MILAN, March 29 (Reuters) – The average European bank could withstand a loss of 38% of its deposits without having to sell at a loss government bond holdings or have a fire sale of illiquid assets, Jefferies analysts said.

The collapse of Silicon Valley Bank after deposit withdrawals that forced the U.S. regional lender to sell Treasury bonds at a loss has focused investors’ attention on the potential losses banks face on their government bond holdings.

“Following the unravelling of several U.S. regional banks and the announced rescue merger of Credit Suisse into UBS (UBSG.S), investors have scrambled to find weak links in the system,” Jefferies said in an analysis of bank liquidity.

“Most investor discussions end up at deposit flight risk and the extent to which this can be offset,” it added.

Rising interest rates have pushed down the market price of government bonds, but banks do not need to reflect that for the sovereign holdings which they intend to hold to maturity (HTM).

This saves them from taking a hit to their capital reserves.

But investors are worried about the risk that banks may at some point be forced to sell their HTM securities.

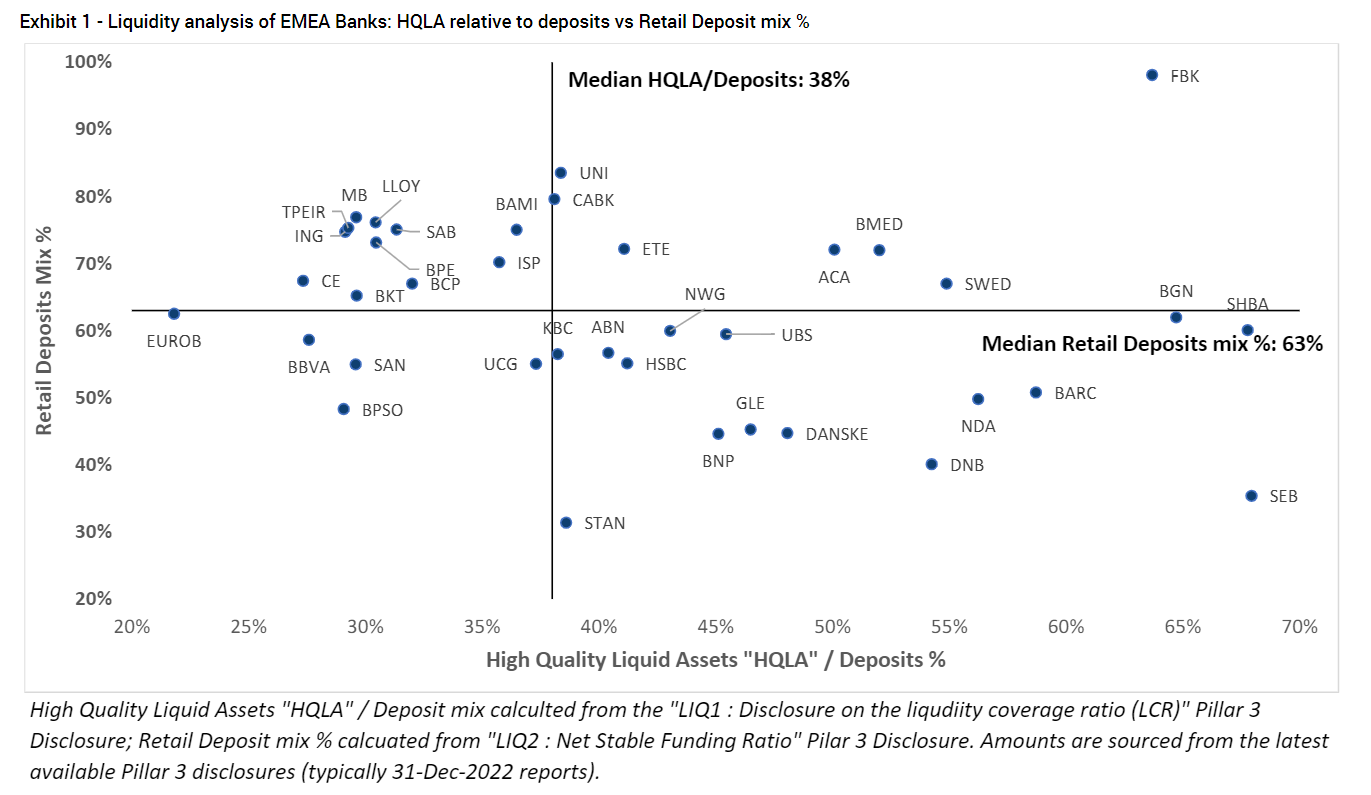

Jefferies calculated that the median European bank could lose in theory 38% of its deposits before facing significant risk to capital due to losses on its HTM securities or the sale of other illiquid assets.

Short-term liquidity regulations introduced after the global financial crisis “appear to be working as intended, irrespective of investors’ current partial lack of faith in liquidity coverage ratios,” the note said.

Jefferies analysed the ability of banks to quickly cover deposit outflows with minimal or no losses, against the level of retail deposits, which comprise 63% of the median bank’s deposit base.

Retail deposits are an important source of funding stability because they are stickier than corporate deposits and pose mainly a threat in terms of cost of funding, rather than an outright danger of outflows.

“Our framework … shows Fineco (FBK.MI), Swedbank (SWEDa.ST), Credit Agricole (CAGR.PA) and National Bank of Greece (NBGr.AT) as screening relatively well,” Jefferies said.

Standard Chartered (STAN.L), Santander (SAN.MC) and BBVA (BBVA.MC) do not score particularly high, Jefferies said, adding however that their geographic diversification had to be taken into account as a mitigating factor.

Following are the results of Jefferies’ liquidity analysis:

Reporting by Valentina Za and Iain Whithers. Editing by Jane Merriman

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}