Rampant government spending continues to mask fundamental weaknesses in the US economy. Recently, national debt grew much faster than the economy for the third quarter in a row, just one of many warning signs concerning legendary investors. Our guest commentator explains just how much the government is spending to make the economy seem strong, even as the US remains in the midst of a “private sector recession.

The following article was originally published by the Mises Institute. The opinions expressed do not necessarily reflect those of Peter Schiff or SchiffGold.

Over the past year, economist Daniel Lacalle has repeatedly warned that the United States is in the midst of a “private sector recession” and that official GDP measures are being propped up by government spending. The latest GDP numbers from the federal government strongly suggest he is right.

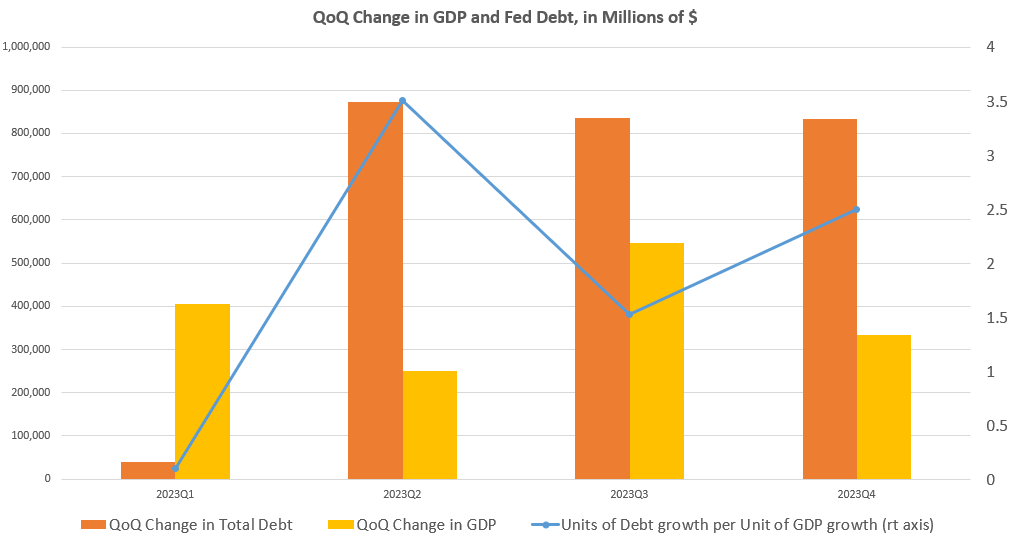

Today, the federal government’s Bureau of Economic Analysis released its revised estimate for GDP growth in the fourth quarter of 2023. According to the report, total GDP increased $334.5 billion (quarter over quarter) during the fourth quarter. That’s down from the third quarter’s quarter-over-quarter increase of $547.1 billion, but is nonetheless an ostensibly robust rate of growth.

Yet, if we compare GDP growth during the fourth quarter to growth in the total national debt, we find that the numbers don’t look quite so robust after all. While GDP may have grown by $334 billion during the period, the national debt grew by more than twice as much: $834 billion. In other words, for every dollar of GDP growth, the national debt grew by 2.7 dollars.

Moreover, this is the third quarter in a row during which debt growth has substantially outpaced GDP growth. During the third quarter, the federal debt grew $1.5 dollars for every dollar of GDP growth. During the first quarter, the debt grew 3.5 dollars for every dollar of GDP growth.

The fact that this has now happened three quarters in a row is notable as well. Over the past fifty years, it is rare to find debt growth exceeding GDP growth for more than two quarters in a row except during periods of economic weakness when the federal government relies on monetary expansion and federal spending to “stimulate” economic growth. For example, we find a three-quarter streak during the Great Recession and the years immediately afterward—when job growth was extremely weak. The same can also be seen in the quarters following the 2001 recession.

This isn’t shocking. If the federal government is trying to boost GDP numbers through “stimulus” it will both spend freely and expand the money supply as the central bank purchases Treasuries to avoid a surge in interest rates. (See more on how the central bank enables deficit spending.) The current reliance on federal deficit spending to keep up the appearance of GDP growth further backs up Lacalle’s theory that the United States is in the midst of both a public-sector expansion and a private-sector contraction. That is, the private sector is experiencing many recessionary trends, such as falling real wages, a decline in manufacturing, and growing bankruptcies. Meanwhile, however, government spending is booming, so sectors of the economy that are closely tied to government spending continue to expand. In aggregate, total GDP numbers thus show an increase, even as the private sector stagnates.

After all, it’s important to keep in mind that GDP measures include government spending, and will also include the consumption that results from additional government spending on welfare programs, weapons manufacturing, and more. As the federal government spends its deficit-financed dollars, the recipients of these dollars consume more, thus pushing up current GDP.

The general problem with this trend can be seen if we apply it to a private firm. Imagine, for instance, that a private firm managed to increase its production by a million dollars, but at the same time took on an additional $2.5 million in debt to buy new sports cars for its least productive employees. Even worse, this new debt is in addition to a huge existing debt load.

This sort of debt should never be confused with good debt, which is debt taken on to fund new capital goods. That could potentially increase productivity later on. Government debit never good debt, however, because it is taken on for purposes of immediate consumption—usually on social welfare benefits or on bombing faraway countries.

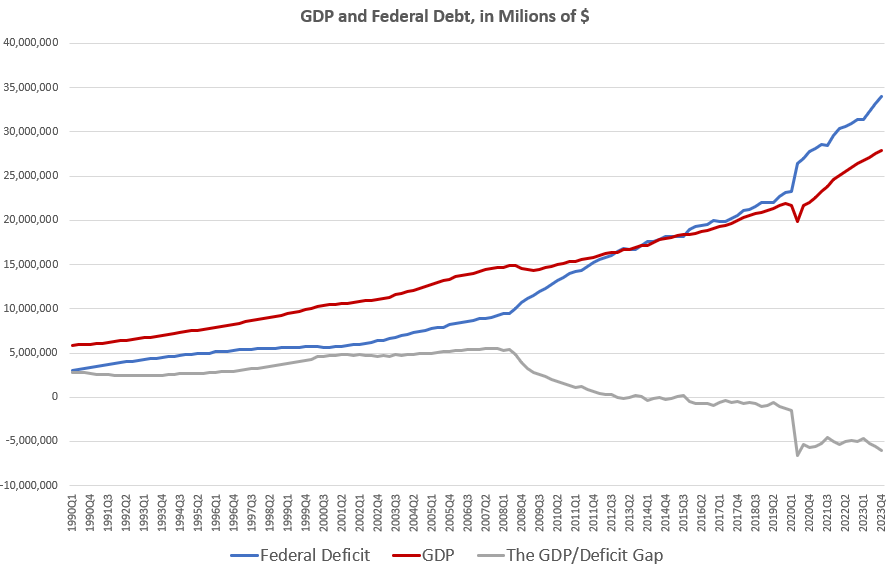

Unfortunately, as we find debt growth repeatedly top GDP growth, we are likely to see more of this phenomenon moving forward. The federal debt is now larger than the entire GDP of the United States, and the gap between debt and GDP in each year has now widened to more than six trillion dollars. As this trend continues, expect to see deficit spending play a larger and larger role in GDP.

{kind=link}