LONDON, May 1 (Reuters) – Inflation in the euro area is too high for comfort, meaning markets expect the European Central Bank to deliver its seventh straight interest rate hike on Thursday.

With some stability returning to banks after a March rout, hawks may feel confident pushing for a larger hike, and key inflation and bank lending data on Tuesday could sway the debate.

“The big question is, is it going to be 25 or 50 bps?,” said Gareth Hill, fund manager at Royal London Asset Management. “On balance at this stage, I’m certainly leaning more towards 25.”

Here are five key questions for markets.

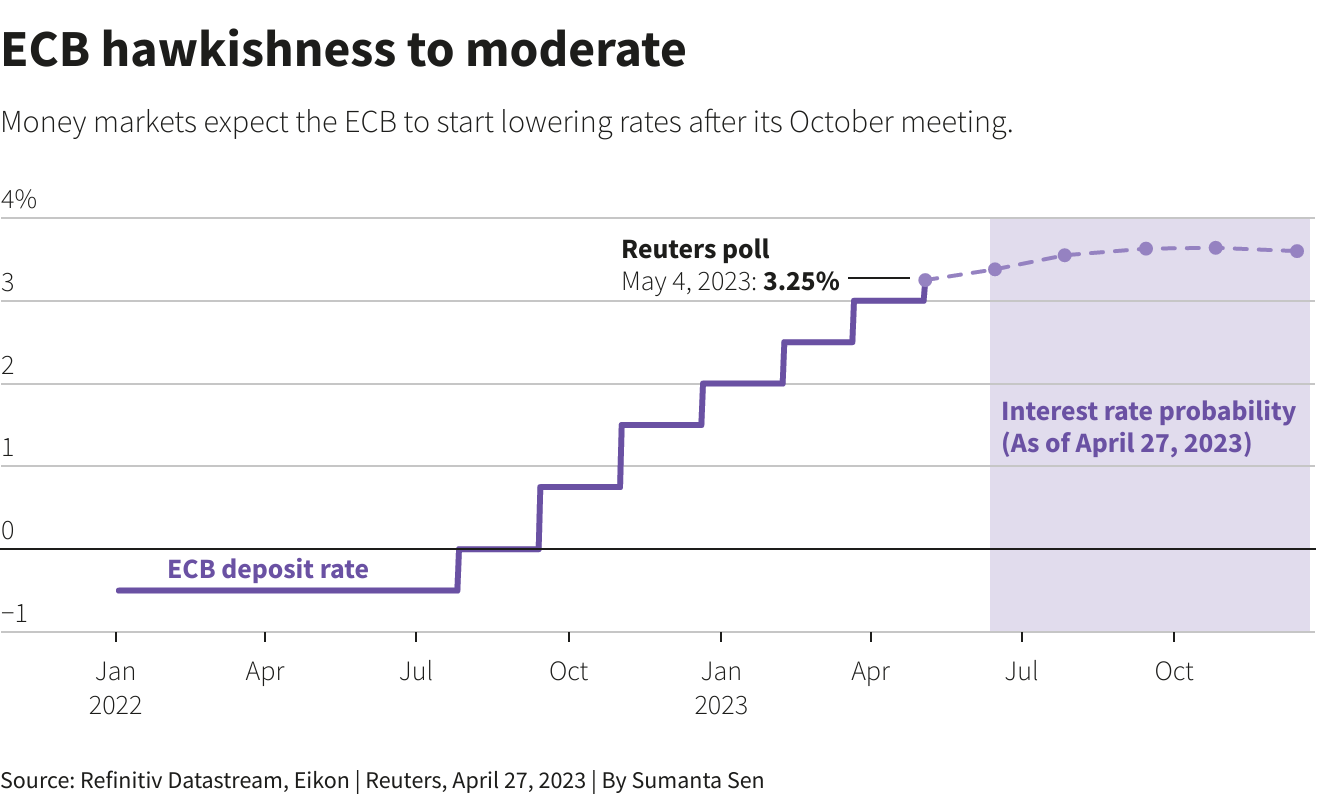

1/ How much will the ECB hike rates by on Thursday?

Economists polled by Reuters expect a 25 bps rise to 3.25%. A recent source-based report suggested policymakers were converging on a such a move, even if other options remain on the table.

ECB board member Isabel Schnabel reckons a 50 bps increase is not off the cards, while France’s Francois Villeroy de Galhau has said further moves should be limited in size and number.

April inflation and bank lending on Tuesday could be key. Data on Friday showed Germany’s economy stagnated in the first quarter, supporting the case for a small hike.

2/ When will the ECB be done with tightening?

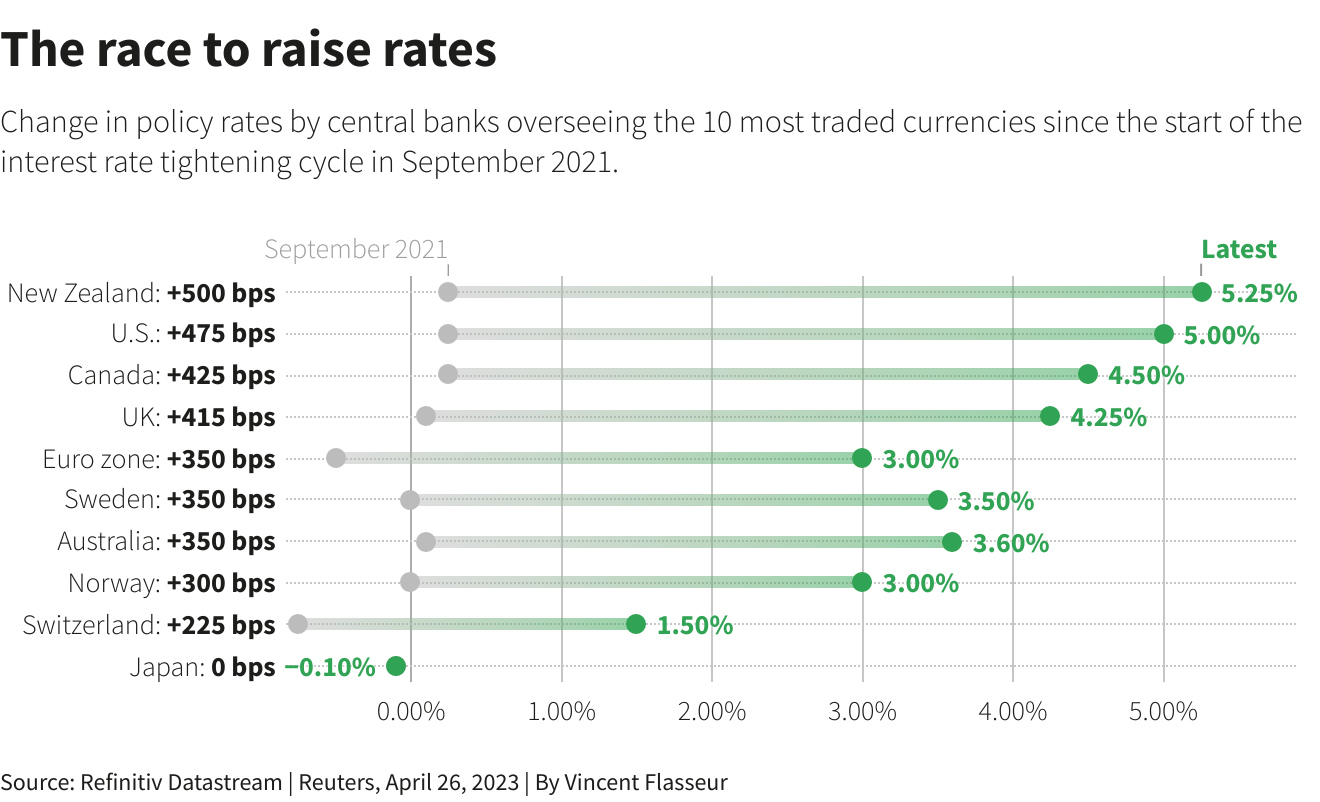

Not yet. Most analysts expect at least one more rate move after Thursday, even as the Federal Reserve looks set to pause its rate hike campaign.

Market pricing suggests ECB rates will peak around 3.6% this year, and Belgium’s central bank governor Pierre Wunsch says he wouldn’t be surprised to see rates rise to 4%.

Deutsche Bank’s global head of rates Francis Yared said he saw a possible terminal rate above 4% given that underlying inflation and wages are growing faster in Europe versus the United States, while euro area fiscal policy has more scope to be expansionary.

“If you look at it under that perspective, it’s not obvious to have a more than 1% gap between the peak policy rates in the two areas,” he said.

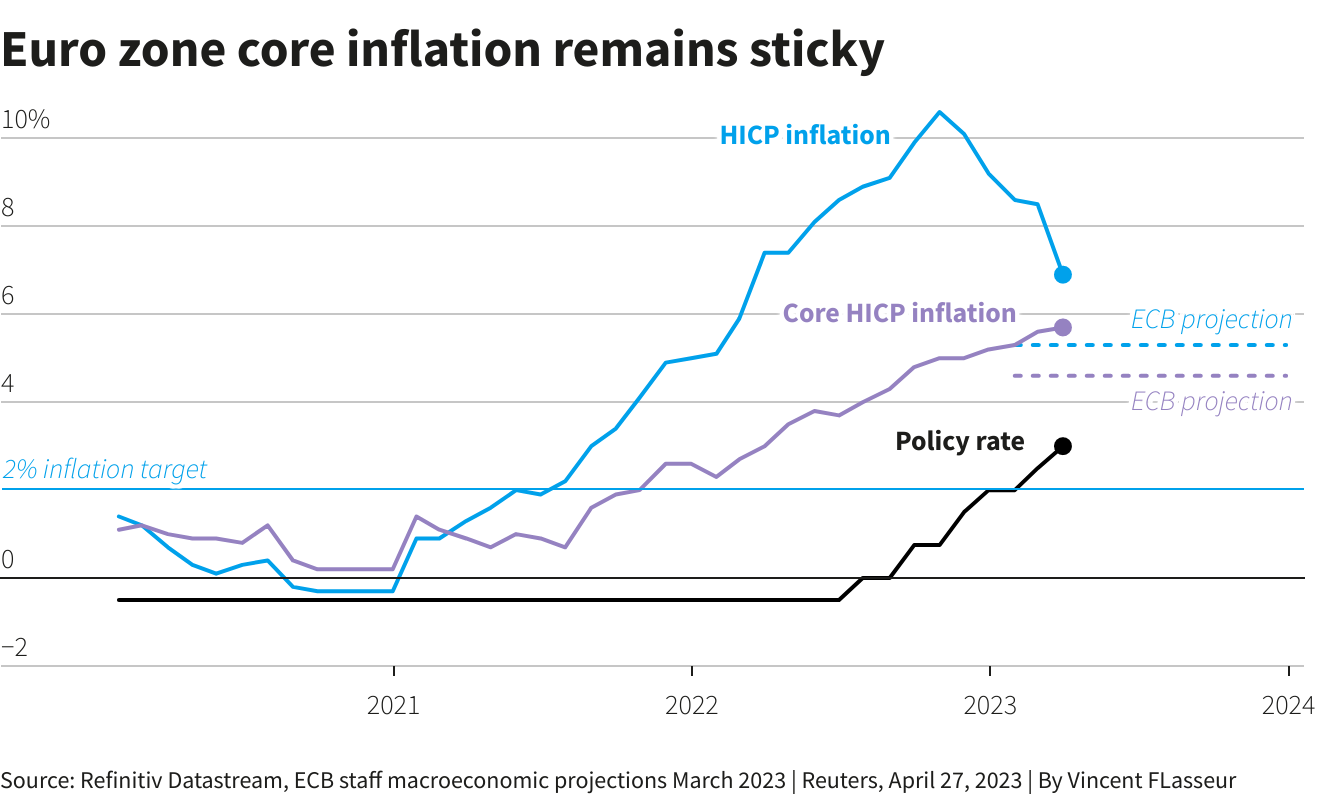

3/ How sticky is core inflation?

Very. Tuesday’s flash inflation release should show that although headline inflation continues to ease from 2022’s record highs, the underlying measure remains well above its 2% target.

Strong growth in the bloc’s services sector, making up the bulk of its economic activity, suggests core inflation and wage pressures remain elevated, complicating ECB efforts to tame inflation.

The April flash Composite Purchasing Managers’ Index, seen as a good gauge of overall economic health, jumped to an 11-month high of 54.4 in April.

4/ What’s going on with wage pressures?

Well, labour markets are tight and workers are demanding wage increases to keep up with higher prices.

Germany’s public sector workers just secured a deal to give 2.5 million employees a 5.5% permanent increase next year.

That will set an important precedent for other pay talks and could threaten the ECB’s forecast for wage growth to peak this year.

“Tight labour markets are supporting worker and union bargaining power,” said Patrick Saner, head of macro strategy at Swiss Re. “Whilst we view a 1970s wage-price spiral as unlikely, recent labour market developments must for sure be concerning for the ECB as it keeps the risk of a spiral simmering.”

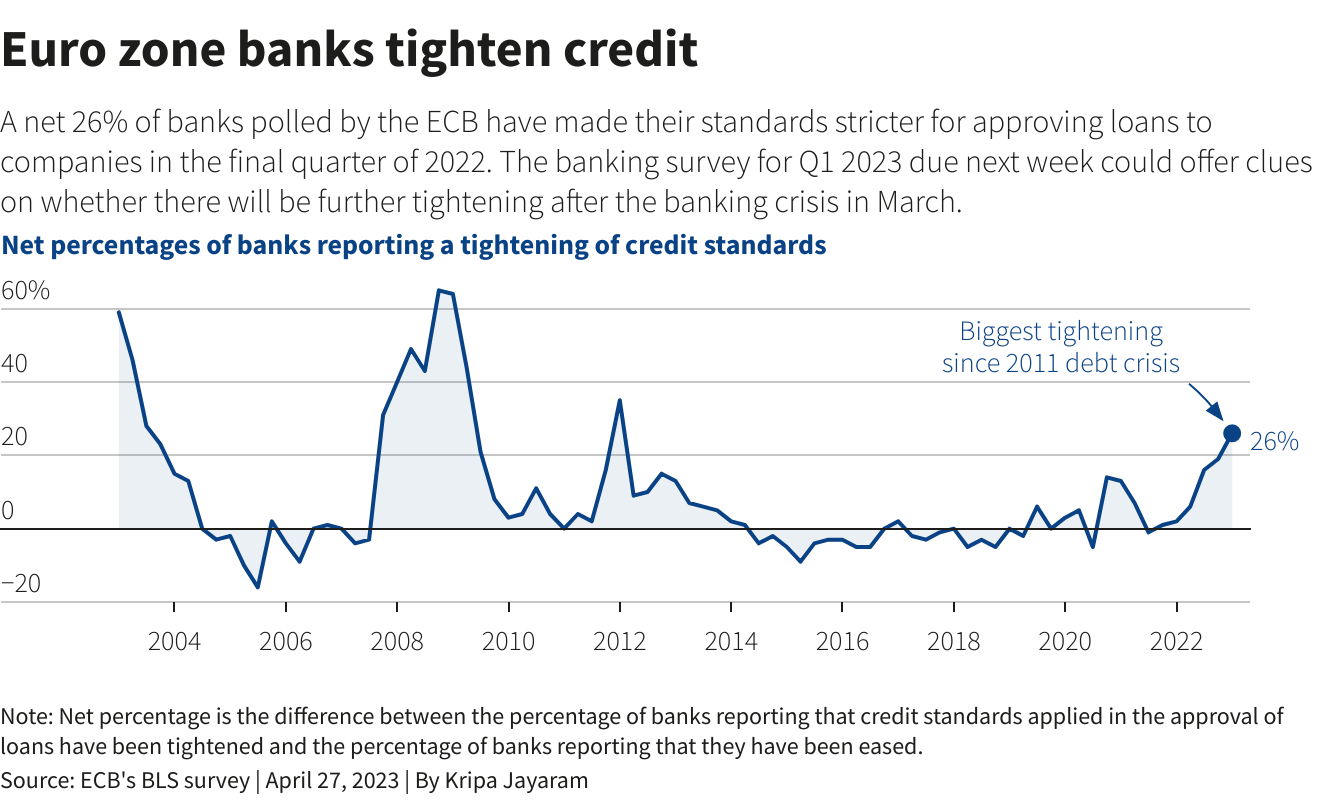

5/ How has the banking turmoil impacting financing conditions?

Tuesday’s bank lending should offer some clues but it might be too early to gauge the full impact of the March banking crisis on financing conditions.

Analysts suspect that the turmoil, which knocked 14% off European banks’ share prices overall in March (.SX7P), has further tightened lending for corporations.

“After the developments in the U.S. and Switzerland banking systems, we cut our policy terminal rate forecasts by 25 bps to 3.75% as we expect banks’ loan offices to become more risk-averse,” said Barclays European economist Silvia Ardagna, adding that the chances of a 50 bps rate hike in May was “very low” given easing economic growth and inflation.

Reporting by Dhara Ranasinghe in London and Stefano Rebaudo in Milan; additional reporting by Yoruk Bahceli in Amsterdam; Graphics by Sumanta Sen, Vincent Flasseur, Kripa Jayaram; Editing by Hugh Lawson

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}