other regional lenders. New York’s Signature failed on March 12, and First Republic lost more than 80% of its market value by mid-March.

As the crisis accelerated, JPMorgan Chase & Co equity analysts wrote on March 17 that short-sellers were “working collectively to drive runs on banks,” and venture capitalist David Sacks asked on Twitter whether “scurrilous short sellers” had used social media to exacerbate depositor flight from SVB.

JPMorgan and Sacks did not respond to requests for comment.

Even so, interviews and public postings show at least some short sellers had placed bets against regional banks well before the crisis hit.

These included: William C. Martin, who shorted SVB in January 2023; Nate Koppikar of Orso Partners, who shorted SVB in early 2021; Barry Norris of Argonaut Capital Partners, who shorted SVB in late 2022; John Hempton of Bronte Capital Management, who shorted Signature in late 2021; and Marc Cohodes, who shorted Silvergate Bank (SI.N) in November 2022, according to interviews with Reuters.

Porter Collins, co-founder of hedge fund manager Seawolf Capital, said he saw how rising interest rates would likely hit banks and, in early 2022, shorted SVB, Signature, First Republic, Silvergate and Charles Schwab Corp. (SCHW.N).

“There were warning signs,” he said, “that were pretty easy to see for those who looked.”

Schwab and Silvergate did not respond to requests for comment.

SHORT POSITIONS

Such early short sellers, however, were in the small minority. Shorts represented only about 5% of SVB’s stock float as of March 1, according to data tracker S3 Partners, with First Republic at around 3% and Signature at 6%. That compares to an average of about 4.65% across all stocks, per S3.

Data from S&P Global Market Intelligence and ORTEX, who use different methodologies, have similar numbers showing SVB, First Republic and Signature with relatively low overall short levels before the crisis.

Short positions increased over March, although the measures vary, per the three data providers. On First Republic, the percentage of shares on loan peaked at between 7% and 39% last month, while SVB peaked at between 11% and 19%, and Signature peaked between 6% and 11%.

Regardless, short positions in most regional banks were nowhere near some highly shorted stocks like electric carmaker Tesla Inc, which hit around 25% as recently as 2019, and GameStop Corp, which surged past 100% of shares in 2020, according to Refinitiv data.

An exception was Silvergate, a cryptocurrency-focused lender, which for months faced an unusually high level of short interest compared to other banks – above 75% by the time it said it would wind down operations on March 8.

S3’s Ihor Dusaniwsky said the overall increase in shorts on U.S. regional banks during March was an “extraordinarily small” part of overall sector trading; the declines were driven by regular stock holders selling their shares.

“The shorts are not driving the stock price,” Dusaniwsky said. “People are saying that the tail is wagging the dog. It’s certainly not the case in most of these names.”

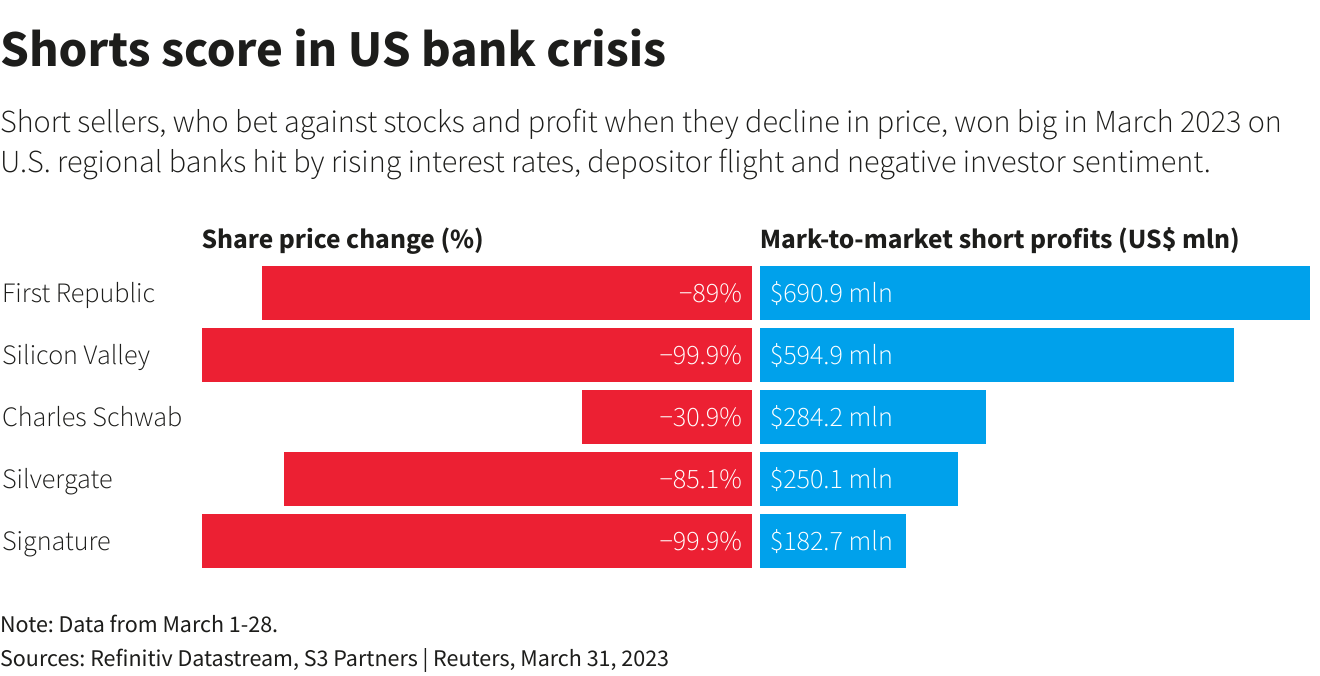

Short-sellers scored regardless: overall short bets in U.S. regional banks gained $4.76 billion in March, up 35% on an average short interest of $13.4 billion, according to S3.

Reporting by Lawrence Delevingne in Boston; additional reporting by Megan Davies in New York and Noel Randewich in San Francisco. Editing by Megan Davies, Paritosh Bansal and Anna Driver

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}