LONDON, Nov 2 (Reuters) – Bond investors bruised by a record hiking cycle are increasing their positions, betting that central banks really are done with raising rates and their next move will be down.

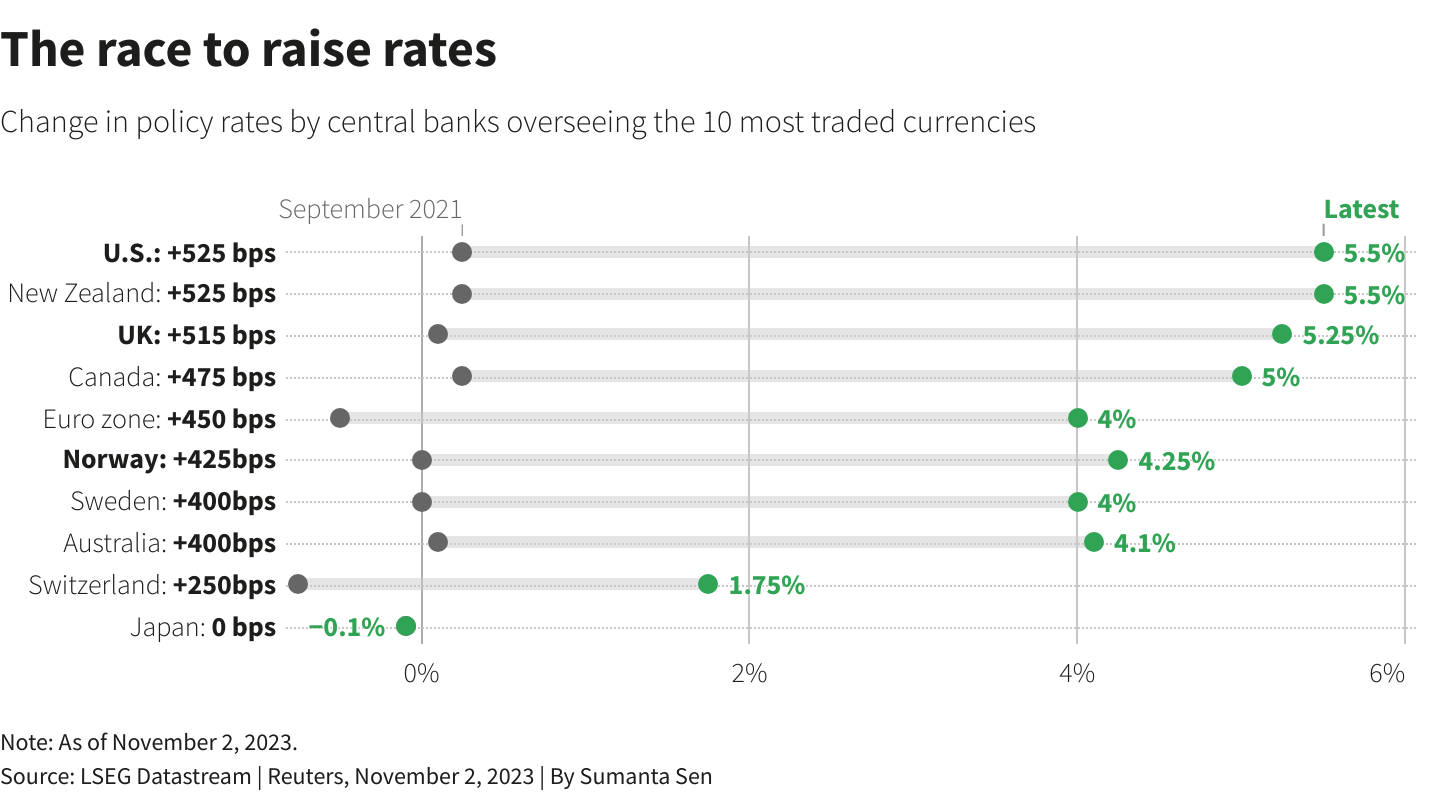

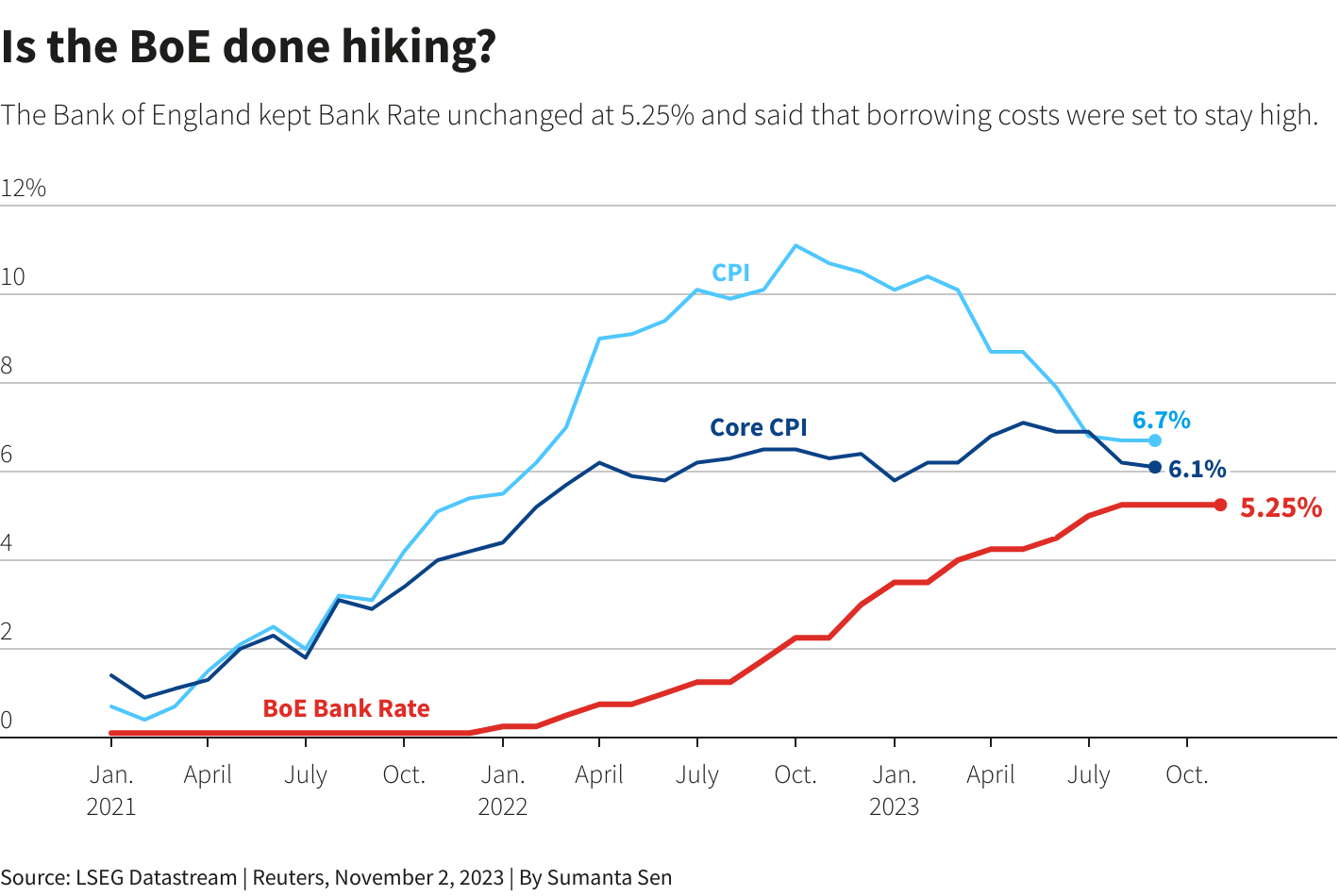

The Bank of England on Thursday followed the U.S. Federal Reserve a day before in pressing the pause button for a second straight month on what has been the most aggressive hiking cycle globally in decades to fight resurgent inflation.

Norway also kept rates unchanged on Thursday, while the European Central Bank last week paused its hikes for the first time since July 2022.

It’s a welcome sign for bond investors, sitting on a roughly 2% loss in global government bond indices so far this year after a record 13% loss in 2022.(.MERW0G1).

A drop in inflation and economic growth followed by swift rate cuts was the scenario most bond bulls predicted in late 2022. Instead, bonds underwhelmed again this year as labour markets stayed tight and central banks said inflation remained too high.

U.S. Treasuries have lost value for the last six months, their longest consecutive monthly losing streak this century, according to Deutsche Bank, pushing up yields which move inversely to bond prices.

On Wednesday and Thursday though government bond yields in the United States and Europe fall sharply, helped by hopes the Fed tightening is over .

The scale of what remains an extreme surge in bond yields since the summer means fund managers expect tightening financing conditions to squeeze economies so hard that even the robust U.S. economy slows enough for rate cuts next year.

“We are starting to see a slowdown already in Europe and we will see the same at some point in the U.S.,” said Gregoire Pesques, CIO of global fixed income at Amundi, Europe’s largest fund manager.

Pesques said that while he already had a neutral position on European government bonds, he “was thinking of adding more” U.S. Treasuries to his portfolios, from a current underweight stance.

UNFAIR VALUES?

Inflation and rising interest rates make bonds less appealing because they erode the value of the fixed coupons paid by the debt securities compared with cash in the bank.

Bludgeoned valuations help explain why investors are doubling down on bond investments with 10-year Treasury yields last month pushing above 5% for the first time since 2007.

As the benchmark for borrowing costs across the U.S. economy, with ripple effects globally, these higher Treasury yields potentially hasten an economic slowdown. They are up some 150 basis points (bps) from lows hit in April, with Fed chief Jerome Powell on Wednesday noting that all this is “showing through” to real world borrowing costs.

In Europe, Germany’s 10-year Bund yield has risen about 75 bps since late March to 2.7%.

For some investors, government bonds are too cheap compared to future expectations for interest rates and inflation.

“Valuations now look much more attractive than they did a few months ago,” said Goldman Sachs Asset Management fixed income macro strategist Gurpreet Gill.

Goldman’s investment arm has a neutral stance towards Treasuries, Gill said, but more certainty on the monetary policy path was a reason boosting their appeal.

“We have more confidence that further rate hikes are unlikely relative to a few months ago when some investors were expecting further tightening into year-end,” she said.

Nikolay Markov, lead economist at Pictet Asset Management, said a fair value for the 10-year Treasury yield was around 4%, based in part on his forecast of the annual rate of U.S. core inflation falling to 2.5% by the end of 2024.

Hopes that inflation continues moderating as economies weaken means traders are still eyeing sizeable rate cuts next year.

Even in Britain, where the BoE on Thursday ruled out a quick easing, traders moved to pull forward their expectations of a first cut to next August.

Fidelity International fixed income portfolio manager Becky Qin said the group was “growing incrementally more bullish” on developed market debt and turned positive on UK gilts as an economic slowdown would prompt a more dovish BoE.

Georgina Taylor, fund manager and head of multi-asset strategies at Invesco, said the firm had also moved into gilts in recent weeks, noting that the BoE would probably need to be the one major central bank that moves first.

INFLATION RISKS STILL THERE

Bond bulls are taking a risk though in expecting rate-setters to call time on their campaign against inflation, given that inflation remains elevated and could spike as uncertainty over conflict in the Middle East supports energy prices.

“The risks to interest rates still remain on the upside in most countries, simply because inflation is above target,” said Shamik Dhar, chief economist at BNY Mellon Investment Management.

Even in the UK, where the BoE does not expect the economy to grow in 2024, “we need to see inflation make good progress back towards target before we can seriously talk about large bond market rallies,” Dhar said.

Reporting by Naomi Rovnick and Yoruk Bahceli; Editing by Dhara Ranasinghe and Susan Fenton

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}