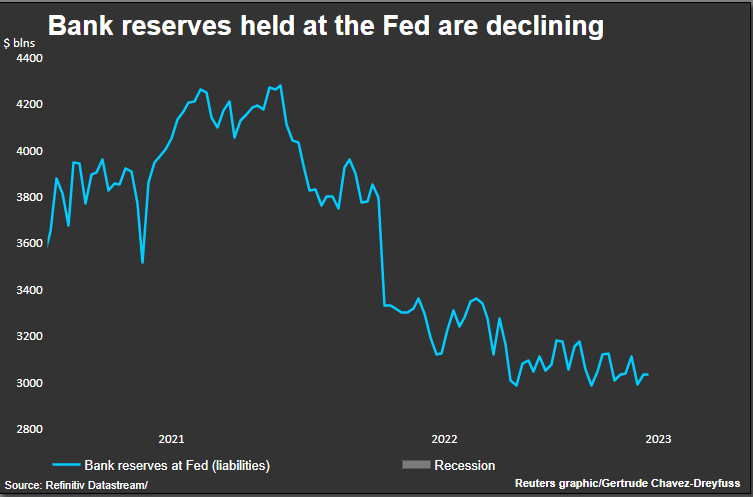

NEW YORK, March 10 (Reuters) – A rapid fall in bank reserves held at the Federal Reserve, coinciding with an expected shortage of U.S. Treasury bills as the debt ceiling battle looms, has raised concerns from investors about potential stress in financial markets.

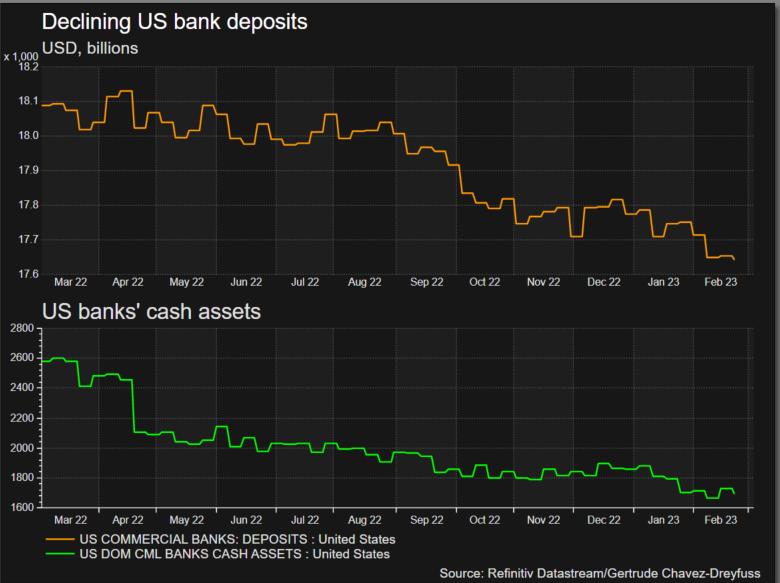

Reserves, which are funds the Fed requires banks to hold as balances at the central bank, have fallen due to the impact of the central bank’s program to reduce its swollen balance sheet, known as quantitative tightening (QT). Bank deposits, which are part of reserves, also dropped with customers seeking higher-yielding alternatives for their cash.

A persistent slide in reserves has broad implications for the economy. Lower reserves constrain banks’ balance sheets, hampering their ability to lend to finance corporate growth and expansions, analysts said.

The Fed’s balance sheet increased during the pandemic as it bought securities under its quantitative easing (QE) program, as did reserves at the central bank. That is now being unwound with QT, which was meant to drain that stimulus from the financial system.

Latest Updates

View 2 more stories

As of March 8, bank reserves during the week averaged $2.999 trillion, Fed data show, falling around $1.3 trillion from a peak of $4.3 trillion in December 2021. In the last QT cycle, $1.3 trillion in liquidity was withdrawn in five years.

“In the event of a liquidity crisis in markets, the banking system is much less ready and able to battle those shocks because of the declining level of reserves,” said Matt Smith, investment director at asset manager Ruffer in London.

One such shock was Friday’s collapse of SVB Financial group (SIVB.O), a startup-focused lender, which has raised concerns about its impact on the broader financial sector.

The last time the Fed undertook QT, it ended abruptly after bank reserves dropped in September 2019 below the minimum needed to ensure the smooth functioning of short-term funding markets. That prompted a spike in repo rates and forced the Fed to provide additional reserves to the banking system.

An expected shortage of bills as the United States hits the debt ceiling and the Treasury must curtail borrowing, is also seen reducing reserves further. The U.S. government came close to its $31.4 trillion debt limit earlier last month, prompting a Treasury warning that it may not be able to avert default past early June.

“If the Treasury is unable to issue bills because of the debt ceiling, then you get more cash into reverse repos and that brings reserves down further,” said John Velis, FX and macro strategist at BNY Mellon in New York.

In a reverse repo, market players lend overnight cash to the Fed at a 4.55% rate in exchange for Treasuries with a promise to buy them back.

Investors have been funneling cash into reverse repos or into money market funds that have access to these repos, instead of putting the money as deposits in banks, analysts said. Volumes on reverse repos have hit north of $2 trillion since June last year, even as bank reserves have dwindled.

DEPOSIT OUTFLOWS, SILICON VALLEY BANK

Deposit rates, with the current average savings rate at roughly 0.2% per annum, have not kept up with the surge in the fed funds rate that came with multiple Fed hikes. Analysts attributed that to people over-depositing during the QE period amid all the government stimulus during the pandemic.

That low deposit rate has led to deposit outflows. Deposits have been declining since the second quarter of last year, according to Fed data on banks’ assets and liabilities.

Joseph Abate, managing director at Barclays, in a research note, wrote that excess deposits gave banks more power to set deposit rates and determine how aggressive they need to be to compete for funding.

SVB Financial’s saga that started on Thursday is the latest example of how deposit outflows could adversely impact smaller banks.

California banking regulators on Friday shuttered SVB, which does business as Silicon Valley Bank amid a run on deposits. Among other issues, SVB grappled with declining deposits from startups struggling for funds.

“Banks with good liquidity and funding profiles should be able to withstand the decline (in deposits),” said Julie Solar, group credit officer at Fitch’s credit policy group.

“But banks reliant on non-core funding, have deposit concentrations, or large unrealized losses in their securities portfolios could face more pressure in this environment.”

Deposit outflows, reverse repos, and bank reserves are all inter-related. Deposits are finding their way into money market funds which invest in reverse repos. Higher reverse repo usage, in turn, effectively cuts reserves.

The current level of reserves though are still higher than in 2019 when they dwindled to $2 trillion due to heavy withdrawals for tax payments and analysts agreed that the market is not necessarily in a panic situation just yet.

But the mininum level of reserves under the current QT is probably higher than the previous cycle since the Fed’s balance sheet has grown substantially more than the last one given a huge QE program.

“All balance sheets have grown since then, so we don’t know where the biting point is,” said Ruffer’s Smith.

Reporting by Gertrude Chavez-Dreyfuss; Editing by Megan Davies, Alden Bentley and Andrea Ricci

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}