Canva

Joint accounts are on the decline for couples

The hands of two people who are using a calculator and pen to make a family budget

Despite the rise of living alone in the 21st century, most households in the United States are still led by a married couple, according to recent U.S. Census Bureau data. But household finances are anything but homogenous in 2023, as more couples are keeping most, if not all, of their finances separate. In many cases, that includes their debts as well.

Experian analyzes the details behind why the average number of joint credit accounts among couples has slowly declined over the past decade.

![]()

Experian

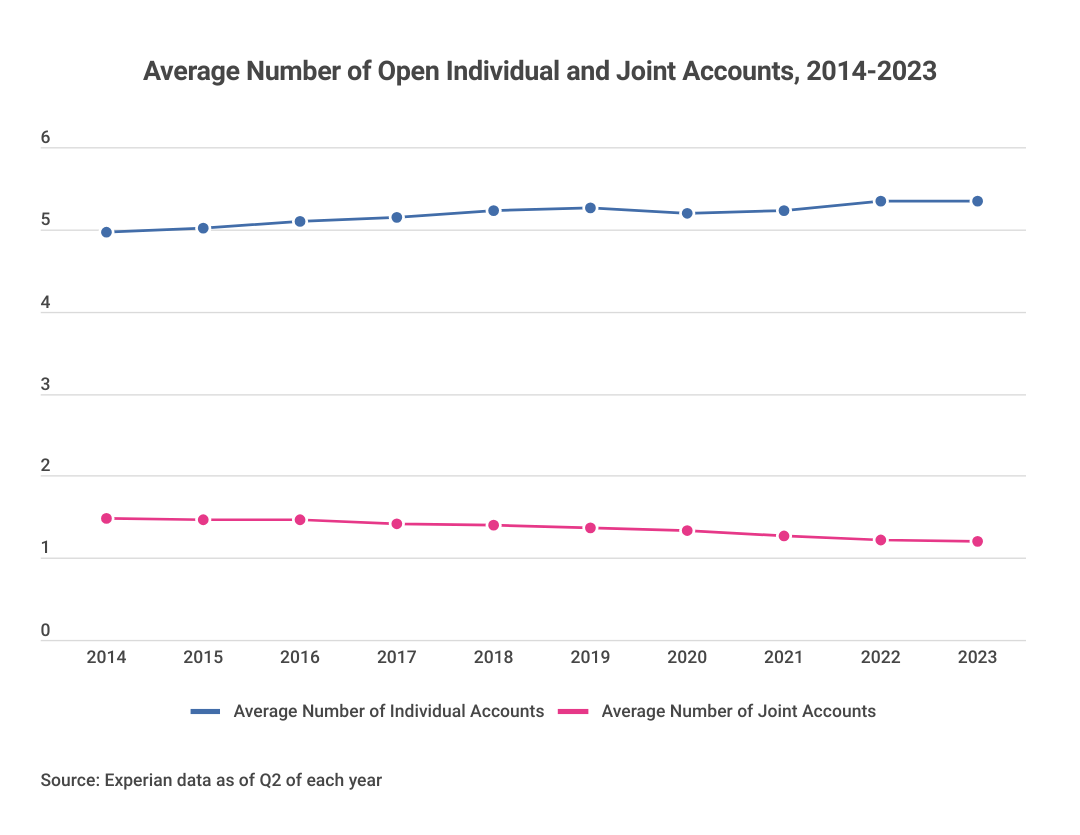

Number of joint credit accounts per couple is on the decline

a line graph showing Average Number of Open Individual and Joint Accounts, 2014-2023

Joint credit accounts are still commonplace, according to Experian data, but they aren’t as prevalent as they were in previous years.

Technically, any two or more people can be part of a joint account, but many of those who share one or more joint debt accounts are in a relationship. For example, couples represent the vast majority of borrowers for mortgages, the type of debt that comprises the largest chunk of consumer debt balances by far. According to National Association of Realtors data, married and unmarried couples account for a combined 71% of mortgage borrowers.

In this analysis, “couple” refers to any pair of people who share a joint account. Data shows the average number of joint accounts has slowly declined over the past near-decade, from an average of 1.47 credit accounts per couple in 2014 to 1.2 credit accounts per couple in the second quarter (Q2) 2023. Meanwhile, the average number of accounts for individuals over the same period increased, from 4.97 accounts to 5.35 accounts.

Experian

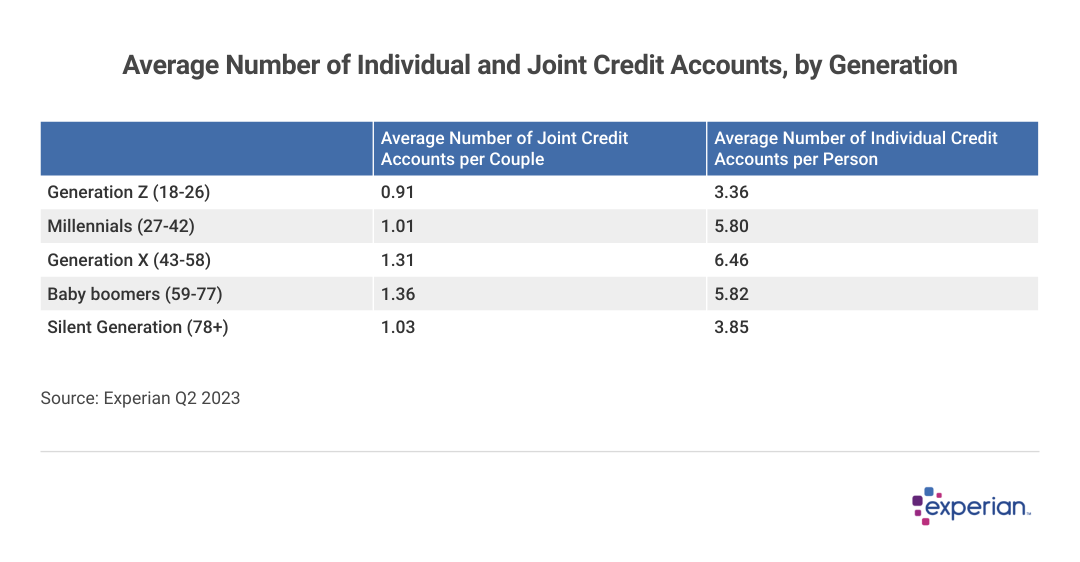

Boomers and Gen Xers lead the generational pack

A chart showing Average Number of Individual and Joint Credit Accounts, by Generation

Younger generations have fewer joint accounts than most of their elders in 2023, according to Experian data. The generation most reliant on joint accounts is the baby boomers, who have 1.36 joint accounts per couple—well above the 1.20 average for all couples.

Each successively younger generation has a lower average number of joint accounts, with the average for Generation Z, who are aged 11 to 26, being less than 1. This gap could be explained simply by the fact that members of Generation Z are less likely to be married or own a home compared with more established generations.

Also of interest are the differences in averages between baby boomers and Generation X. Although baby boomers have a somewhat higher average number of shared credit accounts, Gen Xers have more individual accounts but share fewer of them.

Experian

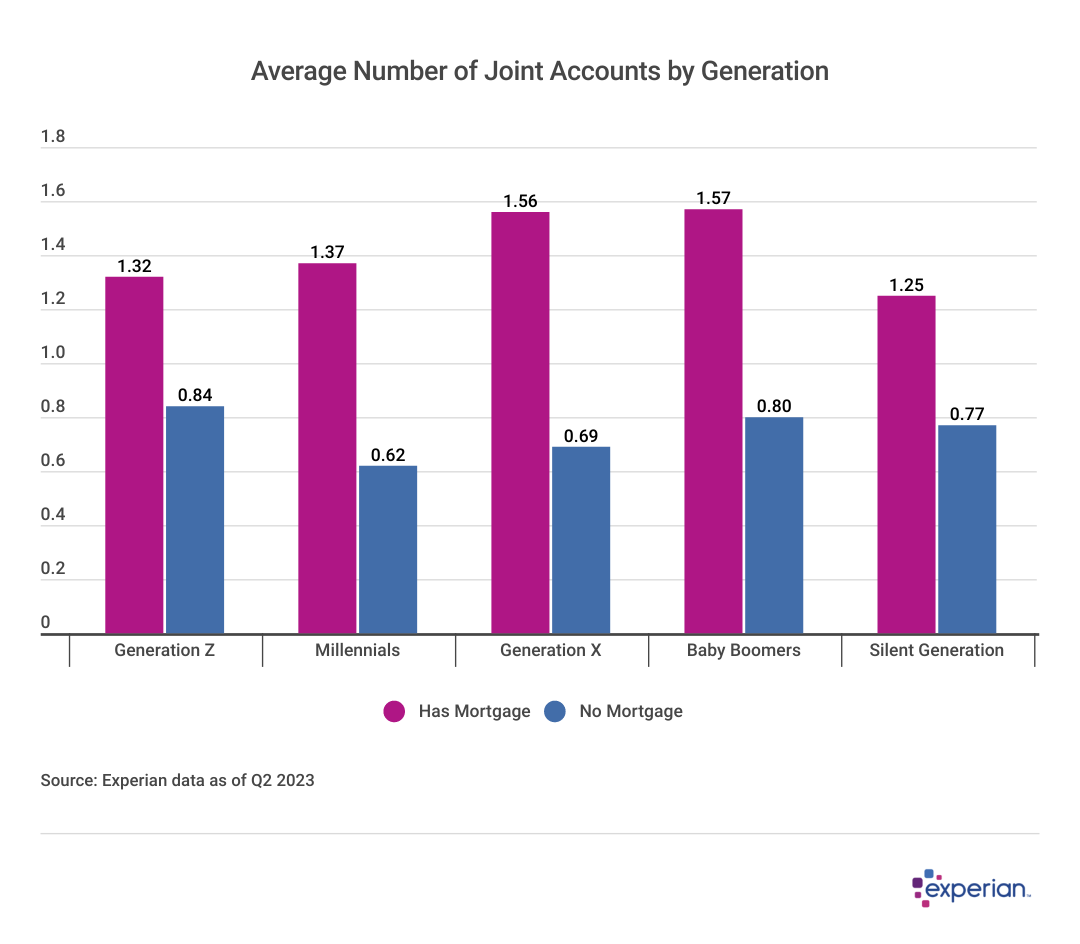

Mortgages make up the lion’s share of joint account types

A bar chart showing Average Number of Joint Mortgage Accounts by Generation

As it turns out, a couple’s preference for joint accounts may have less to do with differences in age or generational attitudes toward finances than having a mortgage.

What’s so special about mortgages that couples often apply jointly?

Many couples rely on both partners’ credit history and income to demonstrate to lenders that they’re creditworthy and have the ability to make monthly mortgage payments. As both home prices and mortgage rates continue to increase, that’s even more essential for most couples. Two incomes, if applicable, can make the difference in keeping a couple’s debt-to-income ratio lower than it might otherwise be with a single applicant.

Of course, other factors, like credit scores of each applicant, also play a prominent role. Usually, lenders will consider and use the lower score between the two applicants in making a credit determination on a joint mortgage application.

Experian

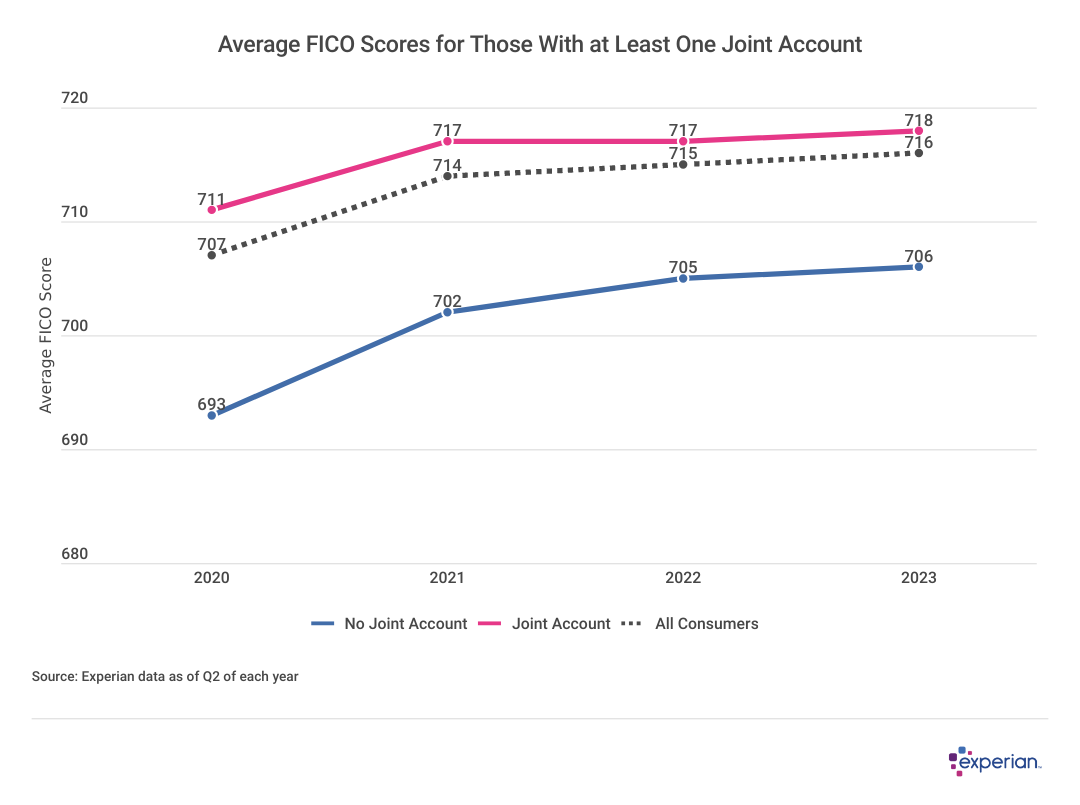

Joint credit account holders have higher average credit scores

A line graph showing Average FICO Scores for Those With at Least One Joint Account

The credit scores of those with at least one joint account are relatively healthy. As of June 2023, the average FICO Score of this group was 718, slightly higher than the overall national average FICO Score of 716. Those without at least one joint account have an average FICO Score of 706. In addition, delinquency rates are lower for those with at least one joint account.

Multiple incomes may allow couples to obtain larger mortgages that either person on their own wouldn’t be able to afford. From the lender’s perspective, having two incomes and two creditworthy borrowers means a built-in redundancy, so there’s less chance of the mortgage becoming delinquent. And while couples combining their mortgage, credit cards and other loans won’t automatically improve their credit scores, it could help build one partner’s credit history if they don’t already have an extensive history using credit.

Experian

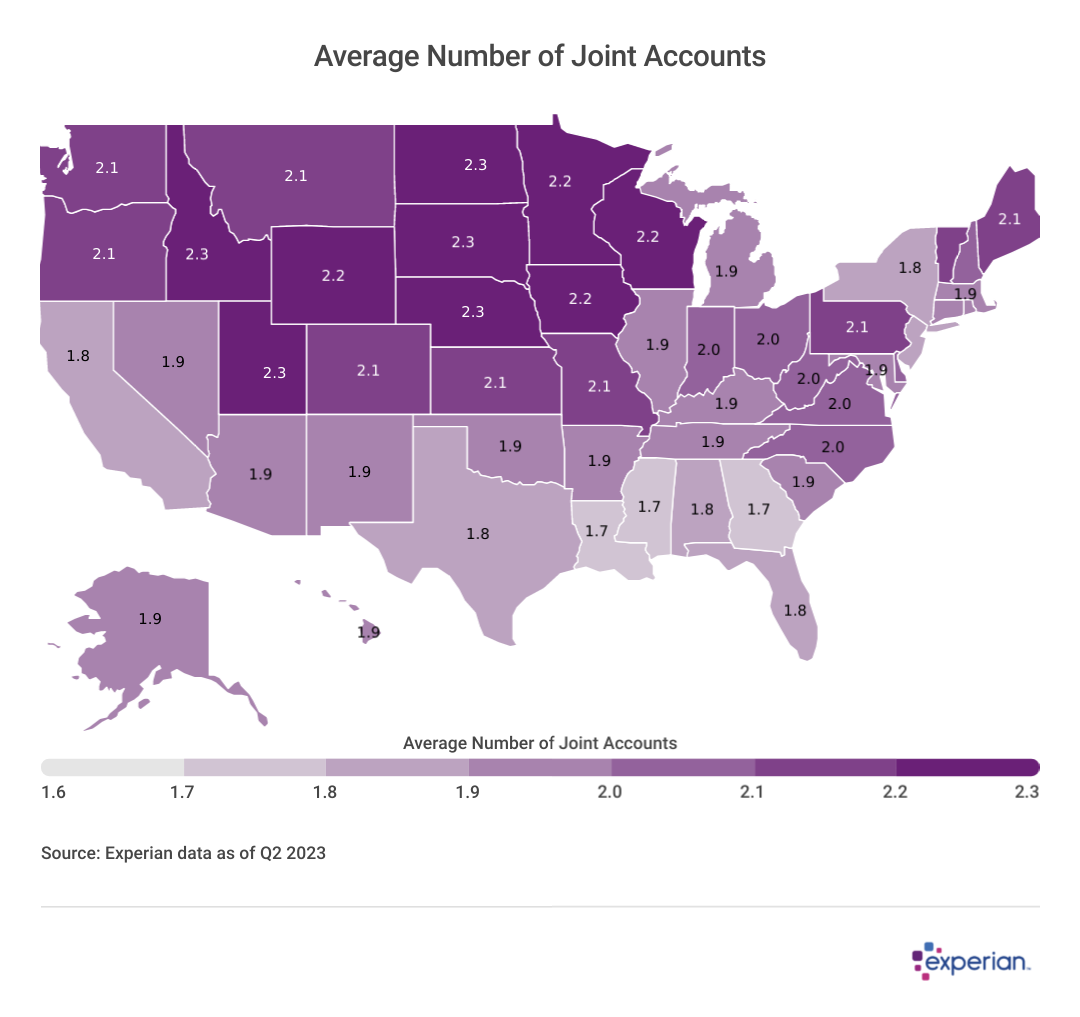

Joint accounts more common in Midwestern states

A color-coded US map showing Average Number of Joint Accounts

Many rural states, especially in the northern half of the continental U.S., have a higher average number of joint accounts than other states. However, even more populated states like Minnesota and Wisconsin also have more joint accounts on average.

These differences could be related to a number of factors. States with more joint accounts generally have higher average FICO Scores than the rest of the nation, meaning that people living there may be more likely to be able to obtain credit, joint or otherwise, than others. They may also have higher homeownership rates than other parts of the U.S., which, as we’ve previously established, is a primary draw for joint accounts. In addition, lower migration rates into and out of many of these states may mean more established roots. Finally, there may be a social dimension as well, as divorce and separation rates may be lower than in other regions of the U.S.

The number of joint accounts will likely continue to decline until home sales rebound

Because the average number of joint accounts was declining even during the relatively healthy mortgage market of the 2010s, there’s no reason to expect the decline in the number of joint accounts to reverse anytime soon. Home sales are on track to be at their lowest levels since 2005, according to data from the National Association of Realtors.

Eventually, however, the next generation of homeowners—Generation Z—will be tying knots more frequently. The median age of a first marriage is 29.2 years of age, according to the Census Bureau. So there may be a lot more wedding invitations going out in three years, when the eldest of Gen Z reach that age. Hopefully by then, the housing market won’t be as barren.

Methodology: The analysis results provided are based on an Experian-created statistically relevant aggregate sampling of our consumer credit database that may include use of the FICO Score 8 version. Different sampling parameters may generate different findings compared with other similar analysis. Analyzed credit data did not contain personal identification information. Metro areas group counties and cities into specific geographic areas for population censuses and compilations of related statistical data.

This story was produced by Experian and reviewed and distributed by Stacker Media.

{kind=link}